Debt Consolidation: In-Depth Guide to Paying off Debt

AL

Last updated 03/15/2024 by

Andrew LathamFact checked by

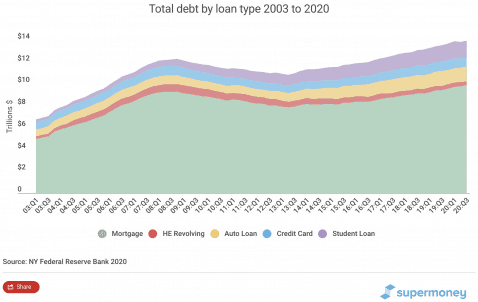

Do you need help getting out of debt? If you do, you’re not alone. The latest report from the New York Federal Reserve tells us that U.S. households hold more than $13.29 trillion in debt. Mortgages aside, consumers owe $4.3 trillion on auto loans, student loans, and credit cards. If you’re among the countless Americans looking to become debt-free, debt consolidation can be a big step in the right direction.

Get Competing Debt Consolidation Loan Offers

Consolidate your debt into one manageable loan with better rates and terms.

It's quick, easy and won’t hurt your credit score.

What is debt consolidation?

Debt consolidation is the process of combining your existing debts into one loan. Instead of making multiple payments each month to various creditors, you make just one payment at a lower overall interest rate, which reduces your monthly payment obligation and simplifies your bill-paying process.

How debt consolidation works

When you consolidate your debt, you are combining all of your existing debt into one single loan. Your old loans are marked as paid off and the balances are combined into the new loan. Having one loan means having only one payment.

Consolidating your debt will give you a lower interest rate, which, in turn, will reduce your monthly payment amount. With a lower amount and only one loan to pay off, it’s easier to make consistent, on-time payments each month.

The goal is to save money and pay off your debt faster by taking advantage of a loan with a lower interest rate.

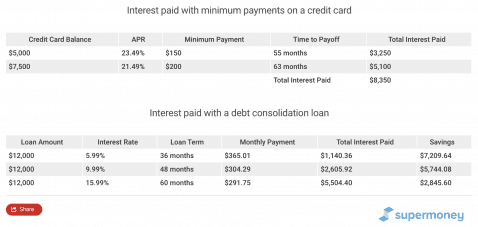

To illustrate, assume you have the following outstanding debts:

- Credit card 1:$5,000 balance, a 23.49% APR, and a $150 minimum payment

- Credit card 2:$7,500 balance, a 21.49% APR, and a $200 minimum payment

The charts below compare the interest payments and time it will take to pay off both cards by only make the minimum payment to using a debt consolidation loan. Notice how much you can save in interest payments if you get a $12,000 fixed-rate loan to consolidate the debt.

Should you consolidate your debt?

It depends on your circumstances and level of self-discipline. “If the root cause of the debtor’s debts arose from a one-time event which is not likely to recur, [it may be worthwhile],” notes consumer rights lawyer Donald E. Petersen.

But it may not be an effective way to deal with overwhelming debt if you’re not disciplined with your spending or continue robbing Peter to pay Paul, Petersen adds.

Calculate your level of debt and determine how long it will take you to pay it off. If you can pay off your debt within three to five years with debt consolidation, it could be a great choice for you.

It can also be a good idea if your unsecured debt is less than half of your gross income.

Your credit score matters

Your credit score also plays a significant role in debt consolidation. The goal of consolidating your debt is to get a lower interest rate and monthly payment– it could save you thousands of dollars.

But you need to have good credit to get an interest rate that will allow you to reap the benefits of debt consolidation.

If you can’t get a lower rate by consolidating your debt, it may not make sense for you to go this route. And the chances of being offered a good interest rate with bad credit aren’t high. But it’s not impossible.

If you can wait to consolidate your debt until you’ve improved your credit score, great. You’ll have more success being offered a loan with a good interest rate.

Five options for debt consolidation

1. Loans from a qualified plan

Do you have a retirement fund or permanent life insurance plan with a cash value component? Either of these might offer you the opportunity to borrow money. Understand the risks, though. Failure to repay some loans can have adverse tax consequences and other financial penalties.

2. Unsecured personal loans

You don’t need stellar credit to qualify for a personal loan, but the most competitive loan offers are reserved for borrowers with excellent credit. Lenders look at your credit score to assess risk and help determine what interest rate to offer.

Different personal loans come with different rates, fees and requirements, so check out what the best personal loans are to ensure that you choose the best option for you.

Understanding personal loan fees

Of course, taking out a personal loan for debt consolidation only makes sense if it saves you money. Some personal loans carry origination fees of anywhere from 1% to 6% that offset savings you might otherwise realize. Several online lenders that don’t charge loan origination fees include SoFi, Discover Personal Loans, and LightStream.

