Bi-Weekly Mortgage Payments: Are They Worth It?

Last updated 03/11/2026 by

Jessica Walrack

The short answer is yes. Making bi-weekly mortgage payments is definitely worth it, if you can afford it. You will save thousands of dollars over the life of your mortgage and pay off your mortgage years earlier than with regular monthly payments.

The “normal” way to pay off a mortgage is to make one payment per month. But there are alternatives payment schedules, such as bi-weekly mortgage payments, which can save you money and help you pay off your balance faster. However, not all mortgage payment plans are worth your time. If you’re considering semi-monthly payments, you may be surprised by how little you will actually save.

Read on to learn more about semi-monthly and bi-weekly mortgage payments, and find out if which plan is right for you!

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

What are bi-weekly mortgage payments?

A bi-weekly mortgage payment plan splits your monthly mortgage payments in half. In other words, instead of making one payment at the end of each month, you’ll make half of that payment every two weeks.

Typically, you’ll set up an automatic withdrawal agreement so that each payment is automatically withdrawn from your bank account on the day that it’s due. Over the course of a year, you’ll make 26 payments. That’s the equivalent of 13 monthly payments — one more than you’d make with a traditional payment plan. Why is this the case? Because each month is slightly longer than four weeks. In other words, there are 52 weeks in a year, and 52 divided by two is 26.

What are semi-monthly mortgage payments?

A semi-monthly payment schedule involves making two payments per month instead of one. This adds up to 24 payments, which are the equivalent of 12 full monthly payments a year. Semi-monthly payments will save you a little in interest — since interest will never accrue for more than 15 days — but the savings are hardly notable. Over the life of a 30-year mortgage, you will only save a month’s worth of interest payments.

Are bi-weekly and semi-monthly payments the same?

Although they’re often mistaken for each other, bi-weekly payments and semi-monthly (or bimonthly) payments are not the same.

Semi-monthly payments split your monthly payment due in two payments, typically paid on the 1st and the 15th. Bi-weekly payments, on the other hand, are due every other week.

That means that after a year of semi-monthly payments, you’ll have made 24 payments (two for each month). After a year of bi-weekly payments, you’ll have made 26 payments (one for every two weeks).

As a result, bi-weekly mortgage payments can help you to pay down your mortgage faster, which can save you a lot of money over the life of the loan.

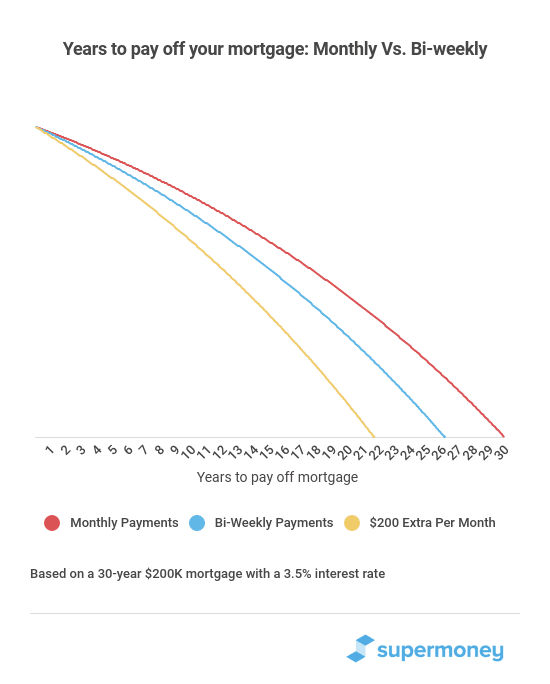

Here’s a quick cost comparison for a $200,000 mortgage with a 5% interest rate over a 30-year term:

| Mortgage Type | Interest Paid | Savings | Years to Repay Mortgage |

|---|---|---|---|

| Traditional Mortgage Payment | $186,512 | NA | 30 years |

| Semi-monthly Mortgage Payments | $186, 382 | ~$130 | 30 years |

| Bi-weekly Mortgage Payments | $151,788 | $34,724 | 25 years and 4 months |

As you can see, the bi-weekly payment plan offers significant savings when compared to a semi-monthly or traditional monthly plan.

Bi-weekly payments can also help you repay your mortgage faster. Obviously, the higher your interest rate, the greater the benefits of bi-weekly payments. However, even with lower interest rates, the benefits are substantial.

What if your lender doesn’t offer alternative payment options?

If you want a bi-weekly payment plan, but your lender doesn’t offer them, you still have options.

Third-party mortgage payment servicers

You may want to consider a third-party mortgage payment service company. How does it work?

Although individual offerings vary, generally speaking, you’ll pay the company bi-weekly or semi-monthly, and then they’ll pay your lender for you. However, if the facilitator is simply making your regular monthly payment while letting you split up your own payments, you might not be saving on interest. Plus, these services often involve monthly fees and a setup fee, which can further nullify your savings. It’s important to ask for details when considering working with a payment service company.

Do-it-yourself (DIY) bi-weekly payments

You can also structure your payments the way you want them yourself. If you’re going to make semi-monthly payments, start by getting one month ahead on your payments. Then, you can set aside half of your mortgage payment on the 1st and half on the 15th, and then submit both payments on the due date.As for a bi-weekly payment, just divide your monthly payment by 12 and make an additional principle-only payment each month. You can also save that amount all year and then pay it all toward your principal at the end of the year.However, before you take these steps, make sure that your payments won’t trigger any prepayment penalties. Also, be sure that they’ll be applied to your principal (not interest).Pros and cons of bi-weekly mortgage paymentsLet’s take a look at the pros and cons of bi-weekly payments overall.

WEIGH THE RISKS & BENEFITS

Here is a list of the benefits and the drawbacks to consider.

If a bi-weekly plan sounds like the right fit for you, contact your lender to find out if it’s available. If your lenders does not provide this service, consider other ways to save on your mortgage.

How else can you save on your mortgage?

Bi-weekly payments aren’t the only way to save on your mortgage. You can also:

Pay down your principal

In addition to your regular payment plan, you can opt to make extra payments to your principal at will. So if you find yourself with some extra income on a given month, consider using it to make an additional payment to your principal balance!

Refinance

Refinancing your mortgage is another excellent way to save. You may be able to refinance with the same lender or a new lender. The process involves taking out a new mortgage (ideally with lower interest and better terms) and using it to pay off and replace your existing mortgage.

Curious about what kind of rates and terms you could qualify for? SuperMoney makes it easy to find out if you’re a good candidate for a mortgage refinance. You can review home mortgage lenders side-by-side and compare their offerings here. Plus, read unbiased feedback from past customers.Your mortgage is likely the biggest loan you’ll pay off in your lifetime. Knowing your options and taking advantage of a better deal can save you big over the next few decades.Click here to compare mortgage lenders now.

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post:

Table of Contents