Does Medicare Check Your Bank Account?

Last updated 09/02/2024 by

Andrew Latham

Summary:

Medicare will usually check your bank accounts, as well as your other assets when you apply for financial assistance with Medicare costs. However, eligibility requirements and verification methods vary depending on what state you live in. Some states don’t have asset limits for Medicare savings programs. Find out what Medicare checks (and doesn’t check) when determining eligibility for financial assistance programs.

Most people qualify for Medicare when they reach 65, but only those with low incomes and limited assets will qualify for financial assistance with their Medicare premiums, deductions, or prescription costs. Unfortunately, the income and asset limits to qualify for financial assistance with Medicare are rather low, which is why many may be tempted to fudge or not disclose the balance in their accounts. Moral considerations aside, is that a good idea? Does Medicare check your bank accounts?

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Does Medicare look at your bank account?

The short answer is yes. However, the auditing standards of Medicare assistance programs can vary a lot by state.

In the past, auditing of applicants was more hit and miss. Nowadays, the states that manage Medicare assistance programs usually verify the income and assets of individuals using automated verifications systems and third-party vendors. Even if the Centers for Medicare & Medicaid Services (CMS) don’t always pick up every account you own, it is smart to act as if they will.

Note that some states, such as Alabama, Arizona, Connecticut, Delaware, Mississippi, New York, Oregon, Vermont, and the District of Columbia, do not have asset limits for Medicare Savings Programs. However, assistance that is organized by federal programs, such as Extra Help (see below for details), will require asset verification.

Another thing to consider is that eligibility for Medicare financial assistance programs is often tied to eligibility for other federal programs, such as Supplemental Security Income, disability, and retirement benefits, which have their own asset verification systems. If you qualify for those programs, qualifying for Medicare Savings Programs can be much easier.

Do you need a bank account to apply for Medicare?

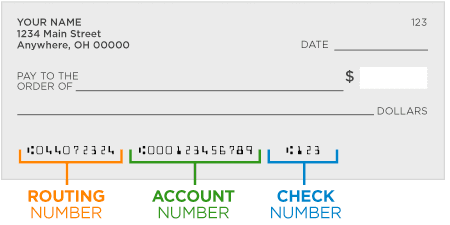

When you apply for Medicare, you’ll need to provide information about yourself, which includes details on at least one bank (or credit union) account. Medicare will need to know your bank’s routing transit number — the first 9 numbers at the bottom of a check — and your account number — the second set of numbers at the bottom of your check (10 to 12 digits).

If you are looking for a checking account, here are a few to consider.

What information will Medicare need?

As well as your bank account information, you will also need to provide the following when you apply:

- Your date and place of birth and Social Security number.

- The name, Social Security number, and date of birth or age of your current spouse and any former spouse. You should also know the dates and places of marriage and dates of divorce or death (if appropriate).

- The names of any unmarried children under age 18, age 18-19 and in elementary or secondary school, or disabled before age 22.

- Your citizenship status.

- Whether you or anyone else has ever filed for Social Security benefits, Medicare or Supplemental Security Income on your behalf (if so, we will also ask for information on whose Social Security record you applied).

- Whether you have used any other Social Security number.

- If you are applying for retirement benefits, the month you want your benefits to begin.

- If you are within 3 months of age 65, whether you want to enroll in Medical Insurance (Part B of Medicare).

To determine eligibility for help with prescription and other costs, the Social Security Administration will request details about your income and resources and those of your spouse if you’re married. The government will usually not require you to provide any documents as proof unless there are questions down the road. However, the following documents will help you complete forms when applying for financial assistance:

- Social Security card.

- Bank account statements, including checking, savings, and certificates of deposit.

- Individual Retirement Accounts (IRAs), stocks, bonds, savings bonds, mutual funds, other investment statements.

- Tax returns.

- Payroll slips.

- Most recent Social Security benefits award letters.

- Statements for Railroad Retirement benefits, Veterans benefits, pensions, and annuities.

How does Medicare’s asset verification systems (AVS) work?

There isn’t a one-size-fits-all answer to this question since each state has its own methods for assessing eligibility and verifying assets. Also — not surprisingly — Medicare programs don’t publicize the details of their fraud detections protocols. However, most states implement asset verification programs and periodically reverify beneficiary resources, including assets, when determining eligibility. As of 2021, 46 states have implemented electronic asset verification systems.

Systems vary by state, but they typically work something like this.

- The state government will set up a contract with vendors to establish and operate portals between state eligibility systems and banks or other third-party systems with electronic access to financial information.

- State eligibility workers then submit requests through the state’s AVS portal, which queries financial institutions for information on accounts in the applicant’s name. Information on applicant assets is then returned to states to be considered part of the eligibility determination process.

