How to Get the Best Mortgage Interest Rate

S

Last updated 03/20/2024 by

SuperMoneyWhen you apply for a mortgage loan, one of the most important factors in your payments is the interest rate. To illustrate, consider a home that is worth $284,000, which was the median sales price of a new home in the United States for August 2016 (source). An interest rate of 3.5% over 30 years would cost you $175,100 in interest. A hike of 0.5% on the same loan would cost you an extra $29,000 in interest over the life of the loan.

However, it’s not just a matter of finding the bank with the lowest rates. Some mortgage lenders advertise low rates, but not everyone qualifies for those. Additionally, some offers are just introductory rates, also known as teaser rates, that go up after a few months. Here’s everything you need to know about finding the best possible mortgage rates.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How are Interest Rates Determined?

All mortgage lenders establish their rates based on the prime interest rate. This rate is determined by the federal government. It represents the best rate banks charge each other for borrowing money overnight. Only the largest companies with the best credit ratings qualify for the actual prime interest rate. Consumers usually get a Prime Plus rate, such as Prime Plus 5, which means the current prime interest rate plus 5 percentage points. If you know the current prime rate, you will find it easier to compare the rates mortgage lenders quote.

How Do Interest Rates Affect Your Payment & Getting a Home Loan?

Let’s begin with the obvious. The higher the interest rate the higher the mortgage payment. For instance, if we use the same 30-year mortgage of $284,000 we used above, a 4% interest rate would mean a monthly payment of around $1,355. The same mortgage with a 5% interest rate would cost you around $1,525 a month. That is a $170 a month. Notice these examples don’t include taxes or insurance premiums.

It may seem like lower interest rates always make it easier to get a mortgage, but it’s a little more complicated than that. Although lower interest rates do make it cheaper to buy a home, it typically isn’t the biggest challenge for potential buyers. Often, the biggest difficulty is finding the cash to put a downpayment on a home. This is particulalry true for renters who want to get a mortgage. Another issue to consider is that lower mortgage rates are often a symptom of a weak economy. In other words, home sales can slow down even if interest rates are low.

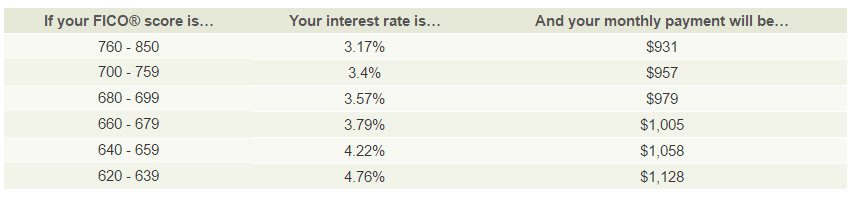

How Does Your Credit Score Affect the Mortgage Interest Rate You’re Offered?

Lenders offer lower interest rates to buyer who have a higher credit score. No surprises there. But how much more should someone with a mediocre credit score expect to pay when compared to someone with excellent credit? There isn’t a universal standard. Every lender has its own risk assessment methods. However, the table below provides a good estimate of the rates you are likely to get, as of October 2016, on a $216,000 30-year fixed rate mortgage based on your FICO score.

Source: myFICO.com

Notice that a homebuyer with a poor credit score (under 640) pays a 1.59% premium when compared with someone who has an excellent FICO score (above 760). This amounts to paying a monthly $197 bad credit penalty.

How Can You Improve Your Credit Rating for a Better Mortgage Rate?

If your credit score disqualifies you for a home loan or makes your interest rate too high to afford, don’t despair. Bad credit is not a life sentence. You can fix it. Improving your credit takes time, but it’s doable. First, make sure to make all your payments on time, including credit cards, rent, car payments, and utility bills. Next, pay down your credit card balances. Higher balances drive up your debt to income ratio, which lowers your credit score. Fixing your credit score before buying a home means paying less and getting more.

What Other Factors Go Into Finding the Best Mortgage Rates?

Several things can drive your interest rate up or down. The interest rate you’re offered depends amonth other things on:

The type of loan — Mortgages either have a fixed or an adjustable rate. Fixed-rate mortages lock you into a single rate for the life of the loan. Adjustable-rate mortgages, also known as ARMs, fluctuate. ARMs usually start with a lower introductory rate that remains fixed for up to a year. Once the introductory period is over, the rates could rise or drop depending on the interest rate index your bank chooses to use.

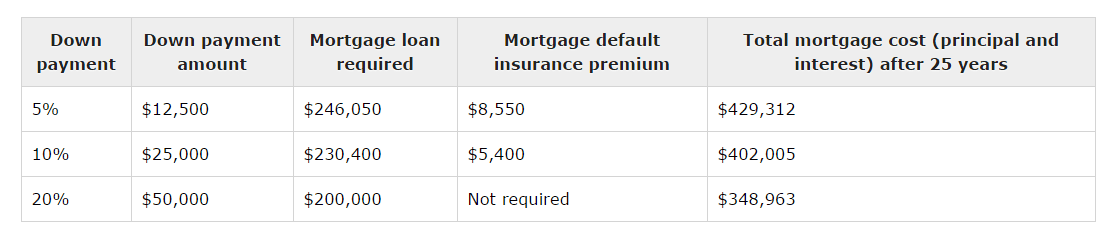

Your downpayment — Paying a larger downpayment will reduce the size of the mortgage you need, which will save you money in interest. You may also avoid paying for a private mortgage insurance, also known as mortgage default insurance premium.This is an insurance lenders typically require in the case of homebuyers who pay a downpayment of less than 20% the property’s value. The table below provides three mortgage scenarios based on the size of the downpayment on a 25-year mortgage of $250,000.

Source: Financial Consumer Agency of Canada

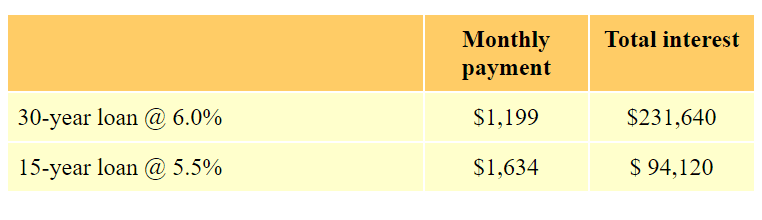

The length of your mortgage — Usually, shorter term loans qualify for lower interest rates. All things being equal, a 15-year mortgage is usually cheaper than a 30-year mortgage. In fact, reducing the term of your mortgage is one of the best ways to pay less interest. For instance, compare the total cost of a $200,000 mortgage at 6% with a 30-year mortgage to a fixed-rate loan 15-year mortgage with a 5.5% interest rate.

Source: Federal Reserve Board

Notice how choosing a 15-year mortgage instead of a 30-year mortgage could save you $137,520 in interest on a $200,000 property.

What Types of Mortgage Loans are Available to You?

There are several types of loans available.

First-time home buyers’ programs offered through HUD. Even if your name has been on a home mortgage before, you still might qualify. These programs sometimes have lower rates and easier requirements to help new homeowners get into their first homes.

FHA loans are popular for those looking for low down payments. These loans are also available to those with lower credit scores than for traditional loans.

VA loans are offered to military members or veterans and their families. These come with low or no down payments and certain protections for those who get behind on payments.

USDA loans are available to certain buyers in rural areas. These loans also require no or low down payments and come with help for those who fall behind on their payments.

Why is Getting Pre-Approved for a Home Loan Important?

Pre-approval for a home loan is proof to home sellers that you have the financing needed to buy the home. Sellers often accept contracts from pre-approved buyers before they accept higher offers from buyers who aren’t approved. Don’t confuse pre-qualified with pre-approved. Pre-qualified is not a guarantee you’ll get the loan. Pre-approval is a guarantee.

Is It Okay to Shop Around for the Best Mortgage Rates?

The short answer is yes. There is nothing wrong with talking to several lenders, finding out what each offers, and picking the option that’s right for you. Just make sure you confine your rate-shopping to a 14-day window. Why? Credit score algorithms consider credit inquiries from mortgage lenders within a two-week period as a single inquiry, which will only have a minimal effect on your score. However, if you spread out your mortgage applications over a longer period, your credit score will take a bigger hit.

Should You Consider ‘Paying for Points’?

Points are fees paid up front to qualify for a lower interest rate. Points are worth about 1 percent of the total mortgage. For example, on a $100,000 loan, a point would be $1,000. Paying for points is worth it if you keep the mortgage in place for a long time. But if you sell that home or refinance your loan within just a few years, it may not be worth the cost. Lenders may also offer negative points. Negative points are when the lender lowers their fees in order to charge a higher interest rate. Negative points can get expensive when you keep the loan for a long time.

Besides Interest Rate, What Else Affects Your Mortgage Loan Payments?

The federal interest rate, your credit score, and the lender you use all affect your interest rate. But those aren’t the only factors that go into a mortgage payment. In summary, your loan payments are based on:

- The buying price of your home

- The downpayment you make at closing

- Your closing costs (usually about 3 percent of the total mortgage) Whether your mortgage payments include property taxes and homeowners insurance

- Whether you get optional insurance, a warranty, or guarantee

- Costs for any incidentals included in your mortgage loan, such as title searches, property inspections, etc.

How Much Should You Expect to Pay in Closing Fees?

Closing costs are usually about 3 percent of the cost of the mortgage. It’s okay to shop around for the lowest closing costs. Don’t confuse closing costs with your down payment. Closing costs help pay real estate agent(s), real estate attorneys, and costs for researching and closing the loan. This includes things like title searches, property inspections and appraisals, and related costs. Your down payment goes directly toward the price of the home. The closing costs do not.

How To Get the Best Mortgage Rate?

- Compare apples to apples. Ask for a statement of the potential costs and loan’s terms from every lender you consider. This will help you to get a feel of the total cost of each mortgage offer.

- Shop around before you commit to a lender. Just make sure you apply for all your mortgages within a two-week period to minimize the impact on your credit score.

- Talk to a professional mortgage broker and ask her to create a set of scenarios to help you compare the pros and cons of each type of mortgage available to you.

- Consider all the variables, such as whether the interest rate is fixed or adjustable, whether the payments include insurance and taxes. Paying for points or making a larger downpayment could also save you money.

Are you ready to begin your search for mortgage lenders? Find the best mortgage companies here .

Share this post: