Where Is a Savings Bond Serial Number?

EA

Summary:

A savings bond is a type of bond purchased from the U.S. Department of Treasury that accrues compounding interest over one to 30 years They use a bond serial number to keep track of who the owner is. Bonds are available in paper and electronic forms. Each paper bond has a unique serial number in its bottom right corner. It’s important to keep a record of this number so that you can assess and control your bond throughout its lifetime.

It might seem like there are a million and one ways to save and invest your money. We’re here to break down your options for you. Savings bonds are a low-risk way to make your money work for you.

The lifetime of a savings bond can extend up to 30 years. It’s important to keep track of your bond information, like your serial number, over that time. Keep reading to learn about savings bonds, where you can find your bond’s serial number, and more.

Compare CD Accounts

Compare certificates of deposit. Discover your best option.

What are savings bonds?

A savings bond is a particular type of bond through which individuals can lend money to the government and receive compounding interest in return. Unlike regular bonds, savings bonds accrue interest that is paid out once you redeem the bond.

Many people use savings bonds as a secure way to save money and earn interest over time. Savings bonds are useful for saving for college, funding a startup, saving for retirement, and more.

How savings bonds work

When you buy a savings bond, you lend the government money. In return, they pay you interest. Earned interest compounds for 30 years or until you cash the savings bond. A savings bond cannot be resold or redeemed by anyone other than the owner.

You can buy a savings bond from the U.S. government’s Treasury Department in the form of a paper savings bond or electronic savings bond. Different types of savings bonds come with different limits.

Pro tip

The more time a savings bond spends maturing, the more compound interest you earn. When buying a savings bond, consider how much money you can put away for the most time to maximize your returns. For example, if you’re planning on buying a home in the next five years, tying up the money you need for a down payment in a savings bond isn’t the best idea. If you want to save for your child’s education in 20 years, a savings bond can be a great tool to do so.

Types of savings bonds

There are two types of savings bonds issued in the United States. While similar, each has its advantages. You can purchase both types of savings bonds electronically through the U.S. Treasury’s website. These bonds are backed by the “full faith and credit” of the U.S. government. This means that, as long as the government keeps paying its debts and meeting its financial obligation, investors will receive what the bond terms promise them.

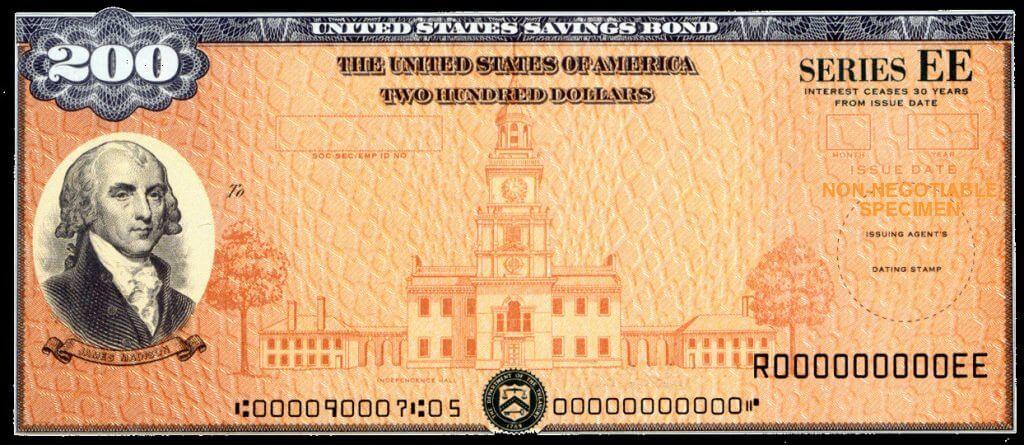

1. Series EE bonds

Series EE bonds, which become unattractive when inflation is high, are securities that have been sold by the U.S. Treasury since 1980. Any Series EE bond issued after May 2005 earns semiannual interest installments paid at fixed rates. In the right circumstances, they can be good for people wanting their money to work for them with minimal risk.

