Cash-on-Cash Return: What Is It and How Does It Work?

Summary:

Cash-on-cash return, or CoC, is a rate of return metric that calculates the cash income on an investment. Generally, CoC shows up in real estate (particularly commercial real estate), as it helps measure an investor’s annual return on a rental property. While it’s relatively easy to understand and use, it also has a few flaws.

Whether you’re assessing potential investment properties or calculating your profit on existing ones, you’ll want to consider the whole financial picture. Upfront and ongoing operating costs, regular income streams, and the current economy can all impact your financial situation.

To analyze various properties, you may have to sift through a sea of acronyms and metrics like IRR, ROI, and capitalization rate. While the process can be daunting, these metrics allow you to quantify and compare your holdings and potential opportunities quickly.

One of the most important of these is your cash-on-cash return. This formula is easy to calculate and understand and can help you see how much money your rental property could (or should) earn.

So, whether you’re house hacking, house flipping, or looking to finance multiple rental properties, here’s what to know about your cash-on-cash return.

What is a cash-on-cash return?

Cash-on-cash return is a simple financial metric that calculates your pre-tax cash return based on the money invested into a property. Sometimes called the “cash yield,” CoC helps property owners analyze a property’s existing or potential earnings on invested equity.

In other words, your CoC return measures your earnings compared to the cash spent to buy, repair, and improve a property.

Cash-on-cash return is significant in commercial real estate, as large property investments often involve a lot of debt. When investors use debt to buy real estate, other profitability metrics — like ROI — become much less reliable.

But CoC excludes debt and evaluates only the actual cash amount invested. This allows investors to obtain a more precise measure of their investment’s performance.

What a cash-on-cash return tells you

Real estate investors use cash-on-cash returns for several reasons, including:

- Picturing annual cash flow. CoC metrics make it easy to compare the money flowing in and out of a property. Expressed as a percentage, it points to a property’s profitability based on your cash investment.

- Property comparisons. Cash-on-cash returns help investors analyze the profitability of multiple real estate deals side-by-side based on rent, expenses from operations, and down payment size. You can use this information to determine how a property has or will perform before you invest.

- Analyzing expense profiles. Properties with higher expenses or more renovations required usually result in a lower cash-on-cash return. Prospective buyers may use this information to determine if a property’s CoC is too low for their portfolio.

- Looking at financing. Cash-on-cash return is a particularly important metric if you’re purchasing properties with financing. A property’s CoC return can help you determine how large of a down payment (and loan) you should consider. Additionally, it may help you decide if a traditional or private lender can better maximize your annual returns.

One important note is that CoC doesn’t include property-related debts like a mortgage or home equity loan. Only your down payment, closing costs, and the price of renovations, upgrades, or maintenance count toward your cash investment.

To compensate, some investors calculate CoC annually by adding the paid-off portion of their mortgage to their initial cash investment. If you’re looking to invest in a property but haven’t found the right mortgage lender yet, take a look at some of the lenders below.

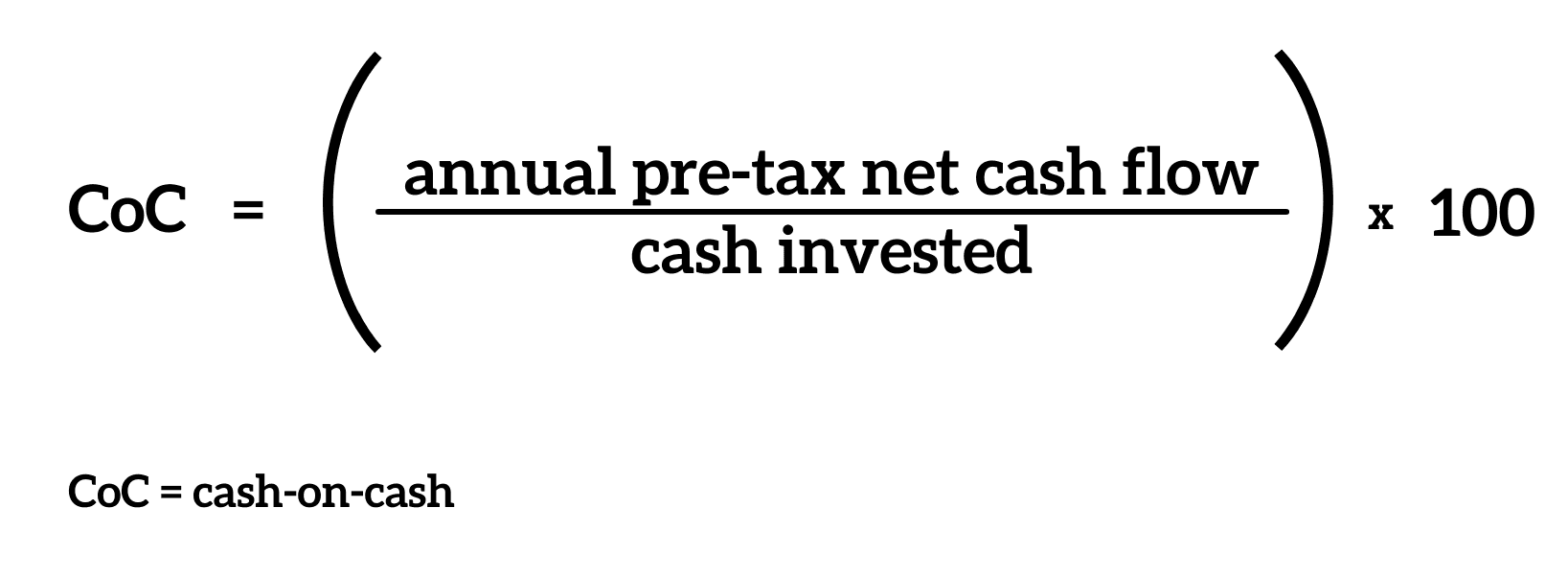

Calculating cash-on-cash return

You can calculate CoC returns using an investment property’s pre-tax cash flow alongside your initial or total cash investment.

The basic cash-on-cash formula looks like this:

While this equation is fairly simple, it does require you to correctly track your property’s total annual cash flow.

To start, you need to calculate your annual pre-tax cash flow. That includes income like rent, parking fees, and storage unit fees. Then, you have to subtract costs like vacancies, maintenance and repairs, and your annual mortgage payments.

Once you’ve calculated your net pre-tax cash flow, you can divide that number by the cash you’ve invested in your property. This value may include your down payment, closing costs, and renovations or repairs you paid for in cash. If you’re calculating an updated CoC, you’ll also want to consider any mortgage payments you’ve made.

Pro Tip

The original cash-on-cash return only uses your initial cash invested, such as down payments and renovations. But you can calculate an updated CoC using your total cash invested by adding in annual mortgage payments, additional upgrades, etc.

Cash-on-cash return example

You can calculate CoC differently based on your situation. Let’s look a simple examples:

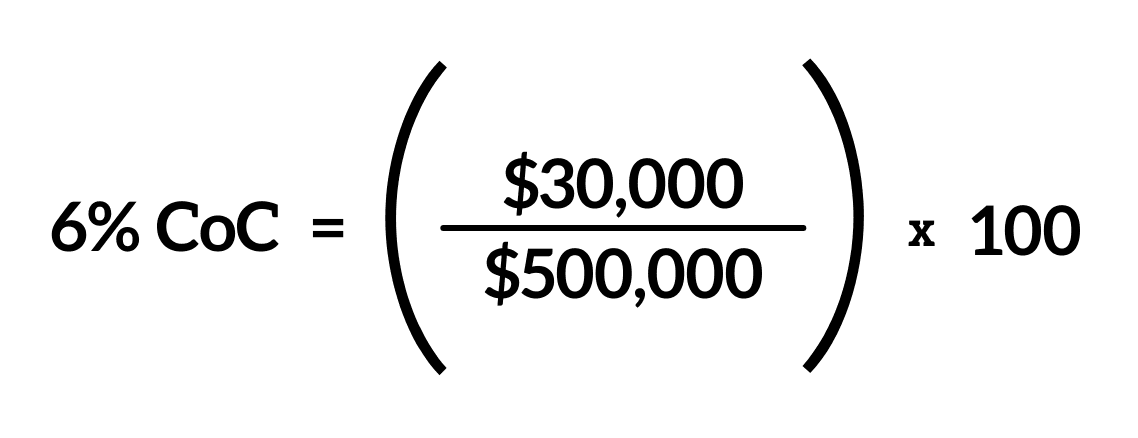

Say that you buy a rental property for $500,000 in an all-cash deal. You charge tenants $2,500 per month in rent or $30,000 per year.

This equation gets a little more complicated when you try to calculate the CoC of a flipped property.

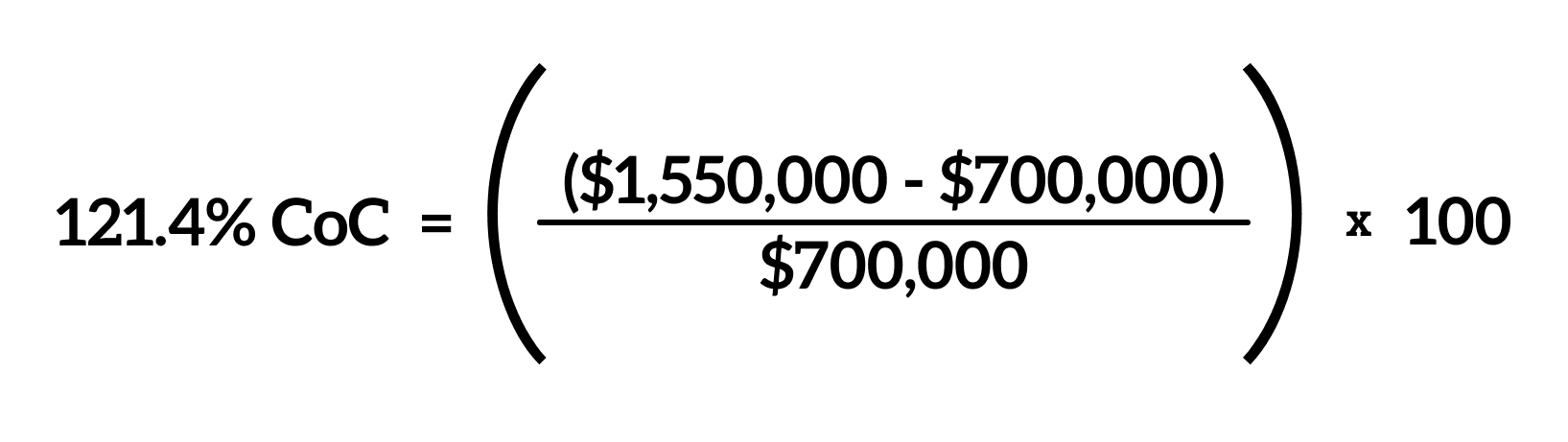

House flipping CoC

Now, say that you buy a property for $1 million with $500,000 cash down. All told, your mortgage is $500,000. You also pay an additional $100,000 out of pocket for closing costs, hardscaping, and other renovations.

A year later, you sell the property for $2 million. At that point, you’ve paid $100,000 in loan payments, including a principal repayment of $50,000.

In this example:

- Your total cash outflow is ($500,000 + $100,000 + $100,000) = $700,000

- Your total cash inflow is ($2,000,000 – $450,000) = $1,550,000

So, your total CoC is:

Pro Tip

You can also use CoC calculations to forecast your expected future returns. That said, because you can’t predict future cash flow, it’s not a promised return.

Factors that affect cash-on-cash return

On paper, your cash yield should stay constant, assuming that your incoming and outgoing cash flow remains unchanged. But in the real world, rental income and operating expenses often fluctuate.

Some of the factors you can expect to impact your cash-on-cash return include:

- Your down payment amount

- Monthly rent prices

- How long and often the property sits vacant

- Property taxes

- Homeowner’s insurance

- Maintenance fees

- Upgrades and renovations

Pro Tip

If you buy property in cash up front, your CoC will drop, but you won’t have a mortgage. By contrast, financing your purchase increases your CoC, but more of your profits will go to your lender.

CoC vs. …

Your cash-on-cash return is just one of several metrics you should watch in your real estate investment portfolio. Here are a few others to consider.

Cash-on-cash vs. return on investment (ROI)

Return on investment (ROI), is a cumulative metric that calculates your total return on an investment, including any debts. Because this metric measures profitability over an investment’s lifetime, you only know a property’s true ROI once it sells.

By contrast, CoC only measures returns on the actual cash invested, providing a more accurate analysis of an investment’s performance.

Cash-on-cash vs. IRR

IRR, or internal rate of return, measures the total interest earned on invested funds. You can use IRR to determine an investment’s potential profitability throughout its entire holding period based on total pre-tax cash flow, initial costs, and time invested. IRR calculations are more complicated and stretch over a longer time horizon.

Cash-on-cash vs. cap rate

The capitalization rate (cap rate) formula measures an investment’s potential profitability by dividing net operating income by the property’s market value. Then, you turn the number into a percentage. Generally, cap rates help compare potential investment properties in a similar area.

By contrast, CoC returns consider total cash invested rather than a property’s market value. While cap rates can help investors choose between potential deals, CoC returns provide a closer look at profitability.

Cash-on-cash vs. NOI

You can calculate NOI, or net operating income, by subtracting a property’s operating expenses from its total monthly rental income. These expenses include costs like maintenance, landscaping, and utilities. Unlike CoC, NOI does not consider debt services.

What is a good cash-on-cash return?

There’s no simple way to determine a “good” cash-on-cash return, as that answer depends on factors like:

- Your risk tolerance

- The property’s location and type

- Any upfront or ongoing maintenance or renovation costs

- Local housing market conditions

- How much cash to invest upfront

Many investors consider 8% to 12% to be a good CoC return. For beginning investors, particularly risk-averse individuals, or those in difficult markets, 5% to 7% may be acceptable. But for other investors, anything less than a 20% to 30% return may be unacceptable.

What is the 2% rule?

The 2% rule is a guideline for real estate investors to follow in order to make sure they are cash flow positive. The rule states that the monthly rent should be at least 2% of the purchase price of the property.

Key Takeaways

- Cash-on-cash return measures the profit from an investment compared to the cash initially invested on a pre-tax basis.

- Unlike some other financial metrics, CoC measures returns only for the current period (usually a year).

- CoC often fluctuates between periods due to annual cash flow changes in rent, expenses, and interest rates.

- Still, you can use cash-on-cash return calculations to forecast projected profitability before receiving cash on delivery.

- Unfortunately, cash-on-cash carries a few important limitations, like:

- Ignoring specific tax situations

- Failing to consider appreciation or depreciation

- Not considering emergency and long-term costs

- It’s wise to check your cash-on-cash return every 6 to 12 months to ensure you’re on track financially.

- You may want to have some petty cash set aside to tide you over in rough markets.

Table of Contents