What is a DSCR Loan? Debt Service Coverage Ratio Definition and Examples

Summary:

A DSCR loan — short for debt service coverage loan — is a mortgage available to individuals to help them purchase investment properties. Whereas traditional mortgage lenders review your income to determine your eligibility, DSCR lenders instead look at the investment property’s cash flow.

Real estate has long been one of the most popular investment opportunities for Americans. In fact, a recent Gallup poll found that 41% of Americans believe that real estate is the best long-term investment, beating out stocks and other popular investments.

Unfortunately, real estate investing isn’t accessible to everyone. Unlike investing in the stock market, buying an investment property requires a huge upfront expense, and loans for investment properties can be difficult to qualify for.

One option that’s available to a real estate investor is a DSCR loan, which someone can qualify for without meeting all of the requirements of a traditional mortgage. Keep reading to learn why this type of loan might be a good idea.

What is a DSCR loan?

A debt service coverage (DSCR) loan is one that qualifies borrowers through an investment property’s cash flow rather than the borrower’s income. DSCR loans — also known as investor cash flow loans — are frequently used by real estate investors to qualify for mortgages and buy investment properties.

What is a debt service coverage ratio?

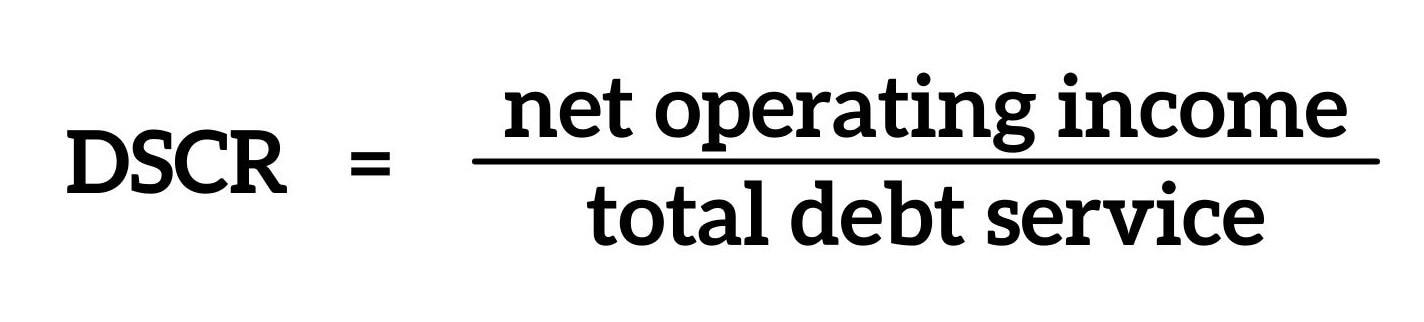

Before we dive further into how DSCR loans work, let’s back up a few steps and talk about the debt service coverage ratio (DSCR). The DSCR is the ratio of an investment’s net operating income to its total debt service. It’s a way of determining whether a borrower has enough cash flow to pay its current debt obligations.

Here’s how DSCR is calculated:

DSCR can have applications in business, government, and personal finances. Like DSCR loans, this ratio is often used in real estate to determine whether an investment property’s cash flow can cover its mortgage payments.

The higher the DSCR, the better the ratio. A DSCR above 1 means that an investment property has positive cash flow and enough net operating income to cover its debts. A DSCR below 1 means it has a negative cash flow, and not enough income to pay its debts. As a general rule, anything above 1.25 is considered a good DSCR.

How DSRC loans work

When you apply for a mortgage loan, your lender usually looks at your income to determine how much you can afford as a monthly payment. The key figure lenders look at is your debt-to-income ratio (DTI), which is the percentage of your monthly income that goes toward debt.

But in the case of investment properties, some lenders offer DSCR loans. Rather than looking at a borrower’s income, the lender takes into account the expected monthly rent from the property. And instead of using the DTI to determine eligibility, lenders look at the DSCR.

If the rental income is more than enough to pay the mortgage payment, then the borrower may qualify. If the rental income won’t cover the mortgage payment, the lender will probably deny the application.

DSCR loan requirements

While DSCR loans may not have the exact same requirements as conventional mortgages, there are still guidelines real estate investors will have to meet to qualify.

Unlike conventional mortgages, DSCR mortgages aren’t backed by entities like Fannie Mae and Freddie Mac. Therefore, there are no standardized requirements. However, there are a few things your lender will look at.

- DSCR. Generally speaking, lenders require a DSCR between 1 and 1.5 to qualify for a DSCR loan, with the most common minimum requirement being a DSCR of 1.25.

- Credit score. Each lender will require a specific credit score, with minimum requirements typically ranging from 620 to 700.

- Down payment. Most DSCR loans have a maximum LTV of 80% — you’ll need a down payment of at least 20% to qualify.

- Cash reserves. Like other investment properties, DSCR loan lenders require a certain amount of cash reserves, often equal to six months of payments.

- Loan amount. The maximum you can borrow for a DSCR loan depends upon your lender, but many financial institutions offer loans up to $2 million.

- Prepayment penalty. Unlike conventional loans and typical investment property loans, many lenders charge prepayment penalties on DSCR loans.

- Property eligibility. DSCR loans can generally be used for investment properties with one, two, three, or four units.

Pro Tip

You’ll notice that even though your income isn’t a factor when qualifying for a DSCR loan, your credit score still is. You’ll need a certain credit score to qualify, and this can impact the interest rate you’re eligible for.

Want to streamline the process of improving your credit score? You can check your credit report with the three national credit bureaus once a year for free but you may want to invest in a credit monitoring service if you are actively trying to improve your score. These companies can help you track your credit reports and find ways to improve your credit score. For instance, you may find negative credit items that are not accurate that can be disputed.

DSCR loan example

Let’s say you’re considering buying a rental property with a price tag of $300,000. Based solely on your annual income, you won’t be able to qualify for the loan. After all, you have your own monthly housing payment to cover. Instead, you look into a DSCR loan.

The lender you’re applying with requires a 20% down payment, meaning that you would be putting down $60,000 and financing the remaining $240,000. With a 6% interest rate, your monthly mortgage payment would be $1,438.

You believe you could rent out the property for $2,100 per month. Using the DSCR calculation and dividing the property’s income ($2,100) by its monthly payment ($1,438), you find there’s a DSCR of 1.46%. This is great news since it means you can qualify for the loan.

In reality, there would be more that goes into this calculation. In addition to the monthly principal and interest payments, the DSCR calculation would also include other expenses like property taxes, homeowners insurance, and more.

Pro Tip

Not sure how to calculate the DSCR for your prospective investment property? Many lenders offer DSCR calculators on their websites where you can input your net operating income and expenses to determine your property’s DSCR.

Pros and cons of DSCR loans

DSCR loans come with several key benefits, but there are also some downsides that real estate investors should be aware of.

Key Takeaways

- A DSCR loan is an investment property mortgage that allows borrowers to qualify based on a property’s rental income, rather than their personal income.

- DSCR — debt service coverage ratio — is used for investment properties but also other areas of business, government, and personal finance.

- Common DSCR loan requirements include a minimum debt service coverage ratio, credit score, cash reserves, down payment, and more.

- DSCR loans make it easier for people to buy rental properties since they don’t look at a borrower’s income. However, these loans also have some downsides, including higher interest rates and larger down payments.

Erin Gobler is a Wisconsin-based personal finance writer with experience writing about mortgages, investing, taxes, personal loans, and insurance. Her work has been published in major outlets, such as SuperMoney, Fox Business, and Time.com.

Table of Contents