- The requests are sent to large, national banks, banks within a set distance of the applicant’s address, and specific banks identified by the applicant in their application. Some states also perform property checks through their AVS.

So, although it is less likely that Medicare will pick up accounts in your name if they are in another country or a small bank in another state, there are no guarantees. Obviously, it is safer to work on the assumption that the government knows about all your accounts.

What are the income and asset limits for Medicare assistance programs?

Medicare Savings Programs (MSPs) help people with low incomes and limited assets pay for premiums, deductibles, copayments, and coinsurance associated with Medicare. Each state has its own eligibility requirements and methods for counting your income and resources. So, you should check with your state Medicaid office to see if you qualify. Here is a summary of the requirements of some of the most widely used programs.

| Program | Assistance | Income limit | Asset Limit |

|---|---|---|---|

| Qualified Medicare Beneficiary (QMB) Program | Deductibles and coinsurance for both Medicare Part A and Part B | up to $1,094 per month ($1,472 for couples) | $7,970 for an individual and $11,960 for a couple |

| Specified Low-Income Medicare Beneficiary (SLMB) Program | Payment of premiums for Part B | up to $1,308 per month.($1,762 for couples) | $7,970 for an individual and $11,960 for a couple |

| Qualified Individual (QI) Program | Payment of premiums for Part B (not as generous as SLMB) | up to $1,469 per month ($1,980 for couples) | $7,970 for an individual and $11,960 for a couple |

| Extra Help | Paying for your prescription drugs | $19,320 a year ($26,130 for married couples) | $14,790 for an individual or $29,520 for a couple |

Qualified Medicare Beneficiary (QMB) Program

This program helps to pay Medicare Part B premiums and copayments. It can also assist with deductibles and coinsurance for both Medicare Part A and Part B.

- A single person can qualify for the program in 2021 with an income of up to $1,094 per month.

- A couple can qualify with a combined income of $1,472 per month.

- The asset limits are $7,970 for an individual and $11,960 for a couple.

Specified Low-Income Medicare Beneficiary (SLMB) Program

This program helps to pay premiums for Part B.

- A single person can qualify in 2021 with an income of up to $1,308 per month.

- A couple can qualify with a combined income of $1,762 per month.

- The asset limits are $7,970 for an individual and $11,960 for a couple.

Qualified Individual (QI) Program

This program helps pay Part B premiums but is not as generous as the Specified Low-Income Medicare Beneficiary Program.

- In 2021 a single person can qualify with an income of up to $1,469 per month.

- A couple can qualify with a combined income of $1,980 per month.

- The asset limits are $7,970 for an individual and $11,960 for a couple.

Note that income limits to qualify for programs vary in Alaska and Hawaii. You can check the income limits in those states by visiting the Social Security Administration website.

Full benefit dual-eligible (Medicaid and Medicare)

If you qualify for both Medicaid and Medicare, you can receive additional benefits. Additional benefits include assistance at home services, nursing care, and certain prescription drugs not covered by Medicare Part D plans. Note that beneficiaries who only meet the income and asset requirements of the Medicare Savings Program are considered partially dual eligible and will receive assistance with Medicare costs, but not additional Medicaid benefits.

Extra Help

Beneficiaries who qualify for any of the Medicare Savings Programs mentioned above will also qualify for a program called Extra Help. This program is designed to help with paying for your prescription drugs. The good news is you don’t have to be in a state-run Medicare assistance program to qualify for help paying for your prescriptions under Extra Help. You can qualify as long as your annual income in 2021 as an individual is below $19,320 ($26,130 for married couples); you may be eligible. Asset limits in 2021 are up to $14,790 for an individual or $29,520 for a couple.

What does Medicare consider as assets when determining eligibility for financial assistance?

The Centers for Medicare & Medicaid Services (CMS) determine eligibility for Medicaid and the Medicare Savings Programs by considering assets such as money in checking or savings accounts, bonds, stocks, or mutual funds. They also consider part of the value of assets such as

vehicles, life insurance policies, and the value of any real estate other than your home.

vehicles, life insurance policies, and the value of any real estate other than your home.

However, some resources aren’t considered assets, such as:

- Your primary residence.

- One car.

- Household goods and wedding/ engagement rings.

- Burial spaces.

- Burial funds up to $1,500 per person.

- Life insurance with a cash value of less than $1,500.

- Some states may exclude other types of assets as well.

Key takeaways

- Although Medicare may not always pick up every account you own, they typically use sophisticated automated verification tools for auditing applications.

- It’s a good idea to assume that Medicare can (and eventually will) know about all your accounts when applying for income or asset-based assistance.

- Eligibility requirements and asset verification methods vary by program and state.

- Not all resources are considered assets for Medicare purposes.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents