Below are some examples of when down payments might be considered illegal in regards to real estate.

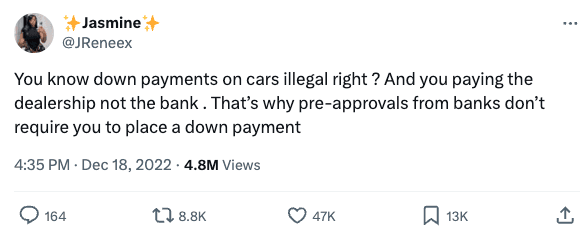

The reason you have a bunch of people thinking down payments being illegal seems to have originated from social media platforms, particularly TikTok. There has been a trend among users on car-related TikTok channels claiming that down payments for

vehicles are actually illegal. This misinformation has spread across various social media platforms, causing confusion and gaping mouths across the spectrum.

One article from The Autopian addresses this trend directly, stating that the idea of down payments being illegal is a piece of misinformation circulating on TikTok. It emphasizes that down payments are not illegal and highlights the benefits of making a down payment when

purchasing a vehicle, such as reducing the credit burden. Remember, in this day and age, misinformation and disinformation is all overt the place. However, it’s important to note that there is a fine line between combatting misinformation and censorship.

There are a few options to get a car with no down payment. For instance, you can steal the car. Joking! Here are the tried and trust ways to get a car with no down payment.

Improve Your Credit Score Elevating your credit score is essential for qualifying for a no down payment car loan, with a minimum

FICO score of 680 often required by lenders. If you’re below this threshold, enhance your score by regularly reviewing your credit reports, keeping track of your score, ensuring timely bill payments, and maintaining a

credit utilization ratio under 30%.

Consider Higher Monthly Payments Instead of a Down Payment

The amount of your down payment directly affects your monthly payments; a higher initial payment results in lower monthly charges. Alternatively, you can negotiate with lenders for higher monthly payments to bypass making a down payment. This approach usually leads to higher interest rates, increasing the total cost over the loan period.

For example, a $25,000 car loan at 5% interest over 72 months with a $5,000 down payment results in monthly payments of $322 and a total interest of $3,191. Without a down payment, the monthly payment increases to $403, with a total interest of $3,988.

Acquire a Co-Signer

Securing a co-signer with a strong credit score can be advantageous, especially if your credit is subpar. A co-signer commits to covering your loan if you default, impacting both parties’ credit scores negatively. Ensure all loan transactions are documented and select a co-signer you can rely on. Note that not all lenders accept co-signers, so it’s important to research and compare various lenders.

Explore Various Loan Offers

Loan conditions differ across lenders, affected by factors like location and market trends. It’s beneficial to compare offers from banks, dealership financing, credit unions, and online lenders, particularly those that provide loans without down payment requirements.

Opt for a More Affordable Vehicle

Selecting a car that fits your budget is key to obtaining a loan. If approval is challenging, consider choosing a less expensive vehicle. If you’re still unable to secure a loan, ask your loan specialist about the down payment amount needed to improve your chances.

Is getting a car with no downpayment a bad idea?

Opting for a

car loan without a down payment might seem financially convenient at first glance, especially for those short on immediate funds. However, this approach typically results in higher interest rates, as lenders perceive the loan to be riskier without upfront equity from the buyer. Consequently, the borrower faces higher monthly payments due to financing the full

purchase price of the vehicle, alongside any applicable fees and taxes. This not only increases the monthly financial burden but also amplifies the total amount paid over the life of the loan.

Moreover, the rapid depreciation of vehicles exacerbates the risk of

negative equity, where the loan balance surpasses the car’s value. This situation can lead to financial strain, particularly if the car is sold or totaled in an accident. Additionally, to counterbalance the absence of a down payment and manage higher monthly payments, borrowers may be compelled to extend their loan terms. While this strategy lowers monthly payments, it prolongs the interest payments, further escalating the total cost of owning the car. Ultimately, saving for a down payment before purchasing a car can significantly mitigate these financial drawbacks, ensuring a more economical and less burdensome car ownership experience.

FAQ

Can making a larger down payment affect my loan approval chances?

Yes, making a larger down payment can positively affect your loan approval chances. Lenders view a larger down payment as a sign of financial stability and lower risk, which can lead to more favorable loan terms, including lower interest rates and better approval odds.

Are there any benefits to financing a car through a dealership versus a bank?

Financing through a dealership can offer convenience and potential promotional financing rates that may be lower than what banks offer. However, banks might provide more personalized service and potentially better rates for customers with strong

banking relationships. It’s important to compare offers from both sources.

How does my credit score impact the interest rate on my car loan?

Your credit score is a critical factor in determining the interest rate on your car loan. Higher credit scores indicate lower risk to lenders, often resulting in lower interest rates. Conversely, lower credit scores may lead to higher interest rates due to perceived increased risk.

Is it possible to refinance a car loan with no down payment?

Yes, it is possible to refinance a car loan for which you made no down payment.

Refinancing can help you secure a lower interest rate or more favorable terms later on, especially if your credit score has improved or if market conditions have changed. However, the success of refinancing depends on factors like your car’s current value, your outstanding loan balance, and your creditworthiness.

Key takeaways

- Car down payments are not illegal, countering the misinformation spread on platforms like TikTok.

- In real estate and other transactions, the legality of down payments may depend on their source and how they’re disclosed, not the concept of down payments themselves.

- Options for acquiring a car with no down payment include improving credit scores, negotiating higher monthly payments, finding a co-signer, comparing loan offers, and selecting a more affordable vehicle.

- While no down payment car loans offer immediate financial relief, they can result in higher overall costs due to increased interest rates, loan amounts, and the risk of negative equity.