How To Pay Off Debt With A Personal Loan

Last updated 03/26/2024 by

Andrew Latham

Regardless of what you might have heard, borrowing from Peter to pay Paul is not always a bad idea. All things being equal, if Peter charges a lower interest rate, you’d be a fool not to. Personal loans can be an excellent way to pay off your credit card debt, lower your interest payments, and even repair your credit score. But you have to do it right or a personal loan could cost you instead of saving you money.

What a Personal Loan Does

Before we get into how to use a personal loan to pay off your loans, it’s worth highlighting exactly what paying your credit card debt with a personal loan will, and will not, do for you.

Before we get into how to use a personal loan to pay off your loans, it’s worth highlighting exactly what paying your credit card debt with a personal loan will, and will not, do for you.

Personal loans can help you consolidate your debt into a single more manageable loan. If you do it right, it can save you money and improve your credit score

Personal loans can help you consolidate your debt into a single more manageable loan. If you do it right, it can save you money and improve your credit score- Taking out a personal loan will not pay your credit card debt. It will refinance your debt for a loan with (hopefully) better terms. If you have more than one outstanding credit card (or other loans), it will consolidate the debt into a single more manageable loan.

- A personal loan will also convert your credit card debt into a fixed-term loan. Most personal loans have terms ranging from 1 to 5 years. Credit cards are open-ended sources of credit. As long as you pay the minimum amount, there is no fixed deadline to pay your credit card balance. You could pay it today or drag it out for years or even decades by just paying the monthly minimum.

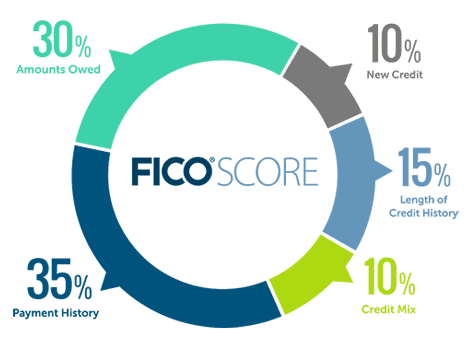

- Personal loans can also help improve your credit score. How? Well, 10% of your FICO credit score, the score most widely used by lenders, is based on your credit mix. If you only have one source of credit, such as credit card debt, it could hurt your score. Having a varied credit mix, such as personal loans, mortgage, and credit card debt can improve your credit score.

- Depending on how much you currently pay toward your credit card debt, getting a personal loan could extend the term of your credit card debt. Although doing this would probably lower your monthly payments, it may also increase the overall cost of your debt. Unless reducing your monthly payments is your chief concern and you can’t afford any other solution, it’s best to opt for the shortest possible term.

Check Your Credit Score Before Applying For A Personal Loan

It’s smart to take a good look at your credit report before shopping for personal loans. After all, this is the data on which lenders will base their decision when assessing your loan application and setting your interest rate.

It’s smart to take a good look at your credit report before shopping for personal loans. After all, this is the data on which lenders will base their decision when assessing your loan application and setting your interest rate.

You can check your credit rating for free at annualcreditreport.com and it only takes a few bucks to get your credit score with the three main credit rating agencies: TransUnion, Equifax, and Experian.

Here is a cheat sheet of recommended lenders by credit score. All the lenders below (except LightStream) allow you to prequalify and check your rates without a hard pull on your credit. So there is nothing to lose by applying and seeing what rates you get.

- If your credit score is higher than 740, your credit score is excellent and lenders will offer you the best interest rates available. Try SoFi and LightStream. They offer low rates with excellent terms but only consider super-prime borrowers.

- If your credit score is higher than 700, you have a good score and you’re likely to get approved for most loans. Try LendingClub and Prosper.

- If your score is below 700, you may still have a chance to qualify for a loan, but expect to pay higher interest rates. Try Avant and Upstart.

- If your score is below 640, finding a lender with decent rates will be a challenge but you still have options.

Improve Your Credit Score

If your score is not great, you may consider improving it before you apply for a loan. You can save hundred of dollars in interest by increasing your credit score before applying for a loan.

If your score is not great, you may consider improving it before you apply for a loan. You can save hundred of dollars in interest by increasing your credit score before applying for a loan.

The best way to improve your credit score is by paying your bills on time, reducing your available credit-to-debt-ratio and removing inaccurate negative items on your report.

Although it’s a good idea to have an emergency fund that will cover your expenses for six to 12 months, you should invest anything above that into reducing your credit card debt. If you’re looking to consolidate your credit card debt with a personal loan you probably don’t have a lot of cash lying around and paying off debt with savings is a moot point. However, you would be surprised how many people have significant amounts of money languishing in savings account with 1% or 2% APY while they pay 15%, 20% or even higher interest rates on their credit card debt.

Shop Around For The Best Personal Loan

Purchasing a loan is like buying a used car. Prices vary wildly depending on whether you buy from a private owner or a dealership, as well as on the age, brand, and condition of the vehicle. Personal loans are also a highly competitive business where prices vary by provider. So get ready to kick some tires.

Purchasing a loan is like buying a used car. Prices vary wildly depending on whether you buy from a private owner or a dealership, as well as on the age, brand, and condition of the vehicle. Personal loans are also a highly competitive business where prices vary by provider. So get ready to kick some tires.

This is particularly important if you have poor credit. Sadly, there are many unsavory companies who specialize in loans for borrowers with poor credit and take advantage of the desperation of people who know their credit is not great. Payday loans with APRs of 700% and higher are a classic example of the usurious rates lenders charge consumers who need cash fast.

Secured personal loans, such as car title loans and home equity lines of credit (aka HELOC), use your assets as collateral.

Secured personal loans, such as car title loans and home equity lines of credit (aka HELOC), use your assets as collateral.Beware of “secured loans,” such as car title loans and home equity lines of credit (aka HELOC). Although these loans usually have lower interest rates, they will convert your credit card debt from an unsecured loan to a secured loan. If you cannot make the payments, the lender could sell your vehicle or house to cover the balance of the loan.

Do the Math Before Choosing a Personal Loan

Consolidating your credit card debt with a personal loan only makes financial sense if it saves you money or if it reduces your monthly payments. If you’re struggling to make ends meet, particularly if you have other debts, such as a mortgage or car loan to pay, reducing your monthly debt payments may be your first priority. However, it may come at the expense of increasing the overall interest charged on your debt.

Consolidating your credit card debt with a personal loan only makes financial sense if it saves you money or if it reduces your monthly payments. If you’re struggling to make ends meet, particularly if you have other debts, such as a mortgage or car loan to pay, reducing your monthly debt payments may be your first priority. However, it may come at the expense of increasing the overall interest charged on your debt.

Personal loans don’t always save you money. Check their interest rates and terms before purchasing a personal loan

Personal loans don’t always save you money. Check their interest rates and terms before purchasing a personal loanIf saving money on interest is your priority, make sure the interest rate, including fees, of the personal loan is lower than the interest rates charged by the credit cards. Be realistic about how much you can afford to pay every month, but at the same time keep the term of your personal loan as short as you possible.

A shorter term will mean higher payments, but it could save you as much, or even more, than the savings generated by lower interest rates.

Do Your Homework

Before you agree to a personal loan, read the small print and make sure you understand its terms and what fees will be added to the cost of your loan. For instance, if your financial situation were to improve and you could afford to repay the entire loan, would the lender charge a pre-payment penalty fee? Does the lender charge an origination fee? Origination fees are included in the APR but are deducted from the loan amount before it is deposited in your account. For instance, if you borrow $10k and you have to pay a 5% origination fee, you will only receive $9,500 in your account.

Before you agree to a personal loan, read the small print and make sure you understand its terms and what fees will be added to the cost of your loan. For instance, if your financial situation were to improve and you could afford to repay the entire loan, would the lender charge a pre-payment penalty fee? Does the lender charge an origination fee? Origination fees are included in the APR but are deducted from the loan amount before it is deposited in your account. For instance, if you borrow $10k and you have to pay a 5% origination fee, you will only receive $9,500 in your account.

Check whether the company is accredited by the Better Business Bureau. Visit the website of your state’s finance oversight department and check the lender’s profile to see whether it has been (or is being) sued for using illegal or unethical lending practices. You should also check whether its license is up-to-date. For example, if you live in California, go to the website of the California Department of Business Oversight and check the lender’s credentials.

Confirm the lender will report your payments to credit reporting agencies. This is particularly important if you need to build or repair your credit.

Having a personal loan with a track record of regular payments will improve the mix of credit types on your credit history and will show a pattern of responsible borrowing, which will improve your credit score. But this only works if lenders regularly report your payments, and they are not required to do so by law. In fact, many lenders avoid the administrative costs and only report you when you fail to make a payment.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

AddTable of Contents