Regardless of the rate, the bond’s value doubles from its purchase price to its par value (face value) 20 years after the bond’s issue date. This guaranteed doubling means any Series EE bond held for 20 years will have an effective interest rate of 3.5%.

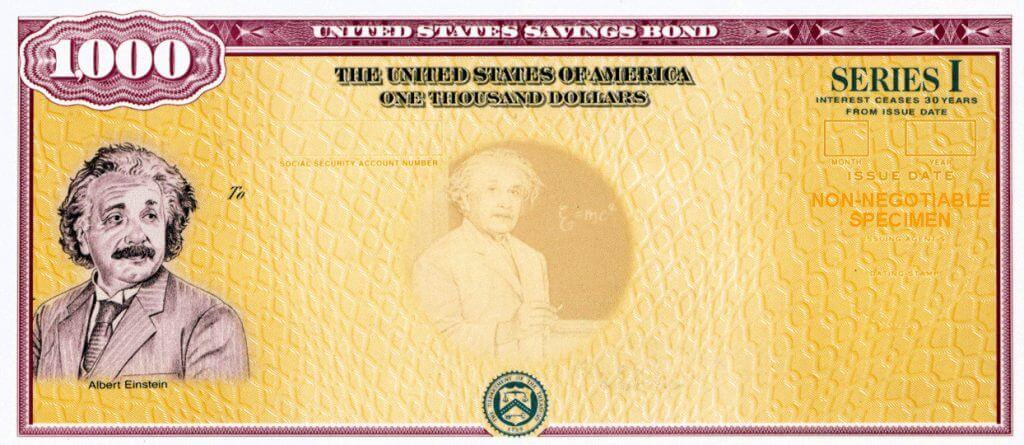

2. Series I bonds

Series I bonds are attractive because they help protect your money from inflation. The interest earned on I bonds depends on a combination of a fixed rate and an inflation rate. The fixed rate stays the same for the lifetime of the bond. The inflation rate adjusts twice per year. You can only buy series I paper bonds when you file your federal income taxes. You can purchase electronic bonds anytime.

Another vehicle of interest to safety-first investors

Safety-focused investors who gravitate toward government bonds also often find certificates of deposit an appealing way to earn a safe return on money they can set aside for a set period.

Redeeming savings bond funds

One year after purchasing a savings bond, the owner can cash it in. However, with both series, any bond cashed in before five years of maturity loses the last three months of interest payments. Obviously, the longer you hold a savings bond, the more interest it accrues. The maximum term is 30 years.

When you’re ready to redeem an electronic savings bond, you can do so through the Treasury Department’s TreasuryDirect website. You can redeem paper bonds at most banks or credit unions or by sending them to the U.S. Treasury. To redeem a bond, you’ll need the bond itself, proof of identity, and, in special cases, proof that you are the named beneficiary for the bond.

Pros and cons of savings bonds

Pro tip: boost your finances with the right tools

The right tools can give your finances a major boost. Check out SuperMoney’s comparisons for money management tools:

Where to find the savings bond serial number

Thirty years is a long time to keep track of a piece of paper. It’s important to know your savings bond serial number in case the bond gets lost or damaged. The serial number can also help you calculate the value of your bond and find other important bond information.

On paper savings bonds, the alphanumeric serial number is located in the bottom right corner. It should be a 10-digit code containing letters and numbers. It’s important to keep a record of this number.

When you buy a new savings bond, write the serial number down and keep it in a safe, easy-to-remember place. You never know when you’ll need it throughout the lifetime of your bond.

Recovering lost or damaged savings bonds

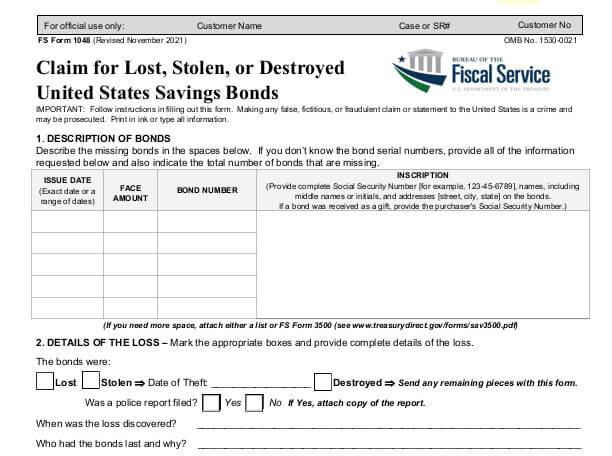

You can use your bond serial number to recover, replace, or transfer savings bonds. If your paper bond is lost, stolen, or destroyed, you’ll need to file a claim with FS Form 1048. Required on this form are some key pieces of information about your bond. You must provide sufficient information to verify ownership and recover the bond.

Form 1048 asks for the bond serial number. If you don’t have it, you’ll be required to submit your month and year of purchase, Social Security number, name, and address. You must sign the form in the presence of an authorized certifying officer at a bank, trust company, or credit union. The U.S. Treasury Department will then reissue your bond electronically.

You can also convert paper bonds to electronic bonds for easy tracking and monitoring of your securities. Keep your account information and bond serial number and follow instructions on the U.S. Treasury website to make the easy switch.

Savings bond calculator

Whether you’re considering cashing out or you’re just curious, it’s helpful to know what the current value of your savings bond is. Your bond serial number isn’t mandatory to find this out, but it makes it more simple and easy. TreasuryDirect has a savings bond calculator tool that makes it easy to find out the exact value of your savings bond.

Navigate to the savings bond calculator tool on TreasuryDirect.gov. You can find it under “Resources & Tools,” or click here to go straight to it. Enter the series type, denomination, and issue month and year. Click “calculate,” and it will show you your exact bond valuation. If you don’t have your serial number, you can omit it from the calculator. It will still give you an estimated value based on the series, denomination, and issue date.

FAQ

What is a bond serial number?

A bond serial number is a unique alphanumeric code that identifies a savings bond.

Can you look up bonds by serial number?

Yes, you can look up bonds by serial number on the U.S. Department of Treasury’s website.

How much is a $50 bond worth after 30 years?

A $50 EE bond purchased 30 years ago would be worth $103.68 today. Note that the face value of the bond is the guaranteed value after 20 years, which is twice the purchase price — $25 in this case.

Curious about how this interest could compound for larger amounts of money? Read about how much interest one million dollars could earn.

How do I verify a bond?

You can verify a bond using your personal information and the bond’s serial number.

How can I check the value of a bond?

You can check the value of a bond through TreasuryDirect, the online hub of U.S. Treasury savings bonds. Check your electronic bonds directly or use their savings bond calculator tool to check the value of your paper bond. You’ll need to provide identifying information like your bond serial number, series type, issue date, and par value.

How do I trace a savings bond?

If you need to track or transfer a savings bond, look it up on the U.S. Treasury Department’s website using the serial number. If you don’t know the serial number, you may be able to trace a savings bond using your Social Security number and other bond information.

Do savings bonds expire?

The maturity date of a savings bond is 30 years after the issue date. Savings bonds stop accruing interest when they reach their maturity date. At that point, you can withdraw your principal and interest earnings. The bond won’t expire if you don’t redeem it right away. You can also cash in a savings bond between one and 30 years after its issue date. If you redeem a savings bond between one and five years of age, you are subject to a penalty equal to three months of interest.

Key takeaways

- Savings bonds are a safe saving method through which you lend the government money in exchange for compounding interest payments. Series I and EE are the two types of savings bonds, each with different characteristics.

- It’s important to keep records of all your financial assets, physical or electronic. If you have a paper savings bond, make sure to note its serial number and keep it in a safe place. The serial number is in the bottom right corner of the bond certificate.

- Use the savings bond certificate to verify your bond, access bond information, calculate the bond’s valuation, and replace a lost paper bond.

Portfolio building begins here

It’s never too early or too late to start building a savings and investments portfolio. Read about some alternative investments that can help you get to your savings goals sooner.

Related reading: As already noted, another safe savings option is a certificate of deposit or CD. Read How To Open a Certificate of Deposit (CD) to learn more.

Share this post: