I’m a CFP With an 800+ Credit Score—Yet This Hidden Score Raised My Insurance Rates

Summary:

Even if you have an excellent FICO credit score, hidden insurance credit scores could be costing you money. These alternative credit scores—used by companies like LexisNexis—can significantly impact your home and auto insurance rates. I am CFP and have researched and written about credit scores and insurance at length, but I learned the hard way how my lower-than-expected insurance score was costing me in higher premiums. This is a deep dive in how insurance credit scores are calculated, and what you can do to improve them.

I’ve spent my career helping people understand credit. As a Certified Financial Planner (CFP), I know that a high FICO score (mine is in the 800s) is supposed to mean the best rates on everything—mortgages, loans, and yes, insurance.

At least, that’s what I thought.

One day, I saw an insurance ad promising to lower my home insurance premium by $600. I was skeptical—these offers usually sound too good to be true. But I always tell my clients to shop around for better rates once or twice a year, and it had been a while since I last compared policies.

So, I called.

And that’s when I got hit with the sticker shock. Instead of saving $600, I was quoted a premium nearly $700 higher than advertised.

Compare Home Insurance Providers

Compare multiple vetted providers. Discover your best option.

The reason? A score I had never even heard of.

The agent told me my insurance credit score was a 4 on a 1-to-10 scale—despite my 826 FICO score.

Confused and frustrated, I requested my insurance credit scores from LexisNexis, the company that provided them to my insurer. When I got my report, the numbers were shocking:

- LexisNexis RiskView Optics Score: 650

- LexisNexis Credit Score: 826

- SageStream Credit Optics Score: 535

I had never even heard of LexisNexis RiskView Optics or SageStream’s Credit Optics Score. Yet, these scores—completely separate from my FICO score—were making me look like a risky policyholder and driving up my insurance costs.

Why was my score so low?

I haven’t had an auto or home insurance claim in 5+ years. I have no missed payments, no collections, and a low debt-to-income ratio. Yet, my RiskView Optics Score and SageStream Credit Optics Score were alarmingly low.

I’m still waiting for my full LexisNexis and SageStream reports to pinpoint the issue, but I suspect it’s due to:

- Multiple credit card applications which can be a red flag (particularly in alternative credit models).

- Frequent address changes (many models associate stability with lower risk).

Alternative credit reports—especially those consumers rarely examine—are notorious for errors, sometimes even mixing up identities. I wouldn’t be surprised if I find incorrect or outdated information dragging down my score.

Understanding the components of an insurance score

Insurance scores, often derived from your credit history, are utilized by insurers to predict the likelihood of a policyholder filing a claim.

Key factors influencing these scores include:

- Payment History: Timely bill payments positively impact your score, while late or missed payments can decrease it.

- Outstanding Debt: High levels of debt relative to available credit can negatively affect your score

- Length of Credit History: A longer credit history provides more data on financial behavior, which can improve your score.

- New Credit Applications: Frequent applications for new credit within a short period may lower your score

- Types of Credit in Use: A diverse mix of credit accounts, such as mortgages, credit cards, and loans, can favorably influence your score.

Understanding these components empowers me to take proactive steps in managing my insurance score, potentially leading to more favorable insurance premiums.

What can you do about it?

If your insurance credit score is driving up your premiums, there are steps you can take to check, dispute, and improve your score. Many consumers don’t realize they can access and challenge their insurance credit reports just like traditional credit reports. Taking action now could help lower your insurance costs and ensure your information is accurate.

Here’s what I recommend:

- Check your insurance credit scores. More on what they are and why they matter below.

- Request a full report from any credit reporting agency where you have a low score. (Details on what qualifies as a low score below.)

- Dispute any errors or inaccuracies. Mistakes in your report could be costing you money.

Time required: About 20 minutes of your time.

Cost: Free.

The potential savings? Hundreds or even thousands of dollars in lower premiums and better rates.

What are insurance credit scores?

If a CFP with a near-perfect FICO score can get blindsided by insurance credit scores, how many others are unknowingly overpaying?

So, what exactly are these hidden scores? And why do they have so much power over your insurance premiums?

Insurance credit scores are different from the FICO or VantageScore models used by lenders. These scores are designed specifically to predict how likely you are to file an insurance claim. Many insurers rely on them to determine your premium.

Why do insurance companies use these scores?

Insurance companies argue that credit-based insurance scores help predict the likelihood of a policyholder filing a claim. Several studies, including research from the Texas Department of Insurance and the Federal Trade Commission (FTC), have found a strong correlation between lower credit scores and higher insurance claim amounts.

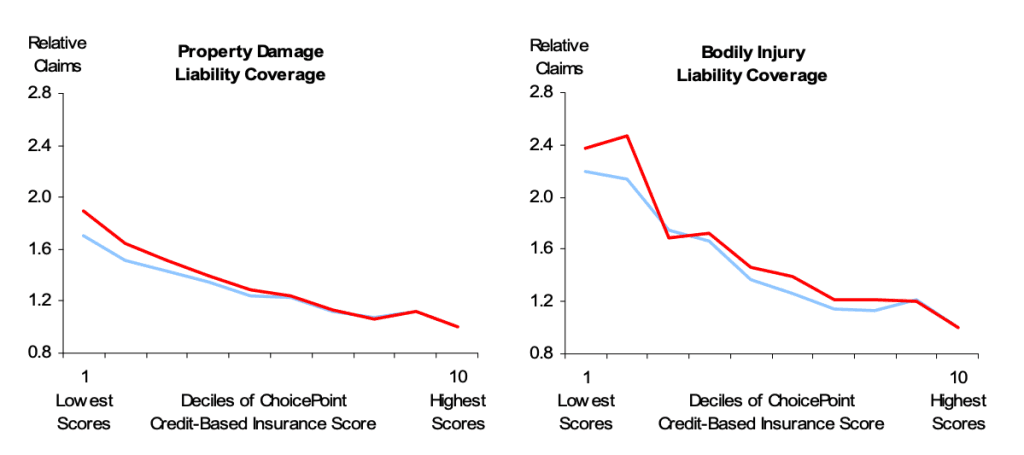

The chart below, based on FTC Automobile Insurance Policy Database analysis, illustrates this correlation across two major types of auto insurance coverage.

What do the graphs show?

Each chart plots relative claim amounts against ChoicePoint credit-based insurance scores, which insurers commonly use to assess risk.

- Lower scores (left side of the graphs) are associated with significantly higher claim amounts.

- Higher scores (right side) are linked to lower claim payouts.

- The red line represents claim costs without adjusting for other risk factors, while the blue line adjusts for factors like driving history, age, and location.

- Even after controlling for other risks, policyholders with lower credit-based insurance scores still tend to have higher claim payouts.

This data supports insurers’ argument that credit-based scores provide valuable predictive insight into insurance losses. They use this information to determine premiums, believing that lower-scoring individuals present a higher financial risk.

The impact of state regulations on insurance scores

It’s important to note that the use of insurance scores in determining premiums varies by state due to differing regulations.

For instance, some states have restrictions on how insurers can use credit information:

- California, Hawaii, and Massachusetts: These states have banned the use of credit-based insurance scores in determining auto insurance rates.

- Other States: Regulations may differ, with some states allowing limited use of credit information.

Steps to improve your insurance score

Improving your insurance score can lead to lower premiums.

Consider the following steps:

- Pay Bills on Time: Consistently making timely payments is crucial.

- Reduce Outstanding Debt: Aim to keep balances low relative to credit limits.

- Avoid Opening Multiple Credit Accounts Quickly: Limit new credit applications to avoid negative impacts on your score.

- Maintain Long-Standing Credit Accounts: Keeping older accounts open can positively affect the length of your credit history.

How do insurance credit scores differ?

Although the evidence linking credit scores and insurance claims is strong, there is a lot of variability among scores, as my own experience illustrates. Different scoring models analyze different factors, and insurers may use one or multiple scores when determining your premiums.

Here’s a breakdown of the most commonly used insurance credit scores and how they work:

| Score Type | Purpose | Key Factors | Score Range | Used For |

|---|---|---|---|---|

| LexisNexis RiskView Optics Score | Assesses financial stability and predicts risk | Public records, bankruptcies, liens, utility payment history | 250-850 | Auto and home insurance underwriting |

| LexisNexis Credit Score | Similar to a traditional credit score but tailored for insurance | Credit history from Equifax, Experian, TransUnion | Varies (often aligns with FICO score ranges) | Insurance pricing and underwriting decisions |

| SageStream Credit Optics Score | Focuses on alternative financial data | Cell phone payments, retail credit history, address stability | 300-999 | Auto insurance pricing, less widely known |

| FICO Insurance Score | Assesses a policyholder’s risk | Payment history, credit utilization, length of credit history, bankruptcies | 100-900 | Auto and home insurance underwriting |

| TransUnion Insurance Risk Score | Developed specifically for insurance underwriting | Credit behavior patterns, length and types of credit history, negative marks | 150-950 | Auto insurance pricing, sometimes used for home insurance |

How these scores differ from traditional credit scores

Unlike regular FICO or VantageScore, which predict the likelihood that you will repay debt, insurance credit scores estimate how likely you are to file a claim.

- They use some overlapping factors (like payment history and credit utilization) but apply different weightings.

- They may include non-traditional financial data (such as rental history, utility payments, and even address changes).

- These scores do not affect loan approvals or interest rates—only insurance pricing and eligibility.

Why do these differences matter?

Depending on which score an insurer uses, you may get very different quotes for the same coverage.

- If one insurer uses your FICO Insurance Score and another uses your LexisNexis RiskView Score, their risk assessment may vary significantly.

- Some insurers combine multiple scores or use proprietary versions of these models.

- If your traditional FICO credit score is excellent, but your SageStream or LexisNexis score is lower, you could still end up with higher insurance premiums.

Since insurance companies aren’t required to disclose which scores they use, it’s essential to check multiple scores and dispute errors where necessary.

How to check your insurance score

Unlike traditional credit scores, insurance scores are not always readily accessible to consumers.

However, you can:

- Request Your Score from Reporting Agencies: Some agencies, like LexisNexis, provide consumers with their insurance scores upon request.

- Review Your Credit Report: Since insurance scores are based on credit information, regularly checking your credit report can help you identify and correct inaccuracies that may affect your score.

Being proactive in monitoring your credit information can help you maintain a favorable insurance score.

How do insurance credit scores affect your rates?

Your insurance credit score can influence:

- Premium pricing: A lower score means higher insurance costs.

- Policy approval: Some insurers may decline coverage based on your score.

- Coverage options: Higher-risk customers may be offered fewer coverage choices.

For example, the Federal Trade Commission found that drivers with the lowest credit-based insurance scores were 1.7 times more likely to file claims than those with the highest scores.

Request your insurance credit scores

Just as you can request your traditional credit report from the major bureaus (Equifax, Experian, and TransUnion), you can also access your insurance credit scores. Insurers commonly use data from LexisNexis, SageStream, FICO, and TransUnion, so checking for errors or outdated information is essential.

You can request your insurance credit score reports directly from these providers:

- LexisNexis Consumer Portal – Provides reports on your RiskView Optics Score and other data insurers may use.

- SageStream Consumer Portal – Offers reports on your Credit Optics Score, which some insurers rely on.

- FICO Consumer Portal – Allows access to your FICO Insurance Score, which some insurers use to assess policyholder risk.

- TransUnion Consumer Portal – Provides reports on your TransUnion Insurance Risk Score, used for auto and home insurance pricing.

Additionally, since insurers sometimes reference traditional credit reports, it’s a good idea to review yours from the three major credit bureaus:

Under federal law, you’re entitled to one free credit report per year from each bureau at AnnualCreditReport.com.

Dispute inaccuracies

Errors on your insurance credit report can lead to higher premiums or even policy denials. If you find incorrect information—such as late payments you never made, incorrect account balances, or outdated personal details—you should dispute them immediately.

How to dispute errors on your insurance credit score

- Step 1: Review your report carefully for inaccuracies or outdated information.

- Step 2: Gather supporting documents (e.g., bank statements, credit card statements, proof of payments) to back up your dispute.

- Step 3: Contact the reporting agency using the dispute process for each provider.

Dispute process by provider

- LexisNexis & SageStream Disputes: File a dispute directly through their online portals or by phone. They are required to investigate and resolve errors within 30 days.

- FICO Insurance Score Disputes: Contact FICO customer service to request corrections to any reported discrepancies.

- TransUnion Insurance Risk Score Disputes: Submit disputes online through TransUnion’s dispute center.

- Credit Bureau Disputes: If your Equifax, Experian, or TransUnion report contains errors, you can file disputes online through each bureau’s website.

Once your dispute is resolved, your insurance credit score may improve, potentially lowering your rates.

Where to request and dispute your insurance credit scores

Below is a table with the contact details, addresses, and websites of the major insurance credit score providers and credit bureaus:

| Company | Contact Number | Mailing Address | Website |

|---|---|---|---|

| LexisNexis Consumer Center | (888) 497-0011 | P.O. Box 105108, Atlanta, GA 30348-5108 | consumer.risk.lexisnexis.com |

| SageStream (A LexisNexis Company) | (888) 395-0277 | P.O. Box 503793, San Diego, CA 92150 | sagestreamllc.com |

| FICO Insurance Score | (800) 777-2066 | 200 Smith Ranch Road, San Rafael, CA 94903 | fico.com |

| TransUnion Insurance Risk Score | (800) 916-8800 | P.O. Box 2000, Chester, PA 19016 | transunion.com |

| Equifax | (866) 349-5191 | P.O. Box 740241, Atlanta, GA 30374 | equifax.com |

| Experian | (888) 397-3742 | P.O. Box 4500, Allen, TX 75013 | experian.com |

Insurance score myths debunked

There’s a lot of misinformation about insurance scores. Here are some common myths and the truth behind them:

Myth: Checking your credit score will lower your insurance score.

Truth: Soft inquiries, such as checking your credit report, do not affect your insurance score.

Truth: Soft inquiries, such as checking your credit report, do not affect your insurance score.

Myth: Closing old credit cards will improve your score.

Truth: Closing accounts can shorten your credit history and lower your score.

Truth: Closing accounts can shorten your credit history and lower your score.

Myth: Your income impacts your insurance score.

Truth: Income is not a factor, but debt-to-credit ratio can influence your score.

Truth: Income is not a factor, but debt-to-credit ratio can influence your score.

Key takeaways

- Insurance companies use hidden credit scores—different from FICO and VantageScore—to determine your insurance rates.

- Even if you have excellent credit, your insurance credit score may be lower, leading to higher premiums.

- Major insurance credit scores include LexisNexis RiskView Optics Score, SageStream Credit Optics Score, FICO Insurance Score, and TransUnion Insurance Risk Score.

- These scores factor in public records, alternative financial data, and traditional credit history but weigh them differently than lender credit scores.

- Studies show a strong correlation between lower insurance credit scores and higher claim frequency, justifying their use in premium pricing.

- Insurance companies aren’t required to disclose which scores they use, making it critical to check your reports for errors.

- Errors on your insurance credit report can be disputed, just like traditional credit reports.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents