How To Get Out of Debt: Ultimate Guide to Being Debt Free

AL

Last updated 03/15/2024 by

Andrew LathamFact checked by

Summary:

Are you struggling with debt? This two-stage guide will help you determine which debt-busting strategies are most likely to work for you and how to implement them in a personalized get-out-of-debt plan. You will also learn how to work out if a debt consolidation loan makes sense and when more extreme debt-busting methods may be required.

Falling into a cycle of debt is easy. Getting out of debt is another matter altogether. If you’re overwhelmed with debt, you are not alone. The latest data by the Federal Reserve shows the steepest increase in household debt since the Great Recession. Overall household debt hit $14.3 trillion. That is $1.6 trillion more than the previous peak in 2008 and 28% more than our last “debt trough” in 2013. It’s no wonder getting out of debt was the number one new year resolution in 2021.

The good news is you already have everything you need to build a debt-free life. This step-by-step guide provides a simple yet effective way to pay off your debt. It’s not easy, but you can do it!

Six steps to freedom from debt

- Build a modest emergency fund. Even just $500, $1,000, or one month of living expenses is a good start.

- Pay off all your debts using the blizzard method. Don’t include your mortgage and other loans with low interest rates at this stage.

- Pay off your smallest loan first and give yourself a quick win.

- Rank your debts by interest rate (larger to smaller) and pay them in that order.

- Consolidate your debt if you qualify for a low interest rate.

- Increase your savings and build a more substantial emergency fund. Aim for three to six months of living expenses.

- Start investing. Aim to save 15% to 20% of your income and invest it in your retirement accounts.

- Pay off all your debts. Now it’s time to tackle your mortgage.

- Create wealth and be generous. Enjoy your hard-earned financial independence and share the wealth.

Get Competing Debt Consolidation Loan Offers

Consolidate your debt into one manageable loan with better rates and terms.

It's quick, easy and won’t hurt your credit score.

Stage 1 — Determine what strategies will work for you

The first stage is designed to help you take stock of your financial situation to determine which debt-payment strategies are the best fit for you. It is an interactive guide, so you will need to put in some work to get anything out of it. In the second stage, we discuss in more detail how these strategies work and how you could combine them in your own get-out-of-debt plan.

Getting out of debt is not rocket science. You just need to understand the pros and cons of each strategy, consider some basic guidelines, and apply them to your specific financial circumstances.

What debt repayment strategies are there?

Here are the seven debt-busting strategies to consider.

- Avalanche method. Pay the minimum on all your accounts and as much as you can on the account with the highest interest rate. Continue until all the accounts are repaid. This is the best method to minimize interest payments.

- Snowball method. Pay the minimum on all your accounts and as much as you can on your smallest account. Rinse and repeat until all debts are paid. Some people find it easier to stick to this method because it provides more frequent small wins that act as psychological boosts every time you pay off an account.

- 0% APR balance transfer credit card. These cards offer a 0% APR during an introductory period that typically ranges from 9 to 18 months. After that, interest rates will usually rise to 20% or higher. If you can repay it within the introductory period, this is probably the cheapest way to get out of debt.

- Debt management program. These are repayment plans set up and managed by a credit counseling agency. There are fees to pay, but it can be a good option for people who are not great at budgeting or managing payments.

- Debt consolidation. A loan or line of credit that allows you to combine high-interest debts into one low-interest payment. It can save you money in interest payments, but it may promote overspending if you’re not good at managing credit. There are unsecured debt consolidation loans, such as personal loans, and secured ones, such as home equity lines of credit and home equity loans.

- Home equity investments. Also known as shared equity agreements, home equity investments allow you to tap into your home’s equity to pay off debt without taking on more debt. There are no monthly payments and no interest rates. Instead, you agree to give investors a share in the equity of your home when you sell it or when the contract ends.

- Debt settlement. A negotiated agreement in which a lender accepts less than the full amount owed in exchange for a lump-sum payment. It can cut your debt in half, but it will nuke your credit.

You have probably heard about all of these strategies before. But which should you use? There isn’t a one-size-fits-all answer to that question.

You are the expert on your finances

Ignore “experts” who tell you which method is the best without knowing anything about you. The best strategy depends on your circumstances and your priorities.

Answer the following questions to reveal which combination of debt relief strategies is best for you. I recommend you create a basic spreadsheet to record your answers and build your budget. This is a basic spreadsheet you are welcome to copy and modify.

7 Questions to determine the best debt-busting strategy

- How much do you owe?

- What is your income?

- What is your debt-to-income ratio?

- What is your credit score?

- What is your discretionary income?

- How long will it take to repay your debts?

- Can you (realistically) follow a debt repayment plan?

1. How much do you owe?

This question is as basic as they come, but it’s often the hardest to answer. It takes courage to sit down and work out exactly how much you owe. Create a spreadsheet and list all your debts. If you can’t remember all your lines of credit, check your credit report using one of the credit monitoring services below.

Once you have all your credit accounts listed, separate them into secured and unsecured debts.

In this guide, we will focus on consumer debt. Consumer debt includes any type of unsecured debt that is not backed by an asset or security, such as credit card debt, personal loans, medical bills, and payday loans.

Similar principles will apply to other types of debt, such as mortgages, auto loans, and student loans, but they should be tackled a little differently because there are additional options available.

Why is this important? If you owe less than $15,000 and you have excellent credit, you may be able to consolidate your debt with a 0% APR balance transfer credit card. This can be the best way to get out of debt if you can repay it within 12 to 18 months. A debt consolidation loan is an option for larger amounts and for when a balance transfer card is not available.

2. What is your income?

Your income is your most powerful debt-busting tool. You need to know if it’s up to the task. If your income varies significantly from month to month, estimate it based on your average income for the last two years.

Why is this important? If you have a low income and no way to increase it, repaying a substantial debt may not be realistic. Getting a second job or an extra shift on your current job is probably the single best thing you can do to get out o debt. If that isn’t possible, or if it doesn’t make much of a dent in your debt-to-income ratio, a debt settlement or even filing for bankruptcy may be your best alternatives. Your income will also determine if you qualify for balance transfer cards or a consolidation loan.

3. What is your debt-to-income ratio?

Divide your total consumer debt by your annual income. For example, let’s say you have $30,000 in unsecured debt and a yearly salary of $50,000; the result would be 0.6.

Why is this important? If your total unsecured debt is more than half your annual income, repaying your debt in a reasonable amount of time may not be feasible. Also, creditors often use a debt-to-income ratio of at least 0.5 as a threshold before they consider negotiating a debt settlement.

4. What is your credit score?

Your credit score is a number that represents the risk a lender takes when you borrow money. Higher scores mean you have demonstrated responsible credit behavior in the past, which may make potential lenders and creditors more confident when you apply for a loan.

Why is this important? If you have good credit (above 670), you may qualify for a debt consolidation loan with competitive rates or a 0% APR balance transfer card. On the other hand, if you have bad credit, aggressive debt relief methods become more attractive.

5. What is your discretionary income?

To answer this question, you will need to create a simple budget that lists all your essential expenses. This spreadsheet has a list of basic expenses with their average cost based on the latest survey by the Bureau of Labor Statistics. Enter your living expenses. Once you finish, deduct your total monthly living expenses (don’t include your unsecured debt payments) from your monthly income. This is your discretionary income.

Why is this important? Your discretionary income is the maximum amount of money you could put toward repaying your debts on your current income. If your discretionary income is low, say $500 or less, but your debt-to-income ratio is also low, you probably need to take a hard look at your budget. The odds are you have plenty of fat to trim from your “basic living expenses.” Once you know your discretionary income, you can answer another important question when choosing the best debt repayment method.