Before applying for a personal loan, be sure to compare rates and terms offered by various lenders.

To get started, use SuperMoney’s loan offer engine to request personalized rates and narrow down your best options. This will not affect your credit score.

3. Credit card balance transfers

If you have credit card debt, reducing or eliminating the interest you are paying on that debt is a good first step towards becoming debt-free. If you are paying high interest rates on your credit card debt, consider transferring that debt to a balance transfer credit card. Some balance transfer cards offer a 0% interest rate for 12-21 months, providing you a window of opportunity to pay down debt interest-free, which can save you hundreds or even thousands of dollars. Balance transfers aren’t free, however. The typical balance transfer card charges a fee that ranges from 3-5% of your balance transfer. And interest rates are typically high after the 12-21 month “introductory period” expires.

Upon approval, you can transfer your outstanding balances to the new card and enjoy a 0% promotional APR, ranging from 12 to 24 months, depending on the card.

4. Home equity loans

Do you own a home with some equity? If so, you can apply for a home equity loan that can provide you with the cash to pay off all or most of your debt. The more equity you have in your home the more likely it is that you will qualify for a reasonable interest rate. The downside of this option is that if you fail to repay the loan, you could face foreclosure on your home.

5. Debt settlement

If consolidating your debts with a loan or credit card balance transfer will still leave you in a tight financial position, you might want to consider debt settlement. A debt settlement company can help negotiate your debt and set up an affordable monthly payment schedule. While there are some benefits to this approach, there are also risks.

Here are a couple of things to consider when looking for a debt settlement company.

How much do you owe?

Most companies require you to have a minimum amount of debt, which is usually around $10,000. Some lenders, such as Freedom Debt Relief, accept lower amounts. Other companies also have a maximum amount of debt you can enroll, such as $100,000. You will need to find a company with requirements that match your needs.

What is their customer service like?

We typically don’t care about the customer service of a company until we run into problems or have questions. It is important to find out ahead of time about the level and quality of support provided by a company. You can do so by researching the support channels they offer (phone, email, live chat, etc.) and by reading reviews from past customers. Look for companies like Debtmerica Relief and Rescue One Financial which are recommended by our community of users. Other debt settlement firms to consider are Pacific Debt and National Debt Relief.

When is debt consolidation a good idea?

If you can realistically pay off your debts with a debt consolidation loan in 3-5 years, this is probably a good choice. However, if you’re not sure about your ability to pay, calculate your level of debt. In cases where unsecured debt is less than half of your gross income, debt consolidation is usually a manageable choice.

When is debt consolidation a bad idea?

Debt consolidation is almost always a good idea if you can both reduce your overall interest rate and make lower payments. However, some types of debt consolidation may be better than others, depending on your situation and spending habits. For example, if you have difficulty controlling your spending, it might not be a good idea to get a new credit card, regardless of your intentions. A debt consolidation loan may be a better option.

Debt consolidation is also not a good choice if your current debt is insurmountable. That is, if your unsecured debt is more than half of your gross income or if it will take more than five years to pay off your debt, consider other options.

How can you improve your chances of approval for a debt consolidation loan?

Before embarking on a debt consolidation project, it is important to know your credit score. A good or excellent credit score will go a long way toward getting you the interest rate you want to see.

You can check your score with one or more of the big three credit bureaus: Experian, Transunion, and Equifax. Check your credit score for free by registering with Credit Sesame with no trial period or other gimmicks. You won’t even have to provide a credit card.

The most well-known credit score is a FICO score. It ranges from 300 to 850, with good credit being anywhere from 650 to 749 and excellent credit being 750 and above. If your FICO score is below 650, your chances of obtaining a debt consolidation loan with a good interest rate are slim.

Here are some ways to improve your credit score and make it more likely that you can get a debt consolidation loan:

1. Pay your bills on time, every time

Your payment history counts as 35% of your credit score. Missing just a few payments can lower your score dramatically. So, even if you can only pay the minimum amount due on your credit cards, be sure that your payment is on time.

2. Increase your income or reduce your debt

While you may have trouble reducing your debt substantially at first, even paying off one credit card bill to a zero balance can help because it will lower your debt to income ratio. Similarly, if you can pick up some extra income, that will also reduce your debt to income ratio, making it more likely that your credit score will improve.

3. Change your due dates

If you are consistently just a few days shy of paying your bills on time, you can ask your creditors to alter the due dates for you. This is especially helpful if you are only paid monthly or bi-weekly.

4. Leave old paid accounts open

While you may think that paying off a credit card account and then closing it is a good idea, it’s not. Closing an account may put a ding in your credit score. By all means, pay off an account if possible, but leave the account open when you do. Your credit score will thank you.

5. Have more than one type of debt

It looks better to lenders when you have a mix of different credit types. A combination of installment debts such as car loans and mortgages, along with revolving debt like credit cards, is a good mix.

Once your credit score is in tip-top shape, getting a debt consolidation loan is much easier.

How does bad credit affect your debt relief options?

You may hear advertisements from lenders offering debt consolidation loans to consumers with bad credit. While it is possible to get a loan with bad credit, the truth is that it may not be your best option.

To make debt consolidation worth your while, it is important that the debt consolidation loan have a better interest rate than the debt you already carry. When your credit is bad, the chances of finding a loan with a good interest rate are very slim. For this reason, those with poor credit may find it advantageous to consider alternative forms of debt relief.

How does debt consolidation affect your credit?

In a perfect scenario, debt consolidation can improve your credit score. Since a debt consolidation loan pays off your unsecured debt like credit cards, your credit card companies will report those accounts as paid in full. This looks good on a credit report. Additionally, if you faithfully pay your debt consolidation loan payments on time, your credit score will improve over time.

However, it is important to note that sometimes a debt consolidation loan can get you into further financial trouble. Because your monthly payment with a debt consolidation loan will be less than the combined payments you are making now, it can seem like you have less debt than you really have. If you are not careful, you can fall back into a pattern of reckless spending and end up in worse financial shape than you are in now. Then, your credit score will plummet.

Using loans vs. credit cards for debt consolidation

Credit card offers with low or 0% interest rates might be tempting, but they’re not always the best choice for those looking to consolidate debt. These rates usually last 12-21 months and then a much higher APR will kick in, leaving you in the same position, or worse than you were before. Also, these cards can be difficult to qualify for, and there is often a balance transfer fee. Unless you plan on paying off your new credit card before the “introductory period” ends, a debt consolidation loan with low interest rates and clear terms may be a better choice.

Debt consolidation options for people with credit scores less than 500

If your FICO score is below 500, your options for a debt consolidation loan are limited. If you own a home, you may wish to consider a home equity line of credit (HELOC). Depending on how current you are with your mortgage payments, you might qualify for one of these loans with a bank or credit union. Another option might be a secured personal loan such as a car title loan, which is backed by the title to your vehicle.

Lenders and loan options for people with credit scores between 500-600

If you have a FICO score between 500-600, you have more options. In addition to the choices listed above, you can either try to borrow from a lender that accepts people with bad credit or find a personal loan lender that allows a cosigner. The benefit of having a cosigner is that you will nearly always receive a more favorable interest rate on your loan.

If you maintain what is considered average to good credit, your choices for a debt consolidation loan improve considerably. These lenders offer loan options for people with credit scores between 600-750+

Alternatives to debt consolidation

There are few alternatives to debt consolidation. If you are unable to pay your debts, you might consider a debt settlement firm or try reaching out to creditors yourself and ask them to lower your payments.

Debt consolidation may not be right for everyone, but it may help you save hundreds, thousands, or even tens of thousands of dollars. If you want to explore your options, let us help you determine whether or not debt consolidation is right for you.Is a credit card a good way to consolidate debt?

Considering that American consumers currently carry $3.8 billion in overall debt, it’s not surprising if you find yourself buried under a mountain of bills. Credit cards and personal loans can quickly add up to a mountain of debt.

To dig out of debt and make your way to financial freedom, you might be considering consolidating all of your outstanding debt with one credit card. Here’s a look at the pros and cons of doing so.

Benefits of consolidating debt with a credit card

Pulling all of your debt under the umbrella of a credit card has various benefits, including the following:

Save on interest

Consolidating debt can give you significant savings on interest. For instance, if you have a personal loan at 8%, a credit card at 20%, and another card at 24%, and you consolidate the balances on a 0% interest rate card for a year, you’ll save a substantial amount in interest. Even if you consolidate all of this debt under a credit card at 7%, you’ll still be ahead.

Simplify matters and pay off debt faster

Managing various types of debt and remembering to pay them all on time can be time-consuming and confusing. When you consolidate, you only have one payment to remember each month. This also enables you to pay off debt faster, especially if you consolidate onto a credit card with a 0% introductory rate.

Potentially elevate your credit score

Having a bunch of credit cards and loans can cause you to have a high credit utilization ratio, which can negatively impact your credit score. By paying off various cards and loans and consolidating under one credit card, you’ll reduce your credit utilization ratio, which should cause your credit score to improve.

Earn added rewards

If you choose a card that offers rewards of some sort, such as cashback or airline credit, and you put a large amount of money on the card in order to consolidate, you’ll open yourself up to increased rewards. You could end up earning yourself an overseas trip or a large cashback credit on your next statement.

Avoid damaging your credit

When you consolidate, you make it more likely that you won’t miss a payment or rack up late charges. Missed or late payments are especially damaging to your credit score, so doing whatever you can to avoid these is important.

Drawbacks of consolidating debt with credit cards

There are some cons to putting all of your debt onto a credit card. Check these drawbacks out before deciding to consolidate debt with a credit card.

More limited options

You’ll need a good to excellent credit score of 700+ to qualify for many of the best credit card offers that feature a 0% introductory rate or low percentage rate. If you’ve paid your current loans and credit cards late or missed payments, your score is probably not going to be high enough to qualify you for credit cards that will enable you to come out ahead.

It’s not a good idea to consolidate your debt under a credit card with interest that is higher than the average of all of your debt. Doing this may give you one monthly payment, but it will put you into deeper debt and is likely to result in it taking even longer to pay off the debt.

The temptation to use paid-off cards

Often, you’ll have credit cards with zero balances after you consolidate. This can present tempting options to use those cards. If you do this, you’ll end up digging yourself into an even deeper debt hole. Keep in mind that it’s best not to take on any more expenses before you pay off your consolidated debt.

It’s wise to have a payoff plan for your consolidated debt and make sure to stick to it. This will allow you to pay off the debt in as speedy a manner as possible so that you can reach your goal of gaining financial freedom.

Pay-off deadline

When you use a 0% introductory rate credit card, you only have between six to 24 months to pay off the card before you’ll have to start paying what is likely to be a high, double-digit interest rate. This means that for the consolidation and debt payoff to work, it’s important to have your debt paid off or at the very least paid down substantially before the introductory rate expires. If you don’t do this, you could end up owing much more than you did before consolidating.

Can ding your credit score

A card that is maxed out because you used it for your consolidated debt can lead to a high utilization ratio, which can result in a dip in your credit score. If you’re paying off other credit cards during the process, which raises your credit score, it could end up a wash.

Extra fees

There are fees associated with transferring debt to a credit card, including balance transfer fees. Check the fine print before consolidating your debt into one credit card.

Credit cards can be an excellent way to consolidate debt if you can qualify for low APRs or, even better, a long 0% APR introductory rate. However, there are drawbacks to consider, such as fees and potential damage to your credit score. Other alternatives to consider are debt consolidation loans and — in extreme cases where you can’t afford the payments — debt settlement programs.

How to approach debt consolidation

You need to look at your debt as a sum total, and not just in terms of monthly payments. If you look at a debt consolidation loan as an “easy way out,” then in all likelihood it will not help you reach your goal. The Consumer Financial Protection Bureau advises:

- Taking on more debt to pay off debt might just be putting off your problems into the future. You can’t pay off debt by taking on more debt.

- The loan you take out to consolidate your debt may end up costing you more in costs, fees and rising interest rates than if you had just continued to pay on your existing debts.

- If your credit score is less than stellar because of your debt load, you probably won’t be able to get the lowest interest rates, so you will want to determine whether consolidation is worth it.

- A nonprofit credit counselor can help you figure out your options.

FAQ on Debt Consolidation

How does debt consolidation work?

When you consolidate your debt, you are combining all of your existing debt into one single loan. Your old loans are marked as paid off and the balances are combined into the new loan. Having one loan means having only one payment. Consolidating your debt will give you a lower interest rate, which, in turn, will reduce your monthly payment amount.

When should you consider debt consolidation?

They’re best when you need $15,000 or less and can pay it off in 21 months or less. If you have more debt, you may need to consider other options, such as a personal loan, for the excess. Based on your credit score, consolidation may not be an option for you.

What to consider before debt consolidation?

Trying to consolidate debt with bad credit is not a great idea. If your credit rating is low, it’s hard to get a low-interest loan to consolidate debts, and while it might feel nice to have only one loan payment, debt consolidation with a high-interest loan can make your financial situation worse instead of better.

Do consolidation loans hurt your credit score?

Debt consolidation can boost the credit scores of consumers struggling to manage several debts such as high-interest credit card debt, medical debt and student loans — if used properly. That said, there are some scenarios in which consolidation could, in fact, cause more harm than good to your credit score.

What credit score do I need for a debt consolidation loan?

Most lenders require a minimum credit score of 630 or 640 to qualify for a debt consolidation loan.

Theory vs. practice

In theory, if you have good enough credit to qualify for a debt consolidation loan that covers all or most of the higher interest debt you carry, you can probably save money in interest and lower the stress on your budget and your life. Just remember that in practice, it takes financial discipline on your part for a debt consolidation loan to have its desired effect and make you debt-free. If and when you are ready, check out SuperMoney’s guide to debt consolidation loans.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: