FHA Loan vs. Conventional Mortgage: Which Is Right for You?

JW

Last updated 03/15/2024 by

Jessica WalrackThinking of buying a house or refinancing, and not sure whether to go with an FHA or conventional loan? The fact that you are wondering is a good thing.

That means you are concerned with getting the best deal.

This article will break down the key factors of both options.

We will look at:

- Property types allowed

- Down payment requirements

- Mortgage insurance

- Interest rates

- Debt-to-income ratios

- Credit score requirements

- Loan limits

- Refinancing options

- Recommendations

- Where you can get a range of conventional and FHA lenders

Let’s get started!

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

FHA loans overview

FHA loans are mortgage loans backed by the U.S. Department of Housing and Urban Development’s Federal Housing Administration (FHA). Select third-party lenders provide these loans to borrowers and, if a borrower defaults, the government ensures the lender is repaid.

Eligible property types

FHA loans will finance single-family properties that consist of one to four units. At least one borrower is required to live in the property as their primary residence within 60 days of signing and must remain there for one year.

Using FHA to obtain investment properties is not allowed.

Second homes are allowed under very specific circumstances, such as if you need to move for employment purposes and can prove rent prices are abnormally high. However, FHA is designed to be used primarily for a borrower’s primary residence.

All properties must pass an inspection from a FHA-appraiser. The inspection includes a long list of requirements to ensure the home is safe, sound, and secure.

(Note: The FHA 203(k) is another option if you want to buy a house that needs rehabilitation. It is a FHA-insured loan that combines the cost of home and the rehab into one loan.)

Down payment requirements

The down payment on an FHA loan can be as low as 3.5% of the loan amount. A 580 credit score is required for this down payment amount. Otherwise, you will be required to put down 10%.

According to the Origination Insights Report from Ellie Mae, the average loan-to-value percentage (LTV) of borrowers who purchased homes with an FHA loan from January to July of 2017 was 96%, meaning the majority of them are putting 3.5% down.

Mortgage insurance

Mortgage insurance (MIP) is required on all FHA loans. Borrowers must pay an upfront mortgage insurance payment AND an annual premium that is typically broken up into monthly payments.

The upfront payment can be financed along with the mortgage. The amount of the upfront MIP is 1.75% of the base loan amount.

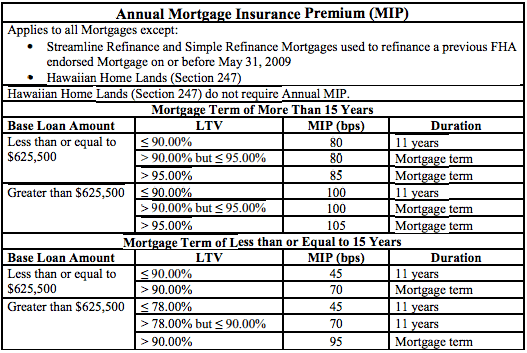

The annual MIP will depend on the length of the loan term, the loan amount, and the loan-to-value ratio. It ranges from .8% to 1% of the base loan amount per year for 30-year mortgages, and .45% to .95% of the base loan amount per year for 15-year mortgages.

Borrowers are required to pay the annual MIP for the entire loan term if the loan-to-value ratio is greater than 90%. That means if you get the 3.5% down payment, you will pay MIP the entire duration of the loan. If your loan-to-value ratio is less than or equal to 90%, you will pay MIP for 11 years.

Here is HUD’s current MIP chart as a reference:

Interest rates

According to the Ellie Mae report, a 30-year fixed-rate FHA loan has a 4.28% average YTD interest rate in 2017.

Debt-to-income ratio

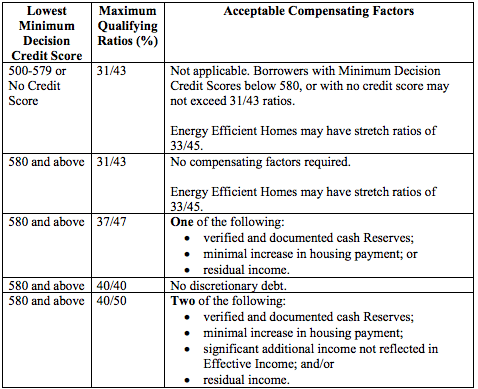

The debt-to-income (DTI) ratio requirements depend on an applicant’s credit score, compensating factors, and if the home is energy efficient. (Note: Compensating factors include residual income, cash reserves, additional income, and an increase in housing payments.)

There are two debt-to-income ratios that are taken into consideration:

- Total Mortgage Payment to Effective Income Ratio (PTI): The maximum percentage of a person’s effective income that a mortgage payment can consume.

- Total Fixed Payments to Effective Income Ratio (DTI): The maximum amount of all debt (including the mortgage payment) a person can have in relation to their effective income.

Here is the chart provided by HUD detailing the DTI limits. The first number in the Maximum Qualifying Ratios column is the PTI and the second is the DTI:

According to the Ellie Mae report cited above, 28/43 is the average DTI of borrowers who purchased homes with an FHA loan from January to July of 2017.

For example, if these buyers bring in $4,000 per month of income, they are paying $1,120 per month to their mortgage (28%) and $1,720 per month total to all of their debts and liabilities (43%).

Credit score

The minimum credit score allowed is 500. However, to qualify for the lowest down payment, better interest rates, and higher debt-to-income limits, you’ll need a score over 580.

According to the Ellie Mae report, 684 is the average FICO score of borrowers who purchased homes with an FHA loan from January to July of 2017.

Loan limits

FHA’s loan amounts are set based on the Metropolitan Statistical Area and County limits. You can look up the prices in your area here.

The FHA national low-cost area mortgage limit for a one-unit property is $275,665. The high-cost area mortgage limit for a one-unit property is $636,150. The average of the two is $455,907.

The only exceptions are for Hawaii, Alaska, Guam, and the Virgin Islands, which face higher building costs so have an upper limit of $954,225.

Refinancing

FHA will insure several types of refinancing such as cash-out refinancing, non-cash-out refinancing, and refinancing of FHA and non-FHA mortgages.

However, if you are refinancing an existing FHA mortgage, you may qualify for the streamline refinance program. The program has two options:

- The first is “credit qualifying,” where the mortgagee will perform a credit and capacity analysis on you but no appraisal of the home is needed.

- The second option is non-credit qualifying, which doesn’t require the credit and capacity analysis or the home appraisal.

Conventional mortgage overview

Now, for a look at conventional mortgages. These are home loans that do not have any guarantees. The most common conventional loans are conforming loans, which adhere to the guidelines established by Fannie Mae and Freddie Mac.

Loans that exceed the conforming loan limits are commonly known as “jumbo loans” and are categorized as non-conforming. Mortgage lenders may also offer non-conforming loans on their own books, which have unique qualification standards.

Eligible property types

Conventional mortgages can be used on a borrower’s principal residence, second home, or an investment property. However, certain conventional loan programs may have restrictions on the type of property you can buy to get the deal.

Down payment requirements

The down payment required can vary.

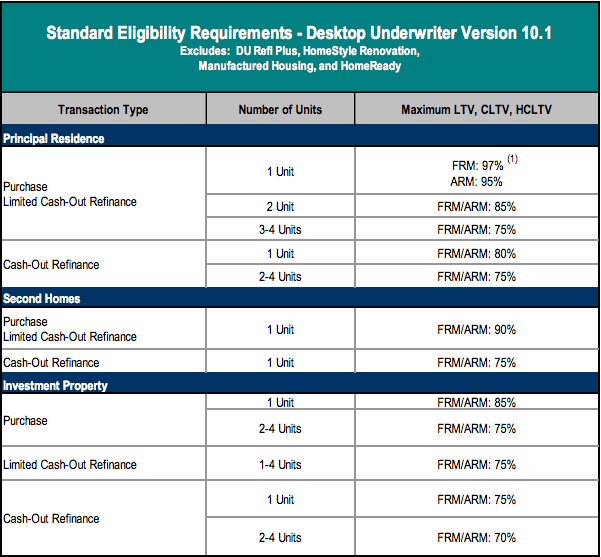

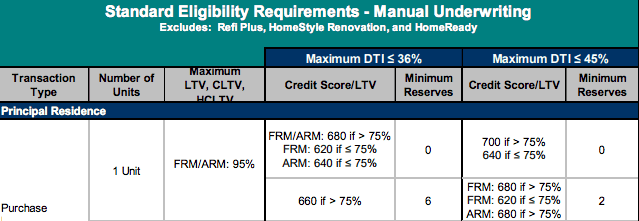

For example, according to Fannie Mae’s guidelines, the amount required changes from 3% to 25% due to a borrower’s credit score, the type of property they want to buy, their debt-to-income ratio, and their minimum reserves.

Here is Fannie Mae’s manual underwriting chart from their 2017 Eligibility Matrix. The down payment is the difference between 100% and the LTV percentage.

Fannie Mae offers a 97% loan-to-value (LTV) option, which contends with the FHA’s 3.5% down payment. Quicken Loans has gone a step further and offered a 1% down payment.

However, both of these programs have restrictions, such as only allowing single-unit primary residences to be eligible. Other private lenders may allow for low down payments based on their own underwriting guidelines.

According to the Origination Insights Report from Ellie Mae, the average LTV of borrowers who purchased homes with a conventional loan from January to July of 2017 was 80%. That means most made a down payment of 20%.

Mortgage insurance

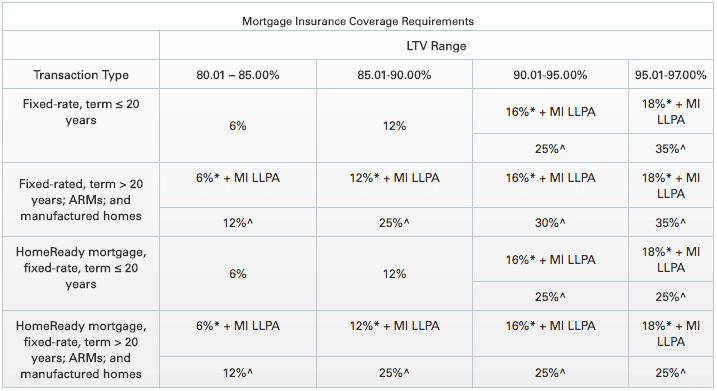

If you get a conventional loan and put down less than 20%, you will have to get annual private mortgage insurance (PMI). Below are Fannie Mae’s requirements.

You’ll see that the lower the loan-to-value ratio, the lower the cost of the mortgage insurance. The good news is that you can drop the insurance when your LTV is equal to or less than 80%. It is automatically canceled when your LTV reaches 78%.

Source: Fannie Mae

Interest rates

According to Freddie Mac, the average YTD interest rates for 2017 are as follows:

- 30-year fixed rate mortgage: 4.04%

- 15-year fixed rate mortgage: 3.28%

- 5/1 adjustable rate mortgage: 3.18%

Debt-to-income ratio

According to Fannie Mae’s eligibility matrix, the debt-to-income (DTI) ratio requirement is affected by other factors, including a borrower’s credit score and loan to value ratio.

For example, a DTI less than or equal to 36% allows for acceptance of a 680 credit score if the down payment is less than 25%. If the down payment is equal to or greater than 25%, then a 620 credit score is required for a fixed-rate mortgage and a 640 credit score is required for an adjustable-rate mortgage.

The higher down payment allows those with lower credit scores to get approved.

A DTI of up to 45% is allowed if a borrower’s credit score is 700 and their down payment is less than 25%. It is also allowed if the borrower has a credit score of 640 and their down payment is 25% or more.

Source: Fannie Mae

According to the Ellie Mae report cited above, the average DTI of borrowers who purchased homes with a conventional loan from January to July of 2017 was 23/35.

Credit score

Generally, conventional loans will require a minimum of a 620 credit score. However, some lenders will have more strict or lenient requirements.

For example, the Quicken 1% loan requires a credit score of 680. The required credit score will also often depend on other factors, such as the down payment amount and DTI.

According to the report from Ellie Mae, the average FICO score of borrowers who purchased homes with a conventional loan from January to July of 2017 was 752.

Loan limits

As of 2017, the maximum conforming loan amount on Fannie Mae and Freddie Mac loans for one-unit properties is $424,100. This is in effect for most areas in the country. However, higher-cost areas will have higher loan limits.

For higher loan amounts, borrowers can look into jumbo loans.

Refinancing

Conventional refinancing is available with or without cash out from various lenders. It requires applying with a lender and going through the normal approval process (credit and income analysis/ appraisal).

FHA or conventional loan, which is better?

“Determining whether FHA or conventional financing is best for a borrower can be a really easy or difficult thing,” says Milauskas.

If you are looking for a second home or investment property, conventional is the way to go. However, when looking for a primary home, you’ll have to compare apples to apples.

“Conventional financing places a lot of emphasis on down payment and credit score in determining the interest rate for buyers, whereas FHA does not. Generally, borrowers with lower credit scores will benefit from FHA financing, and borrowers with good credit will benefit from going conventional. This is not a steadfast rule, just a generality,” says Tim Milauskas, Loan Originator at

First Home Mortgage Corp.

First Home Mortgage Corp.

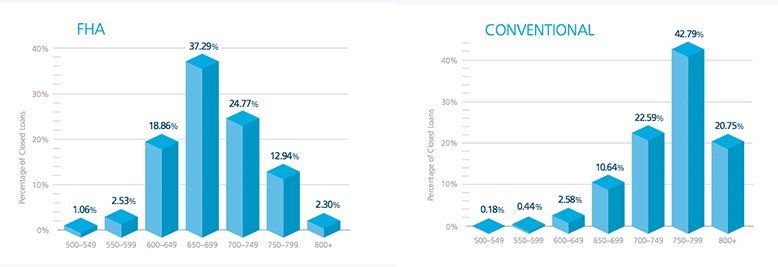

As you can see in the graph below, the credit score spread for conventional loans was significantly higher than for FHA loans.

The majority of conventional borrowers have a score from 650 to 800+, whereas the majority of FHA borrowers have scores between 550 and 799.

Another main differentiating factor is the mortgage insurance. On an FHA loan, two types are required: upfront and annual. Conventional loans typically only require annual, which saves buyers the 1.75% of the base loan amount cost at the outset of the loan.

Furthermore, FHA requires you to keep the insurance longer than conventional loans. If you put down less than 10% on an FHA loan, you have to keep the insurance for the duration of the loan.

If you put down 10% or more, you still have to keep it for 11 years. With a conventional loan, you can drop the insurance as soon as your LTV reaches 80%.

Other factors to consider include:

- Down payments: Both loan types can provide buyers with a low down payment. However, conventional borrowers typically put more down.

- Loan limits: The loan limits aren’t much different for single-unit residences. However, they will vary based on where you live, so you should check what limits are offered by each in your area. Furthermore, some mortgage lenders will extend non-conforming loans for higher amounts.

- Interest rates: When looking at FHA vs. conventional loan rates, interest rates are typically lower on conventional loans. The catch is, you have to have good credit to get the lowest rates. If your credit isn’t so good, FHA may provide the better deal.

- Debt-to-income ratios: FHA allows for a slightly higher debt-to-income ratio, allowing borrowers with more debt to afford a higher monthly mortgage payment.

- Refinancing: Refinancing can be done through both routes. However, if you are refinancing an FHA loan, the FHA streamline refinance program is highly convenient. If not, shop around and compare rates and terms. d your plans for the future.

For those with low or no credit and a modest income, FHA is often the way to go. For those with more established credit and higher income, a conventional loan may offer a better deal.

However, there are exceptions, so it’s wise to do your due diligence. This is a decision that will heavily impact your finances for up to three decades.

If you are still a bit unclear, Milauskas advises, “Working with a knowledgeable and experienced loan officer helps.”

Here is an overview of the factors we have discussed so far:

FAQ on FHA loan

What is an FHA loan and how does it work?

An FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA). They are popular especially among first time home buyers because they allow down payments of 3.5% for credit scores of 580+. However, borrowers must pay mortgage insurance premiums, which protects the lender if a borrower defaults.

What qualifies someone for an FHA loan?

For one, FHA requires a low-down payment of just 3.5% with a 580 credit score. You can get approved for an FHA mortgage loan with a 500-579 credit score with 10% down. If you have at least a 580 credit score, it is easier to qualify for an FHA mortgage.

What is considered a conventional mortgage?

A conventional mortgage is a home loan that isn’t guaranteed or insured by the federal government. Conventional mortgages that conform to the requirements set forth by Fannie Mae and Freddie Mac typically require down payments of at least 3%.

What is the minimum down payment required for a conventional mortgage?

Though some conventional mortgages have a down payment requirement as low as 3 percent, most typically require a down payment of 5 to 20 percent, according to the Consumer Financial Protection Bureau. No mortgage insurance is required on a conventional loan with a down payment of at least 20 percent.

Do I qualify for a conventional mortgage?

Conventional loans are best suited for borrowers with good credit. Most conventional mortgages will require a minimum credit score of 620-640. Having a higher credit score is even better. If you’re score is on the lower end, or below the minimum score required than an FHA loan may be a better option for you.

Ready to shop around for a lender? Head to our Mortgage Purchase Review Page. You will find a range of conventional and FHA lenders, reviews of their services, and ratings from real users.

Still have more questions about FHA loans? Check out our comprehensive FHA FAQ.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: