What Is Rental Car Reimbursement Coverage and Is It Worth It?

Last updated 04/08/2024 by

Marcie GeffnerIn a perfect world, no one would ever be involved in a car accident or need car insurance. But in the real world, accidents happen.

If you were in an accident that left your car badly damaged, to the point that you were unable to drive it, how would you get where you needed to go? Maybe you’d carpool or borrow a car from a friend or family member.

Or maybe you’d take public transportation or use a ride-sharing service like Uber or Lyft to get around town. But wouldn’t you rather have your own wheels so you could go wherever you want, whenever you want, without the extra hassle or cost?

If so, rental car reimbursement coverage could be a good option for you. Let’s find out.

Compare Auto Insurance Providers

Compare multiple vetted providers. Discover your best option.

What is rental car reimbursement coverage?

Rental car reimbursement coverage is as simple as the name implies. If your own car isn’t available for your use, your insurance company will reimburse you for the cost of a rental car.

Of course, there’s some fine print.

Rental car reimbursement coverage will pay (for you) to rent a car if yours is no longer drivable after a covered accident.

“Rental car reimbursement coverage will pay (for you) to rent a car if yours is no longer drivable after a covered accident,” says Brad Goldsberry, agency producer for Farmers Insurance at The Nate Bingel Agency in Northglenn, Colo.

The important word is “covered.” If the accident wasn’t covered by your auto insurance policy, your rental car reimbursement coverage won’t kick in.

What does it cover?

“Rental car coverage isn’t for mechanical problems,” Goldsberry explains. “If your car breaks down, you would not be able to use this coverage to get a rental car.”

Likewise, if you don’t have comprehensive or collision coverage, neither an accident nor a rental car would be covered.

Rental car coverage isn’t for mechanical problems. If your car breaks down, you would not be able to use this coverage to get a rental car.”

“If you have liability (coverage) only, there’s nothing to cover (an accident), and therefore, you would not be able to have rental car reimbursement coverage,” Goldsberry says.

Renting a car for a vacation or recreational purposes also isn’t covered. On the upside, you typically can use rental car reimbursement coverage whether you were at fault for the accident or not.

You might also be able to use it if your car was stolen, vandalized, or damaged by severe weather.

Do insurance companies have to pay for a rental car?

Rental car reimbursement coverage isn’t standard with most auto insurance. That means you’ll probably have to pay extra if you want it.

Rental car coverage isn’t for mechanical problems,” Goldsberry explains. “If your car breaks down, you would not be able to use this coverage to get a rental car.”

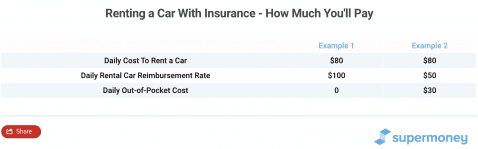

How much you’ll pay depends on your insurer’s rates and the daily reimbursement rate you want if you need to rent a car. You’ll pay more for a reimbursement rate of, say, $100 per day than you will for a lesser amount.

How much you’ll pay depends on your insurer’s rates and the daily reimbursement rate you want if you need to rent a car. You’ll pay more for a reimbursement rate of, say, $100 per day than you will for a lesser amount.

How much does it cost to rent a car with insurance?

How much you’ll pay to rent a car with insurance depends on whether you have rental car reimbursement coverage and, if so, how much your insurance will pay.

Rental car reimbursement coverage may be limited to a set number of days, such as 30. Some policies have a per-accident cap as well as a per-day cap.

If you choose to take public transportation instead of renting a car, your insurer might reimburse your fare instead of your rental car expense. Ask your insurer for details.

Rental car reimbursement coverage typically isn’t subject to a separate deductible.

Insurance is supposed to get you back to normal. If you can’t get to work after you get into an accident, that’s not back to normal.”

How to rent a car with insurance

Suppose you have rental car reimbursement coverage and you can’t drive your car due to a covered claim. Should you rent the car yourself and get reimbursed or ask the insurance company to organize the rental? Here is an in-depth analysis of the pros and cons.

How To Rent a Car With Insurance – Pros and Cons

Should you get rental car reimbursement coverage?

The answer depends on how much you’re willing to pay for additional insurance, how much you rely on your car, and how likely you are to be involved in an accident.

“Insurance is supposed to get you back to normal” Goldsberry says. “If you can’t get to work after you get into an accident, that’s not back to normal.”

Marcie Geffner is an award-winning freelance reporter, editor, writer and book critic. Her work has been featured online and in print by The Washington Post, Los Angeles Times, Chicago Sun-Times, Urban Land, Business Start-Ups and Fox Business Network Online, among many other newspapers, magazines, and websites. With a bachelor’s degree in English from UCLA and MBA from Pepperdine University in Malibu, Geffner has impressive credentials in both story-telling and business management. A second-generation native of Los Angeles, Geffner now lives in Ventura, California, a surf city northwest of her hometown.

Table of Contents