Should You Refinance From a 30-Year to a 15-Year Mortgage?

Last updated 03/08/2024 by

Marcie Geffner

Refinancing your home mortgage into a shorter term can be a smart move. But you should be prepared for the costs of refinancing and able to handle a much higher monthly payment.

Examples of good reasons to refinance might include:

- Securing a lower rate

- Locking in a fixed rate instead of a variable

- Removing a borrower from your loan

- Getting rid of mortgage insurance, which protects your lender at your expense

Perhaps the best reason to refinance from a 30-year to a 15-year term is to pay off your loan faster with a lower rate, which can save you a lot of money.

How much depends on how high your current 30-year rate is, whether your rate’s fixed or variable, how long you’ve had your loan, and how much lower your new 15-year rate would be.

Compare Mortgage Refinance Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

Cost of refinancing

An important consideration in whether to refinance from a 30-year to a 15-year mortgage is the cost. Typically, you’ll have to pay lender’s fees and third-party charges from other companies in the refinancing process.

Examples of lender’s fees include:

- Loan origination

- Loan commitment

- Doc prep (documentation preparation)

- Processing

- Underwriting

Examples of third-party fees include:

- Appraisal

- Settlement services

- Credit report

- Recording

- Title search and title insurance

These fees can add up to thousands of dollars. How much you’ll pay depends on your loan amount, where you live, and how much your lender charges. A refinance closing costs calculator can give you an estimate of how much it might cost you to refinance.

If you don’t want to pay closing costs out of pocket, shop for a loan with low or no closing fees.

A no-closing costs mortgage isn’t free. The costs will be added to your loan amount, or you’ll pay them over time through a higher rate.

Shopping for a refi mortgage? Check out these lenders: Veterans United Home Loans, AHC Lending, Quicken Loans, loanDepot, USAA and Chase Bank.

Higher monthly payment

If you are thinking about a mortgage refinance, consider your monthly payment.

When you refinance from a 30-year to a 15-year loan, your monthly principal and interest (P&I) payment will be higher due to the shorter payment term.

Usually, your interest savings will more than make up for that higher payment in the long run, says Byron Ellis, a financial planner with United Capital Financial Advisors in The Woodlands, Texas.

If your 30-year loan includes mortgage insurance and you’re able to refinance into a 15-year loan without it, your total payment might be lower.

Another important factor to consider is what you could do with the extra money.

You might want that money to pay off credit card bills, car loans, student debt, or to save for emergencies, retirement, medical expenses, or your kids’ education. Any of those goals might be more important than paying off your mortgage sooner.

If you’re debt-free apart from your mortgage and you’ll all set for savings, you might want to use the money to invest in stocks, bonds, mutual funds, or other assets instead of making a higher mortgage payment. Or you might want to further your education, make a career move, or start your own business.

Extra payments option

Another point to consider is that you don’t have to refinance to a shorter term to pay off your mortgage faster. If you keep your 30-year loan, you won’t get the lower rate of a 15-year term, but you can make additional payments to reduce your balance and get to zero sooner than 30 years.

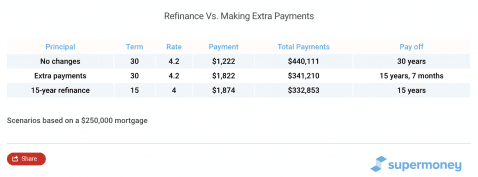

Suppose you have a $250,000 loan with a 30-year term and a fixed rate of 4.2%. Your monthly P&I is $1,222.54. If you make that payment for 30 years, you’ll pay a total of $440,111.

Now suppose you added $600 to your payment every month. That would increase your payment to $1,822.54. If you made that payment every month, your loan would be paid off in 15 years and seven months, and your total payments would be $341,210, a savings of $98,900.

If, instead, you refinanced into a $250,000 loan with a 15-year term and a fixed rate of 4%, your payment would be $1,849.22, and your total payments would be $332,853. You’d save an extra $8,357, but you wouldn’t have the flexibility to skip the higher payment if you needed to and you’d have to pay closing costs.

Get started

It’s smart to shop around and compare loan quotes because the difference between your 30-year and 15-year interest rates is a key factor as seen in the example above.

Marcie Geffner is an award-winning freelance reporter, editor, writer and book critic. Her work has been featured online and in print by The Washington Post, Los Angeles Times, Chicago Sun-Times, Urban Land, Business Start-Ups and Fox Business Network Online, among many other newspapers, magazines, and websites. With a bachelor’s degree in English from UCLA and MBA from Pepperdine University in Malibu, Geffner has impressive credentials in both story-telling and business management. A second-generation native of Los Angeles, Geffner now lives in Ventura, California, a surf city northwest of her hometown.

Share this post:

Table of Contents