Using 401k To Pay Off Credit Card Debt Cares Act

Last updated 12/03/2024 by

Benjamin Locke

Edited by

Andrew Latham

Summary:

Using a 401(k) to pay off credit card debt is a significant financial decision that can impact your future retirement. This article explains the implications of accessing retirement funds, including penalties, taxes, and alternatives, while considering temporary provisions under the CARES Act.

Dealing with mounting credit card debt can be overwhelming, especially when high-interest rates make repayment seem impossible. Many consider tapping into their 401(k) accounts as a solution. While this might offer immediate relief, the long-term impact on retirement savings is substantial. This article provides a comprehensive guide to understanding the pros, cons, and alternatives of using a 401(k) to address credit card debt, while revisiting the temporary changes introduced by the CARES Act.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is a 401(k)?

A 401(k) is a retirement savings plan offered by many employers in the United States. It allows employees to save and invest a portion of their paycheck before taxes are taken out. These plans are named after the section of the U.S. Internal Revenue Code that governs them. Here’s an overview of how a 401(k) works:

How a 401(k) works

Understanding the key features of a 401(k) is essential for effective retirement planning. Here’s how it works:

- Tax advantages: Contributions to a traditional 401(k) are made with pre-tax dollars, reducing your taxable income for the year. The earnings on your investments grow tax-deferred, meaning you don’t pay taxes until you withdraw funds in retirement.

- Employer match: Many employers offer a matching contribution up to a certain percentage of your salary, essentially providing free money to boost your retirement savings.

- Investment options: Participants can choose from a range of investment options, including mutual funds, stocks, and bonds, tailored to their risk tolerance and retirement goals.

Types of 401(k) plans

There are two main types of 401(k) plans, each with unique benefits:

| Type | Description |

|---|---|

| Traditional 401(k) | Contributions are made with pre-tax dollars, reducing taxable income. Withdrawals in retirement are taxed as ordinary income. |

| Roth 401(k) | Contributions are made with after-tax dollars, meaning you pay taxes upfront. Qualified withdrawals in retirement are tax-free. |

Withdrawal rules

Withdrawals from a 401(k) are generally allowed once you reach age 59½. Early withdrawals are subject to income tax and a 10% penalty unless specific exceptions, such as hardship withdrawals, apply. The CARES Act temporarily waived some of these penalties, but those provisions have since expired.

Contribution limits

The IRS sets annual limits on how much you can contribute to a 401(k). For 2024:

- Employee contribution limit: $22,500 (or $30,000 for individuals age 50 and older).

- Total contribution limit: $66,000, including employer contributions.

What is the cares act, and how did it change 401(k) rules?

The CARES Act, passed in March 2020, provided financial relief during the COVID-19 pandemic. Among its key provisions was a temporary relaxation of 401(k) withdrawal rules, allowing individuals to access retirement savings to address financial hardships.

Key changes under the CARES Act

- Penalty-free withdrawals: Allowed up to $100,000 in withdrawals without the standard 10% penalty.

- Tax flexibility: Taxes on the withdrawn amount could be spread over three years instead of being due in the year of withdrawal.

- Repayment option: Withdrawn funds could be repaid within three years to avoid taxes altogether.

Options for using a 401(k) to pay off credit card debt

There are three main ways to access funds from your 401(k) account to manage credit card debt:

1. 401(k) loans

Many employer-sponsored plans allow participants to borrow against their accounts. Here’s how they work:

- You can borrow up to 50% of your vested balance, with a maximum of $50,000.

- The loan must be repaid within five years, with interest paid back into your account.

- Repayments are typically deducted from your paycheck.

| Advantages | Disadvantages |

|---|---|

| Interest is paid back to your account, not a lender. | If you leave your job, the loan may become due immediately. |

| No impact on credit score. | Failure to repay the loan converts it into a taxable distribution. |

| No early withdrawal penalty. | Missed investment growth during repayment. |

2. Hardship withdrawals

Hardship withdrawals allow you to access funds for immediate financial needs, such as preventing eviction or paying for medical expenses. However, credit card debt is rarely considered a qualifying hardship.

3. Early withdrawals

Taking an early withdrawal from your 401(k) before age 59½ typically results in a 10% penalty in addition to income tax on the withdrawn amount. This should be considered a last resort due to its significant financial impact.

Impact on your retirement savings: Real-life examples

Accessing your 401(k) to repay debt is a significant decision that goes beyond immediate financial relief. While it may reduce high-interest debt, the long-term effects on your retirement savings can be substantial. Below are two scenarios demonstrating how withdrawing or borrowing from your 401(k) can impact your future financial security.

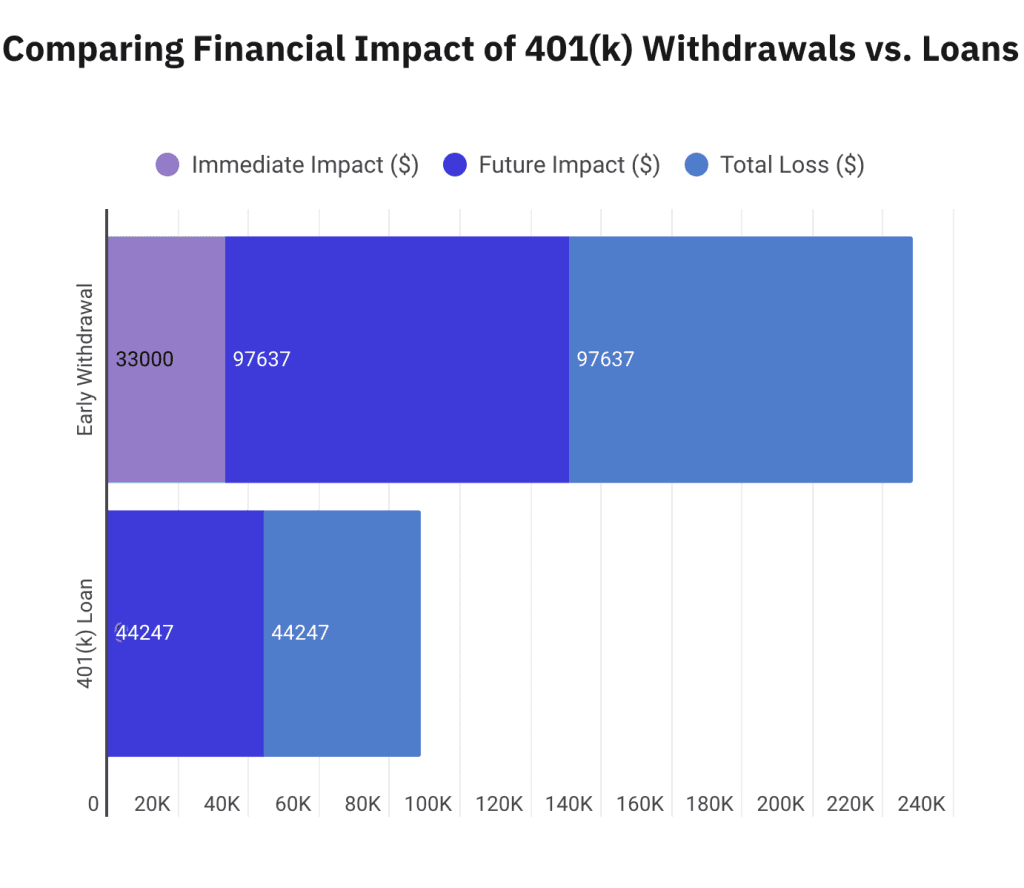

Scenario 1: Early withdrawal

Taking an early withdrawal from your 401(k) before age 59½ incurs penalties and taxes, immediately reducing the amount you receive.

Suppose a 35-year-old withdraws $50,000 from their 401(k) with a balance of $150,000, an income tax rate of 24%, and an annual return of 6%. While the withdrawal provides $33,000 to address debt, the long-term cost is nearly $100,000 in lost retirement savings. This highlights why early withdrawals should be a last resort for debt repayment.

Scenario 2: 401(k) loan

Borrowing from your 401(k) can avoid penalties and taxes but comes with other risks. Using the same $50,000 withdrawal scenario, consider the case of a loan with a 5% interest rate, repaid over five years.

A 401(k) loan avoids the immediate financial burden of penalties and taxes, but missed growth during repayment still results in a long-term loss of $44,247. While less damaging than an early withdrawal, it’s essential to repay the loan promptly to minimize financial impact.

Understanding the financial impact

Tapping into your 401(k) can provide immediate relief, but it also comes with long-term consequences. Here’s what you need to consider:

Alternatives to 401(k) withdrawals for managing credit card debt

Before tapping into your retirement account, consider these alternatives:

Debt consolidation loans

A debt consolidation loan allows you to combine multiple high-interest debts into a single loan with a lower interest rate. This can simplify payments and reduce the total interest paid over time.

Balance transfer credit cards

Many credit card issuers offer 0% APR promotions for balance transfers. Transferring high-interest debt to one of these cards can save you money if you can pay off the balance before the promotional rate expires.

Debt management plans

Nonprofit credit counseling agencies can negotiate lower interest rates and manageable payment plans with your creditors. These plans require discipline but can be an effective way to get out of debt.

Negotiating with creditors

Many creditors are willing to negotiate lower interest rates or offer settlement options if you’re struggling to make payments. This can be a less costly option than tapping into your 401(k).

| Alternative | Pros | Cons |

|---|---|---|

| Debt consolidation loan | Lower interest rates; simplified payments. | Requires good credit; may involve fees. |

| Balance transfer card | 0% APR promotional period. | Fees; promotional rate expires after a set time. |

| Debt management plan | Lower interest rates; structured payments. | Requires commitment; potential impact on credit score. |

| Negotiating with creditors | Reduces interest or balances owed. | Not guaranteed; may impact credit score. |

FAQ

What are the penalties if I cannot repay a 401(k) loan?

If you fail to repay a 401(k) loan, the remaining balance is treated as a taxable distribution. This means you’ll owe income taxes on the amount, and if you’re under 59½, you’ll also face a 10% early withdrawal penalty. These penalties can add up quickly, significantly reducing your retirement savings.

Are there exceptions to the 10% early withdrawal penalty?

Yes, the IRS allows exceptions to the 10% penalty for specific situations, such as permanent disability, certain medical expenses exceeding 7.5% of your adjusted gross income, or if you are separated from your job after age 55. These exceptions help reduce the financial burden for qualifying individuals.

How do I determine if using my 401(k) is the right choice?

Evaluate your financial situation by considering alternatives like debt consolidation or balance transfer cards. Compare the costs of withdrawing from your 401(k), including penalties and missed growth, against other options. Consulting a financial advisor can help you make an informed decision tailored to your goals.

Can I use my 401(k) to consolidate multiple debts, or is it only for credit card debt?

You can use 401(k) funds for any purpose, including consolidating multiple high-interest debts like medical bills or personal loans. However, the financial impact, including taxes and penalties, applies regardless of the type of debt being paid off.

How does withdrawing from a 401(k) affect my employer match?

Withdrawing funds doesn’t impact your employer match directly, but it reduces the balance eligible for matching contributions to grow. Additionally, if you leave your job, any outstanding loan balance may become immediately due, putting your employer-matched funds at risk if the loan is not repaid.

Key takeaways

- Accessing your 401(k) to pay off credit card debt can provide immediate relief but may have significant long-term financial consequences, including lost retirement savings.

- The CARES Act temporarily allowed penalty-free withdrawals, tax flexibility, and repayment options, but these provisions expired at the end of 2020.

- Alternatives such as debt consolidation loans, balance transfer cards, and negotiating with creditors should be explored before tapping into retirement funds.

- Using a 401(k) loan avoids early withdrawal penalties and taxes but still results in missed investment growth during the repayment period, impacting long-term savings.

Share this post:

AddTable of Contents