What is an Adjustable-Rate Mortgage?

Last updated 05/18/2026 by

Andrew Latham

An adjustable-rate mortgage (ARM) is a loan that has an interest rate that can change over time. If interest rates drop, so does your monthly payment. But if interest rates rise, your monthly payment does as well.

Here are some key facts to know about adjustable-rate mortgages when you consider buying a home:

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

Adjustable-Rate Mortgage vs. Fixed-Rate Mortgage

How does an adjustable-rate mortgage work?

An adjustable-rate mortgage is different from a fixed-rate mortgage because, as the name suggests, its rate will fluctuate depending on prevailing interest rates. The interest on fixed-rate mortgages does not change over time.

Most ARMs consist of an initial period (during which the rate remains steady) plus an adjustable period (during which the rate is subject to change).

The difference between the two types of mortgages is the way the loans are structured. A fixed-rate mortgage has an interest rate that does not change over the course of the loan. Because of that, the amount of the monthly payment you make is also fixed for the duration of the loan.

The interest rate on an ARM, however, is based on a market index rate plus a specific amount, called a margin. The index rate is set by a third party. It is often based, for example, on the rate tied to a one-year US Treasury bill or the London Interbank Offered Rate (LIBOR). These rates will change over time. The margin, or a second layer of interest added to those rates, is predetermined by the lender when the mortgage is issued and does not change.

For example, the interest rate on an ARM could be 1.5% (index rate) plus 3 percentage points (the margin), to equal 4.5% for a given year. That will change over time as the index rate fluctuates.

One thing to keep in mind is that there are maximums and minimums on ARMs that protect against massive swings in the interest rate. For example, a periodic rate cap limits how much the rate can differ from one year to the next. A lifetime rate cap limits how much the rate can rise over the full term of the loan.

What are the pros and cons of an Adjustable Rate Mortgage (ARM)?

The benefit of a fixed-rate mortgage is that you know what you’re getting into. There are no surprises, no matter if interest rates in the market rise or fall. Your monthly payments are well-known in advance.

This benefit, however, can also be its downside. Having a fixed rate means that if interest rates fall, you are likely to be paying more for your loan than you would if you had waited.

That flexibility is one of the potential benefits of an adjustable-rate mortgage. If interest rates decline, so will your monthly payments. But remember, this is a gamble. If interest rates rise, you are likely to end up paying more than the amount you had planned.

The other benefit of an ARM is that during the initial period, the interest rate on an ARM is typically lower than for a fixed-rate mortgage.

To compare an ARM with a fixed-rate mortgage, look at “indexes, margins, discounts, caps on rates and payments, negative amortization, payment options, and recasting (recalculating) your loan,” the Federal Reserve suggests.

The most important thing is to ask yourself what works best for your financial situation. If you’re planning to pay your loan in a few years, an ARM may be a smart choice. However, if you are likely to take 15, 20, or 30 years to repay the loan, a fixed-rate mortgage may be a safer option.

Different Types of ARMs

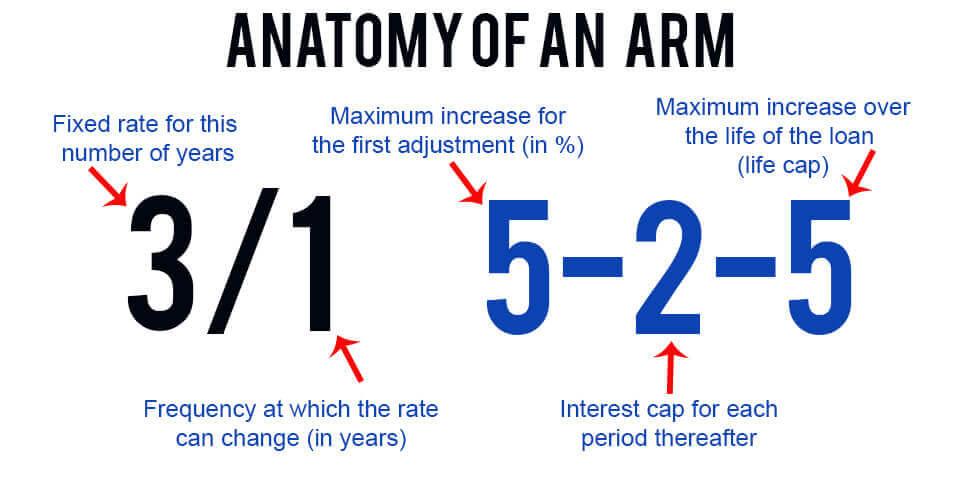

As you conduct your research, be aware that there are different types of adjustable-rate mortgages. You will want to familiarize yourself with them. The most popular types of adjustable-rate mortgages are the 3/1 ARM and 5/1 ARM. The first number represents the number of years that the initial period of a fixed interest rate will last. The second number indicates the frequency in years that the rate is subject to change.

For example, 3/1 and 5/1 ARMs have fixed interest rates for the first three and five years, respectively. Their rates are then adjusted each year after that.

Some lenders offer variations on this, including 7/1 and 10/1 ARMs.

An ARM may also have a 5-2-5 cap structure. The first number signals the largest amount that the interest rate can adjust after the initial fixed period. The second number represents the cap on the interest rate rise from one adjustment period to another. The last number is a lifetime cap or a limit on how much the interest rate can increase over the life of the loan.

In the case of the 5-2-5 loan, the interest rate could change by a maximum of 5 percentage points after the initial fixed period. After that, the interest rate can change by a maximum of 2 percentage points for each adjustable period. The most the interest rate could change over the lifespan of the loan is 5 percentage points, which is indicated by the final number.

Which kind of ARM is the best for you?

Ultimately, whether a fixed-rate mortgage or an adjustable-rate mortgage is right for you depends on a number of factors. If you decide to choose an ARM, the best type for you will depend on your unique financial situation – especially how much you’re able to pay on a monthly basis. To choose the right ARM, you must also consider whether you believe interest rates are set to rise in the next few years and by how much. Only by studying your options and knowing your current financial picture can you make the right choice.

When you’re ready to find best mortgage lenders out there, check out SuperMoney’s list here.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Table of Contents