Record Number of Households Only Making Minimum Payments as Delinquencies Rise

Last updated 04/28/2025 by

SuperMoney Team

Edited by

Andrew Latham

Summary:

A record-high share of U.S. households are now making only minimum payments on their credit cards, reflecting growing financial stress as inflation and borrowing costs remain elevated.

New data from the Federal Reserve shows that American consumers are increasingly struggling with credit card debt. A record percentage of households are making only the minimum payment on their balances — a sign that financial pressure is intensifying. Combined with a spike in late payments, this trend could signal broader economic trouble ahead.

Take control of your financial future

SuperMoney's AI-powered budgeting and personalized financial insights help you reduce financial stress and achieve your goals faster.

Minimum payments hit a record high

More households are now making just the minimum payment on their credit cards than ever before. This behavior often indicates financial stress, as it suggests borrowers cannot afford to pay down their balances significantly.

The data shows a steady climb starting around 2022, reaching over 11% of households in early 2025. High interest rates and stubborn inflation are major contributors to this trend.

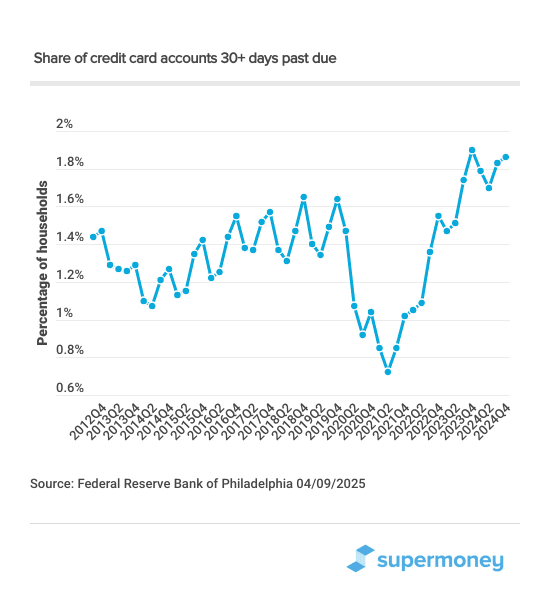

Late credit card payments are surging

Making only minimum payments is not the only red flag. The percentage of credit card accounts 30 days or more past due is also rising sharply, suggesting that many households are falling behind on their obligations.

This spike in delinquencies could foreshadow future increases in defaults, creating risks not only for individual households but for the broader banking system.

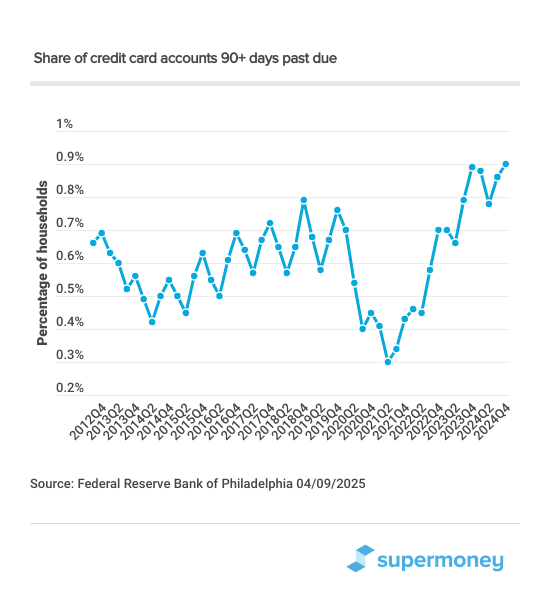

Serious delinquencies are climbing

Even more concerning, the number of accounts that are 90 days or more past due is also rising quickly. Serious delinquencies have nearly tripled since 2022.

Serious delinquency is often a leading indicator of financial crises at both the household and systemic levels. If left unchecked, this trend could lead to greater credit tightening and slower economic growth.

What does this mean for the economy?

These growing signs of strain are not just personal finance concerns — they could have national economic consequences. When more consumers fall behind on debt, banks often tighten lending standards, making it harder and more expensive for households and businesses to borrow. With consumer spending driving nearly 70% of U.S. economic activity, restricted access to credit can quickly slow growth.

Higher delinquencies also raise concerns about financial stability. Smaller banks and lenders heavily exposed to consumer debt could face mounting losses if defaults continue rising. In a worst-case scenario, this strain could ripple through the economy, tightening credit further and amplifying a downturn.

In short, mounting credit card stress isn’t just a household problem — it’s a flashing warning sign for the broader economy.

What can consumers do?

Consumers struggling with high-interest credit card debt have several options to ease financial stress. Typically, the best first step is to build a realistic budget and try to increase income. Consumers can also lower costs by combining multiple higher interest debts into a debt consolidation loan at a lower fixed interest rate, simplifying repayment and reducing total interest costs.

Another option is a balance transfer credit card, which can temporarily eliminate interest charges and help pay down debt faster if used carefully. Homeowners may also consider home equity financing, such as home equity loans, lines of credit, and shared equity agreements, which typically offer lower rates by using home equity as collateral. However, it’s important to weigh the risks, such as fees, potential credit score impacts, or putting your home at risk if payments are missed.

Key takeaways

- A record share of households are making only minimum payments on credit card balances.

- Delinquencies (30+ days and 90+ days) are rising sharply.

- Financial stress among households could have broader economic implications.

- High inflation and interest rates are major factors driving this trend.

Feeling overwhelmed by money worries?

SuperMoney's AI-powered budgeting tools help you track your money goes, set realistic goals, and reduce financial stress.

Share this post:

Table of Contents