How To Raise Your Credit Score Without a Credit Card

JA

Summary:

There are other ways to raise your credit score if you can’t get your hands on a credit card. For example, you could become an authorized user on someone else’s credit card or take out a small personal loan to establish a credit history. It’s important to note that these methods will all take time since building your credit is not an overnight process. However, if you take consistent action and stay patient, you’ll eventually see positive results.

Raising your credit score when you can’t qualify for a good credit card can be frustrating. And if you have little to no credit history, you may find yourself in a catch-22 situation when it comes to building credit — because how can you build credit if no one is willing to give you credit in the first place?

But don’t worry, you’re not doomed. Thankfully, building an excellent credit score is still possible without access to a credit card.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

1. Get a credit builder loan

Credit builder loans are exactly what they sound like — they help build your credit. When you have a thin credit file or no credit, it may be difficult to get approved for a loan. For this reason, you may want to start with a credit builder loan, which has less stringent eligibility requirements.

When you apply for a credit builder loan, the lender (typically a bank or credit union) provides you with a small loan amount that you repay in monthly installments over a certain period of time. The catch is that you don’t receive the funds upfront. Instead, they’re placed into a separate savings account or certificate of deposit (CD) account and won’t be released to you until you’ve made all your payments. In the meantime, your on-time payments are reported to the credit bureaus to help boost your credit score.

Errors on your credit report can hurt your credit score, so it's essential to regularly review your credit report and dispute any errors you find. — Cyrus Vanover, financial expert and founder of The Frugal BudgeterClick to Tweet

2. Become an authorized user

Most credit card companies allow their customers to assign an authorized user who can access the account holder’s credit line without being responsible for making monthly payments. By becoming an authorized user, you can essentially piggyback off the account holder’s good credit to boost your own credit score.

However, it’s worth noting that if the main cardholder fails to make on-time payments and maintain a positive payment history, your credit score could suffer.

3. Stay current on your private or federal student loans

If you took out a private or federal student loan, you could boost your credit score simply by making on-time payments and not defaulting on the loan. So, if you’re straight out of college and have little to no credit, start by focusing on paying down your student loans.

And if you’re not financially stable enough to make payments on your student loan, contact the loan servicer as soon as possible to discuss payment plan options. This way you can avoid damaging your credit score with late or missed payments.

4. Use rent payments

Another way to boost your credit score without a credit card is to ask your landlord to report your rent payments to the credit bureaus. If your apartment’s property management uses third-party solutions like PayYourRent and RentTrack, it should be easy to report your rent payments to the three major credit bureaus. This would allow you to build credit with bills you’re already paying.

You could also look into services like Experian Boost, which tracks your bill payments each month. You may even be able to track your rent and utility payments, further increasing your score.

5. Consider car loans or personal loans

Your credit mix is an important factor that affects your credit score. By having a healthy mix of different credit types, you indicate to future creditors that you can manage various forms of credit responsibly.

So, if you need a car or need to finance a big-ticket purchase, consider taking out a car loan or a personal loan instead of paying with cash or a credit card. Just make sure that you can repay your loan before committing to it.

6. Apply for a secured credit card

While secured credit cards function a lot like regular credit cards, they require you to pay a cash deposit upfront to guarantee your credit line. This deposit serves as a guarantee to the credit card issuer that they will receive their money back if you fail to make your payments.

You can think of secured credit cards like traditional credit cards with training wheels. By using a secured credit card responsibly and making payments on time, you can establish a positive credit history and eventually qualify for unsecured cards with higher credit limits.

7. Check your credit report for errors

Another way to improve your credit score is by checking your credit report for errors. Cyrus Vanover, financial expert and founder of The Frugal Budgeter, says, “Your credit report contains information about your credit history, including your payment history, outstanding debts, and other financial information. Errors on your credit report can hurt your credit score, so it’s essential to regularly review your credit report and dispute any errors you find.”

Fortunately, you don’t have to do this alone. If you want help reviewing your credit report, you can hire a credit repair company to look for errors on your behalf.

Pro Tip

If you don’t know where you stand in terms of your credit health, head to AnnualCreditReport.com to request a free copy of your credit reports from the three credit bureaus — Experian, Equifax, and TransUnion. You’re entitled to one free copy annually from each credit bureau.

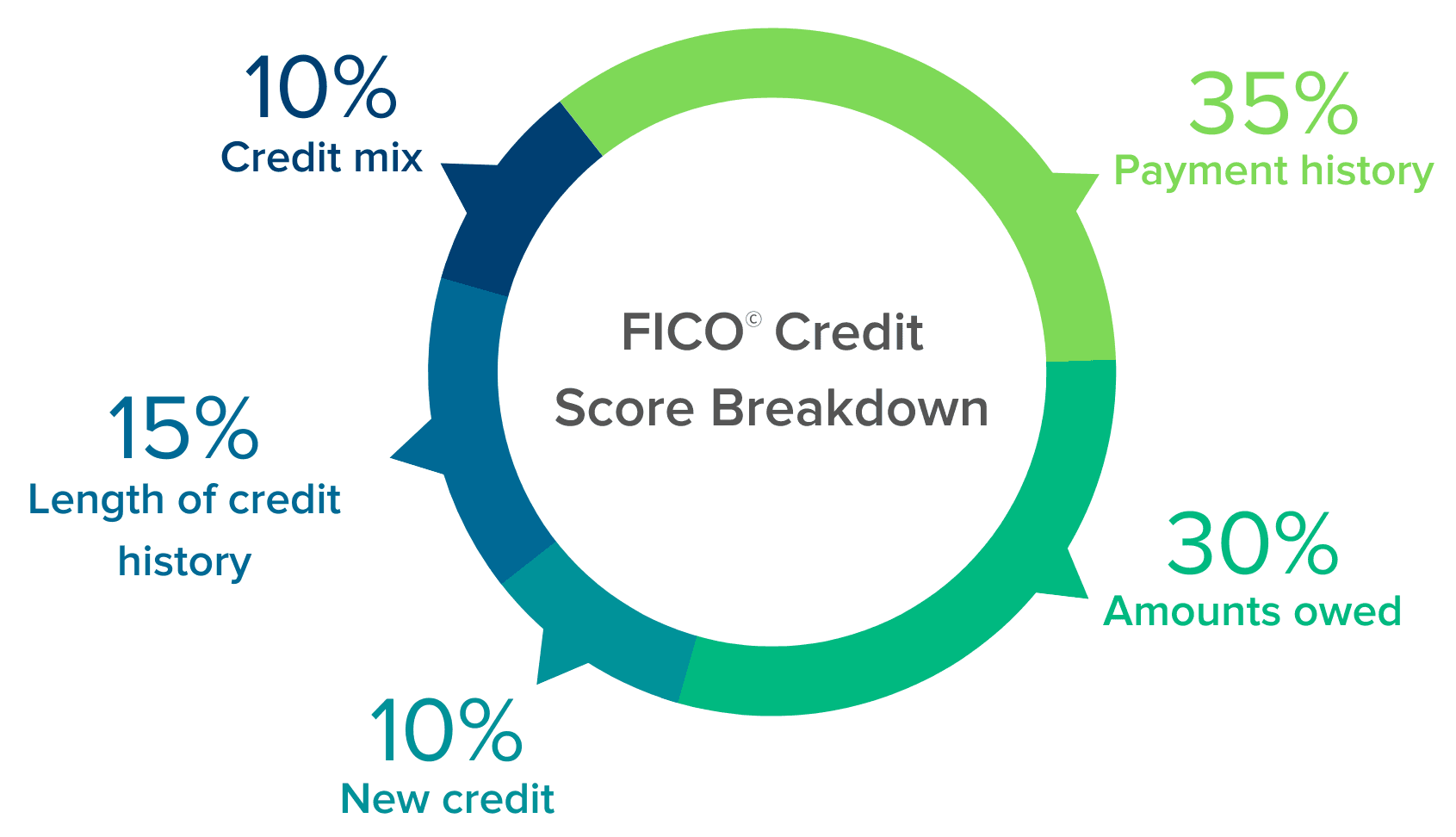

Factors that affect your credit score

Before taking steps to improve your creditworthiness, you should know what factors influence how high (or low) your credit score is.

As you can see, your payment history and credit utilization both greatly impact your score. This is why certain installment loans (like a credit builder loan) can be a great way to build credit. However, these factors aren’t the only pieces of the puzzle.

Related reading: To learn more about your credit score and how you can quickly improve it, take a look at our article on just that.

FAQs

How fast can you raise your credit?

According to Equifax, one of the three major credit bureaus, the amount of time it takes to boost your credit score will depend on your unique situation. But in general, you could see changes in your credit score as early as between 30 and 45 days if you’ve taken the correct steps to improve your creditworthiness.

However, if you have multiple negative items, such as late payments on your credit report, it could sometimes take over a year to notice the positive impact on your credit score.

How can I raise my credit in 30 days?

You could begin see to gradual improvements to your credit score in 30 days if you make the effort to build good credit habits. However, remember that you likely won’t see any dramatic changes in just a month since good credit is the result of excellent financial habits you maintain over a long period of time.

What is the fastest way to boost your credit score?

While it may be tempting to search for the fastest way to improve your credit score, the reality is that improving your creditworthiness is a long-term process that requires consistent effort. There’s no shortcut and no instant fix.

What you can do, though, is adopt healthy financial habits that will gradually improve your credit score. This could include paying down your existing debt, keeping your credit utilization low, and making all your payments on time. These small actions will add up and eventually help you reach that credit score you desire. So, don’t get discouraged by the lack of instant results.

Key Takeaways

- Ways to raise your credit score without a credit card include getting a credit builder loan, becoming an authorized user, and staying current on student loans. You could also use rent payments to build your credit, take out car or personal loans, and apply for a secured credit card.

- Factors that affect credit score include payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit applications (10%).

- It could take between 30 to 45 days to see changes in your credit score by building good financial habits.

- You could have a credit score without owning a traditional credit card since creditors like mortgage lenders can also report your information to the three main credit reporting agencies.

Boost your credit with the right tools

Building your credit takes time and commitment. By sticking to good credit habits, such as making on-time payments and keeping your credit utilization low, you’ll eventually see the improvements you desire.

If you’re ready to boost your credit score, consider looking into some of the best personal loans for rebuilding credit. These loans report to the three major credit bureaus and don’t require good credit to qualify.

Share this post: