How Do You Refinance a Personal Loan?

JW

Last updated 03/26/2024 by

Jessica WalrackAre you looking to get a better deal on your current personal loan? Whether you want to lower your payment, change your term, improve your APR, or all of the above, refinancing may open that door. Read on to learn how to refinance a personal loan, and how to know if refinancing is right for you.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What does it mean to refinance a personal loan?

When you refinance a personal loan, you take out a new personal loan (ideally with better rates and terms), and use it to pay off your current loan in full. If you’re struggling with your monthly payments and need to lower them at any cost, a loan with a longer term might better suit your needs. Or if you want to save money overall, look for a loan with a lower APR.

For example, say you have $5,000 left to pay over 3 more years with a 10% annual percentage rate (APR). If another lender offers you a three-year $5,000 loan with a 6.5% APR, you could save on interest and potentially pay off the loan off early.

If you decide to refinance, you’ll originate the new loan and use the proceeds to pay off your existing loan. Then, you will make payments to your new lender until the account is paid off.

How do you refinance a personal loan?

If you are interested in refinancing your personal loan, here’s what you need to do.

Shop around

First, shop around to see if you can get a loan that will be better, in some way, than the one you have.

The good news is, shopping for personal loans is easier than ever. Many lenders use online applications, which you can use to get a quote without hurting your credit score. Plus, you can use SuperMoney’s personal loan engine get offers from top lenders in just a few minutes.

Compare offers

Once you have at least three offers, compare them to each other and to your existing loan. Remember, it’s important to look at the whole picture, including loan term (how long the loan will take to repay), APR (how much you pay per year in interest), fees (look out for prepayment fees, in particular), and overall customer satisfaction (how happy past customers are with the lender).

Apply for the new loan

When you find an offer you want to take, you can go ahead and complete the origination process with that new lender. Once you receive the funds, use them to repay your old loan. Always confirm that your old loan is closed off and paid-in-full.

Then, start making payments to your new lender and enjoy the benefits of the new loan.

Does refinancing a personal loan hurt your credit?

Refinancing a personal loan can temporarily hurt your credit due to the following reasons.

A hard inquiry on your credit report

When you are shopping for a new personal loan, look for lenders that will prequalify you without a hard credit check. You can get many quotes now without impacting your credit score.

However, once you select an offer and go ahead with the loan process, a hard inquiry will be processed. The hard inquiry will stay on your credit report for 12 months, and can lead to a small drop in your credit score.

A reduction in the average age of accounts

The average age of your credit accounts is a factor in your credit score. The higher your average, the better. When you pay off your existing loan and add a new one, it may decrease the average age of your accounts, which could hurt your score.

However, while refinancing your personal loan can cause a drop in your credit score, it won’t cause long-term harm. As you begin repaying your new loan on time, you will build a new positive credit line, which will bring your score back up.

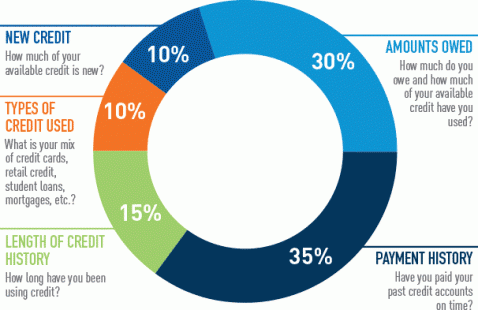

Personal loans and credit scores

Personal loans can help or hurt your credit score. The factors that affect your credit scores (ranked from most to least influential) include:

- Payment history.

- Credit utilization.

- The type, number, and age of credit accounts.

- Total debt.

- How many new credit accounts and inquiries are on your report

Because payment history is the most heavily weighted factor, making timely payments will help to boost your credit.

Additionally, if you open a personal loan and do not have other installment-type credit lines, it can improve your profile by diversifying your credit mix.

However, personal loans can also hurt your credit if you don’t keep up with your payments. Further, as covered above, they can temporarily hurt your credit when first initiated due to the hard inquiry and drop in your average age of accounts.

In the long run, though, as long as you stick to the payment turns, personal loans are good for your credit.

When can you refinance a loan?

You can refinance a personal loan whenever you can qualify for a new loan. Terms and qualifications will vary by lender, so you’ll have to check as you are shopping around.

How long does it take to refinance a loan?

The process of refinancing a personal loan varies from lender to lender. In total, it often ranges from 5 to 14 business days. Be sure to check with potential lenders when deciding, especially if time is an important factor for you.

Pros and cons of refinancing a personal loan

Still not sure if refinancing your personal loan is right for you? Here are the pros and cons:

Should you refinance your personal loan?

Do you need to lower your monthly payments? Or are you looking to pay off your loan early? Has your credit score gone up since you initiated your current loan? If you answered “yes” to any of these questions, refinancing is worth investigating.

Knowing whether you should refinance a personal loan can be tricky. It all depends on your circumstances and goals. More specifically, it depeonds on whether you can qualify for better loan terms than you currently have. And whether the savings are sufficient to justify your prepayment penalty or any other account closing costs.

Not sure if you qualify for a better offer? SuperMoney can help! Find out what rates you qualify for in minutes with SuperMoney’s personal loan engine.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: