Roth IRA vs. Traditional IRA vs. Brokerage Account: Which is Right for You?

Last updated 04/23/2026 by

SuperMoney Team

Edited by

Andrew Latham

Summary:

Trying to decide between a Roth IRA, traditional IRA, or a taxable brokerage account? Each offers a different mix of tax benefits, flexibility, and long-term growth potential. This guide breaks down when a Roth IRA makes the most sense — and when a traditional IRA or brokerage account might be the better play for your goals.

When it comes to building wealth, the type of account you use matters almost as much as what you invest in. That’s why it’s important to understand the strengths and limitations of different investment vehicles. This guide focuses on how Roth IRAs compare with traditional IRAs and regular brokerage accounts — and helps you figure out the best place to grow your money.

The first thing to remember is that most brokerages offer Roth and Traditional IRA so it’s not a case of comparing IRAs to brokerages but discussing the type of account that fits the best for your needs.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

When a Roth IRA is better than a traditional IRA

Here are some scenarios when Roth IRAs really shine.

When you expect to be in a higher tax bracket in retirement

If you’re early in your career, between jobs, or earning less than you expect to in the future, a Roth IRA can be a tax-smart move. You pay taxes now — while you’re in a lower tax bracket — and withdraw money tax-free in retirement.

“Pay taxes on the seed, not the harvest.”

Young professionals and people in transition periods (like grad school or career changes) can benefit the most. Locking in today’s lower rates is a powerful strategy if you expect to earn more — or if tax rates rise.

When you want tax-free growth and withdrawals

One of the biggest perks of a Roth IRA is that all qualified withdrawals — including earnings — are completely tax-free. That means no taxes on decades of compounding growth if you follow the rules (age 59½ and 5-year account rule).

This makes a Roth ideal for long-term investors who want to hedge against future tax increases or enjoy worry-free withdrawals in retirement.

When you want flexibility

Roth IRAs let you withdraw your contributions at any time without penalties or taxes. That’s a huge benefit over traditional IRAs, which charge penalties for early withdrawals. You also don’t have to take required minimum distributions (RMDs) from a Roth during your lifetime — which gives you more control in retirement.

When you don’t qualify for a deductible traditional IRA

If your income is too high and you’re covered by a retirement plan at work, your traditional IRA contributions might not be deductible. In that case, a Roth IRA is the better choice — if you’re still within the income limits.

When a traditional IRA may be better

Traditional IRAs still have some advantages, especially if you’re looking to lower your tax bill today. Here are a few cases where they make more sense:

- You’re in a high tax bracket now and expect to be in a lower one later.

- You want the upfront tax deduction to reduce this year’s taxable income.

- Your income is too high for a Roth IRA and you’re not interested in a backdoor Roth conversion.

Quick example:

A 25-year-old making $60K? A Roth IRA is likely better — lock in a low rate and enjoy tax-free growth.

A 55-year-old earning $180K and expecting a modest retirement? A traditional IRA may offer better tax relief now and lower taxes later.

A 25-year-old making $60K? A Roth IRA is likely better — lock in a low rate and enjoy tax-free growth.

A 55-year-old earning $180K and expecting a modest retirement? A traditional IRA may offer better tax relief now and lower taxes later.

What about a regular brokerage account?

Roth IRA vs. brokerage account

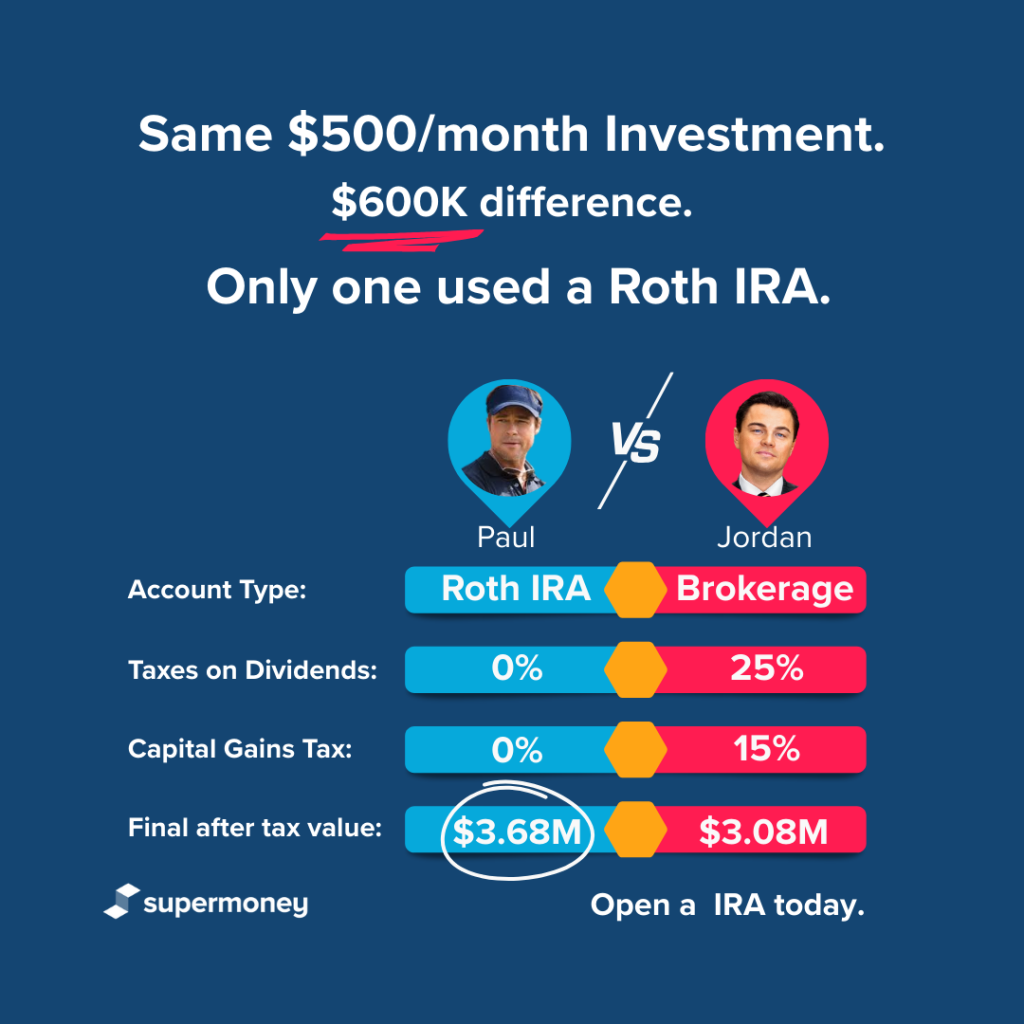

If you’re comparing a Roth IRA with a regular taxable brokerage account, the main difference is how your investments are taxed.

- Roth IRA: No taxes on investment growth or withdrawals (as long as you follow the rules).

- Brokerage account: You pay taxes on dividends and capital gains — either annually or when you sell.

In a Roth, you can buy and sell without worrying about a tax bill. In a brokerage account, even just rebalancing your portfolio can trigger taxes. Short- and long-term capital gains tax rates apply to profits from selling investments held outside of a tax-advantaged account.

Brokerage accounts offer unmatched flexibility

Taxable brokerage accounts don’t have income or contribution limits, and you can pull your money out whenever you like — for any reason. They’re perfect for medium-term goals, like saving for a home, or for investing beyond your IRA limits.

Roth IRAs are flexible too — you can access your contributions anytime, but not your earnings without penalties (unless you’re over 59½ and meet the 5-year rule).

Roth IRA vs. traditional IRA vs. brokerage account: key differences

| Feature | Roth IRA | Traditional IRA | Brokerage Account |

| Contributions | After-tax | Pre-tax (if deductible) | After-tax |

| Tax on growth | None | Tax-deferred | Taxed annually or on sale |

| Tax on withdrawals | None (qualified) | Taxed as ordinary income | Capital gains and dividend taxes |

| Contribution limit (2025) | $7,000 ($8,000 if 50+) | $7,000 ($8,000 if 50+) | No limit |

| Income limits | Yes | Limits for deduction | No |

| Withdrawal flexibility | Contributions anytime; earnings after 59½ | Penalties before 59½ | Anytime |

| RMDs | No | Yes (starting at age 73) | No |

| Best for | Tax-free retirement growth | Tax deduction now, lower taxes later | Flexible investing and mid-term goals |

WEIGH THE RISKS AND BENEFITS

Here is a list of the benefits and the drawbacks to consider.

Frequently asked questions

Can I contribute to both a Roth IRA and a brokerage account?

Yes! In fact, many investors do. Just remember the Roth IRA has annual limits, while the brokerage account doesn’t.

What happens if I take money out of a Roth IRA early?

You can always take out your contributions tax- and penalty-free. But if you withdraw earnings before age 59½ (or before meeting the 5-year rule), you may owe taxes and a 10% penalty.

What if I earn too much for a Roth IRA?

You may be able to do a backdoor Roth IRA — a legal strategy that involves contributing to a traditional IRA and converting it to a Roth. It works best if you don’t have other pre-tax IRAs.

Should I max out my IRA before using a brokerage account?

Generally, yes — especially if you’re eligible for a Roth. The tax benefits of an IRA typically outweigh those of a taxable account. After maxing your IRA, a brokerage is a great next step.

Key takeaways

- Roth IRAs offer tax-free growth and withdrawals, no RMDs, and some flexibility for early access.

- Traditional IRAs give you a tax break now but require RMDs and tax your withdrawals later.

- Brokerage accounts are the most flexible but come with annual tax obligations on gains and income.

- If you’re eligible, prioritize a Roth IRA for long-term savings — then use a brokerage account to invest more.

- Combining all three can give you tax diversification and greater control over your income in retirement.

Share this post:

Table of Contents