6. How long will it (realistically) take you to repay your consumer debt?

A shorthand way to do this is to divide your debt balance by your monthly discretionary income. The result is an extremely optimistic estimate of the time it will take to get out of debt. Of course, few people have the discipline to put all their discretionary income toward debt for any significant amount of time. And this estimate doesn’t include interest payments. However, it gives you a rough estimate. So let’s say you owe $30,000, and your discretionary income is $500 a month. That means it would take a minimum of 60 months to pay off your debt.

How does this help? If you can repay your debt in less than five years, consider using the snowball or avalanche method. Borrowers with good credit who can qualify may also want to consider getting a 0% APR balance transfer card if they can repay it within 12 to 18 months. If that isn’t realistic, a debt consolidation loan can also save money in interest payments.

However, if it’ll take 5 years or more to repay, you will probably struggle to find a debt consolidation loan. Try to increase your income. In cases where that is not an option, it may be time to look at more aggressive debt-relief options, such as filing for bankruptcy.

7. Are you confident you can follow a debt repayment plan by yourself?

Because we are not robots, we don’t always do what we know we should. The math of getting out of debt is simple, but the behavioral side is anything but. Some people enjoy geeking out on their budget and maximizing every dollar they make. If that describes you, you can do this by yourself. Others — which include successful individuals in their fields of interest — struggle with managing money and making payments on time.

If you would benefit from some help or thrive when you are held accountable to someone providing you regular feedback, consider hiring a credit counseling agency. They can help you prepare a personalized debt management plan, negotiate lower monthly payments, and create a realistic budget. If you choose a debt management program with lower monthly payments, it will increase the interest you pay and the time it takes to get out of debt.

Another option is to hire a debt settlement company to negotiate a lower debt balance with your creditors. It could reduce your debt and help you get out of debt faster. But it will destroy your credit.

Which debt repayment method is best for you?

Every single one of the strategies we listed above (i.e., avalanche, snowball, debt consolidation, and debt management program) could be the best option for you. It all depends on how you answered the questions above.

Here’s a quick summary of some of the guidelines you may want to consider when choosing.

- Debt levels. If you owe more than $15,000, a balance transfer credit card is not an option. But a debt consolidation loan may help. Borrowers who owe less than $15,000 and have excellent credit should consider a 0% APR balance transfer credit card. But only if they can repay the entire balance within 12 to 18 months. A debt consolidation loan is a good alternative if it will take longer to repay. Either way, the snowball or avalanche methods are great repayment options to use with all your debts (secured and unsecured).

- Debt-to-income ratio A ratio that is higher than 0.5 may indicate that you are financially overextended. Creditors use this as a threshold to negotiate a debt settlement. Consider increasing your income. If that is not an option and it will take more than 5 years to pay, you may want to consider negotiating with your creditors.

- Time to get out of debt Will it take more than 5 years to get out of debt with your current discretionary income? You may need to consider a more aggressive debt relief strategy if you can’t increase your income or have poor credit. But if your debt-to-income ratio is low, you can probably tighten your budget and pay it off sooner. However, if you can pay it off in less than 60 months, use the snowball or avalanche methods. You can save money and get out of debt faster if you get a 0% APR balance transfer or a debt consolidation loan. A credit counseling agency can also help if you need help managing your payments and budget.

- Credit score. If you have great credit, a 0% APR balance transfer or a debt consolidation loan can help you save money and get out of debt faster. If your credit score is poor and you are struggling to make payments, you will need to consider other options.

Stage 2 — How to get out of debt

You now have a good idea of which strategies would work best for you. Now it’s time to combine them into a cohesive plan.

A step-by-step guide to paying off debt

- Take stock of your debts and create a budget.

- Consolidate your debt and reduce interest payments.

- Choose the best payment method for you (snowball, avalanche, blizzard).

- Make more money.

- Determine whether extreme measures are necessary.

Step 1: Take time to get a handle on your financial situation

For many, this is the hardest step in our guide. After all, who has time to sit down and create a budget. Unfortunately, there is no way around it. If you worked through stage 1 of this guide, you already have a good start.

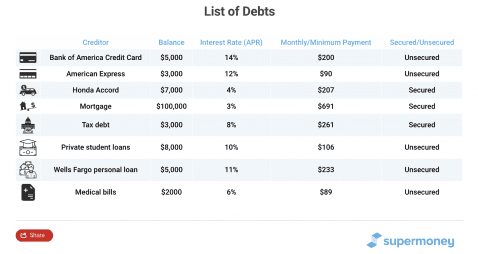

For many, this is the hardest step in our guide. After all, who has time to sit down and create a budget. Unfortunately, there is no way around it. If you worked through stage 1 of this guide, you already have a good start.Create a simple spreadsheet with a row for each creditor. Include auto loans, student loans, mortgages, credit cards, and any other source of debt. Include the balance you owe, the interest rate you’re charged, and the monthly payment. If it’s a credit card, include the minimum payment. In the last column, specify whether the debt is secured or unsecured. For example, a mortgage is a secured debt because the bank will take your home if you don’t make payments. Credit card debt, on the other hand, is unsecured debt.

The list may look something like this:

Remember that if you’re not sure about the balances in all your accounts, check your credit report. It will have a list of all the creditors that report to the credit reporting bureaus. The balances on your credit report may not be 100% accurate. Once you have a list of creditors, confirm the balances with them. Now you know the extent of your debt and the money you have available to pay it off, you have some serious decisions to make.

Although it is possible to do it all by yourself, some people benefit from talking to a professional personal finance counselor at this stage. If you think you could benefit from a better understanding of how to budget, improve your credit, and reduce your debt, consider hiring a credit counseling service, such as Consumer Education Services. Many of the budgeting and personal finance counseling services offered by these companies are free.

Step 2: Consolidate your debt and reduce interest payments

Debt consolidation allows qualified consumers to take out a new loan that pays off most or all their outstanding debt. However, it is not for everyone. Look at the questions in the first stage of this guide to determine if debt consolidation is a good option for you.

The purpose of debt consolidation is to combine all your existing debt from various sources into one loan.

This means that you only have to pay one loan payment a month instead of several smaller loan payments. Ideally, debt consolidation loans should have a lower interest rate than the rates you are currently paying to help you get out of debt.

What options are available for debt consolidation?

It boils down to three main options. You can:

- Get a personal loan.

- Transfer all your other credit card balances to one card.

- Apply for a home equity loan or cash-out mortgage refinance.

Personal loans

If your credit isn’t where it needs to be to get approved for a balance transfer card, consider applying for a personal loan. You won’t get any 0% APR offers, and the interest rate can be higher than that of a HELOC. But this alternative’s unsecured nature means you’re not risking any collateral.

A couple of things to keep in mind with personal loans:

- A lower interest rate isn’t guaranteed. Depending on your credit, you may not get approved for a loan. And if you do, the APR may even be higher than your credit card’s APR.

- Personal loans have a fixed repayment period and fixed monthly payments. Make sure you can afford the payments before accepting a loan.

Consolidating your debt can improve your credit score

Personal loans can also help improve your credit score. How? Well, 10% of your FICO credit score, the score most widely used by lenders, is based on your credit mix. Having a varied credit mix, such as personal loans, mortgages, and credit card accounts, can improve your credit score. Your credit utilization ratio on revolving accounts — your debt as a percentage of your available credit — is also an important factor when calculating your FICO scores. Moving revolving credit debt to a personal loan will lower your credit utilization ratio, which could improve your credit.

Purchasing a loan is like buying a used car. Prices vary wildly depending on whether you buy from a private owner or a dealership, as well as on the age, brand, and condition of the vehicle. Personal loans are also a highly competitive business where prices vary by provider. Different personal loans come with different rates, fees, and requirements, so check out what the best personal loans are to ensure that you choose thebest option for you.

SuperMoney’s loan offer engine makes it easy to compare your options across many different lending partners without affecting your credit score. You can also research product details and company reviews directly on SuperMoney’s personal loan review pages.

Balance transfer credit cards

Consider switching your credit card debt to a 0% APR balance transfer card. If you have $15,000 in debt and an average 15% APR, you could save $1,940 in interest during just 12 months of 0% APR. Combine a 0% APR balance transfer with an aggressive repayment plan, and you could repay your entire credit card debt in less than a year.

Remember, balance transfers are not always free. The APR may be 0%, but APRs don’t include balance transfer fees, which can be as high as 5%. There are balance transfer credit cards, such as Slate, that don’t charge transfer fees, but these are rare. This doesn’t mean you shouldn’t transfer your credit balance. Make sure you take into account these fees when calculating the pros and cons of a balance transfer.

Home equity loans

A home equity line of credit is similar to a credit card in that you have a revolving line of credit that you can use, pay off, and use again. The difference is that most credit cards don’t require collateral, while a HELOC uses your home as collateral.

A home equity line of credit is similar to a credit card in that you have a revolving line of credit that you can use, pay off, and use again. The difference is that most credit cards don’t require collateral, while a HELOC uses your home as collateral.Because of this setup, HELOCs are considered secured debt and have relatively low – and usually variable – interest rates. To illustrate, the average APR for credit cards in 2018 was around 16%. The average APR for a HELOC was about 5%.

The obvious advantage of using a HELOC to pay off credit card debt is that you can consolidate at a lower interest rate, even if you have poor credit.

However, it is not for everyone. You need to have substantial equity and there is the risk of losing your home if you don’t make payments on your HELOC or home equity loan.

Refinance secured loans

Refinancing your loans for shorter terms and lower interest rates can save you thousands of dollars and help you pay off your debt faster.

Mortgage refinancing

Mortgage debt represents 68% of American households’ debt. Imagine how much you could save if you lower your housing expenses by refinancing your mortgage. To illustrate, a 1% interest reduction on a 30-year $300k mortgage could lower your monthly payments by $178 and reduce the mortgage’s total cost by $64,000.

If you qualify for a mortgage refinance, consider a cash-out refinance to consolidate and pay off your other debts.

A cash-out refinance involves getting a new loan for a larger amount than the existing mortgage balance (ideally with a lower interest rate). As the borrower, you receive the difference between the two loans in cash to use as you please. In this case, you’ll be using the cash to pay off your high-interest debt like credit cards, a car loan, or a personal loan.

For instance, say you own a home valued at $250,000 and still owe $150,000 on the mortgage. You’ll have built up $100,000 in equity. You need an extra $25,000 to pay off some credit card debt and a car loan.

You can get a cash-out mortgage refinance with a new loan for $175,000 ($150,000 loan you’ll still owe on your home via mortgage payments, plus $25,000 cash). With this strategy, you can consolidate debt into a home loan and pay it off at a much lower interest rate.

Compare rates and terms from top mortgage refinance lenders now.

Student loan refinancing

The average debt of a four-year college student is $26,830, according to the Federal Student Aid Office. For some graduates, that could amount to more than half of their starting salary.

If you’re looking for ways to relieve your student debt burden, considering refinancing your student loans. You may qualify for lower interest rates if your student loans are older or if your credit has improved.

Compare the top student loan refinancing lenders to see which one offers the best feature combination for your needs.

Auto loan refinancing

If you decide to refinance your car loan, it can save you money and possibly reduce the length of the loan. SuperMoney’s auto loan offer engine makes it easy to compare the rates and terms of the top auto refinance lenders.

Say you owe $20,000 on your auto loan at 7% interest, and you’re paying $300 per month for the next 85 months, you’ll pay $5,401 of interest over the life of the loan. Here are interest reduction scenarios for comparison. Keep in mind–these loan refinancing scenarios are examples and don’t include any taxes or extra fees.

- Lower your rate to 5% interest and your monthly payments will drop to $280, saving you a total of $1,702.

- Reduce the interest rate to 4% and the monthly payment will be $271, saving you a total of $2,490.

- A reduction to 3% interest will lower the monthly payment to $261, saving you a total of $3,262.

Step 3: Choose the best payment method for you

oAll debt payment methods boil down to two main strategies: the snowball method and the highest rate first or avalanche method.

Pay the highest interest rate first – Avalanche method

This method works by organizing your debts by their interest rate. Identify the account with the highest APR. Make minimum payments on all the other accounts and pay off as much as can toward the account with the highest APR. This method is also called the avalanche method. If you don’t qualify for a 0% APR balance transfer card, this is probably the best way to reduce interest payments while getting out of debt.

Snowball Method

The snowball method requires you to pay as much as you can on your smallest debt while making minimum payments on the other ones. Once it’s paid, go on to the next smallest debt until you are debt-free. This method will probably cost you more in interest, but it has the advantage of providing quick wins, which could help you stick with the debt repayment plan.

Snowball vs. avalanche: which debt payment is best?

Let’s use an example to compare both methods. Imagine you have three credit card accounts:

#1 has a balance of $5,000 and a 13% APR

#2 has a balance of $8,000 and a 20% APR

#3 has a balance of $2,000 and a 12% APR

#2 has a balance of $8,000 and a 20% APR

#3 has a balance of $2,000 and a 12% APR

If you can afford to make $800 in monthly payments and follow the debt avalanche method (i.e. pay off the account with the highest interest first), you will pay $2,226 in interest and be debt-free in 1 year and 11 months.

Use the snowball method (i.e., start with the account with the smallest balance) and you would pay $2,786 in interest and take 2 years to be debt-free. In other words, you would pay an additional $559 in interest and take a month more to be debt free than those who start with the highest-interest accounts.

Although the debt avalanche method is clearly the rational way to pay off debt, humans are not always that rational. A study by a team of Kellogg School researchers found that people with large credit card balances are more likely to pay down their entire debt when they follow the debt snowball method. As any casino manager will tell you, the lure of small wins is powerful.

Really, it doesn’t matter which method you use, as long as you stick with your payments until you are debt-free. Our personal favorite is to use the “blizzard method.”

Blizzard method

Pay off your smallest loan to give yourself a boost of motivation. Now rank your loans by their interest rate (from the highest to the lowest) and pay them in that order. This method provides the psychological benefits of the snowball method and helps you to minimize interest rate payments.

Step 4: Make more money

Increasing your monthly income will allow you to put more towards repaying your debt.

Increasing your monthly income will allow you to put more towards repaying your debt.Get a side job

If you’re trying to get out of debt and have cut as many expenses as possible, it may be time to supplement your income. Thanks to today’s gig economy, it’s easier than ever to find “moonlighting” jobs that allow you to increase your income quickly.

If you want to earn some extra money pronto, consider one or more of the following side jobs.

Sell stuff

Admit it. You have way too much junk. The average household has $1,000 to $2,000 of potential cash in stuff they no longer use. Empty that basement. Reclaim your garage. Get rid of that storage unit.

Step 5: Desperate measures to get out of debt

But what if your financial situation is so bad no amount of budgeting, consolidating, refinancing, or extra gigs will make a dent in your debt? In most cases, the tools mentioned above are enough for a determined person to get out of debt. However, there isn’t always a way to get out of debt without help. In such cases, there are two tools to consider: debt settlement and bankruptcy. To find out if your situation warrants these such aggressive debt relief strategies work through the questions in stage 1 of this guide.

How does debt settlement work?

A debt settlement is an agreement between borrowers and lenders to make a lump-sum payment instead of the full amount owed. It is one of the most aggressive and effective debt resolution methods available. However, it is not a debt relief method you should take on lightly. Debt settlement will probably damage your credit score and force you to deal with debt collection agencies. It is a last-ditch resort that forces lenders to decide between forgiving a chunk of your debt or getting nothing at all.

Why would lenders consider forgiving part of your debt?

The threat of bankruptcy is what brings many creditors to the table. Lenders know that personal bankruptcy can discharge unsecured debt and prefer to get something than to be left standing with worthless promissory notes. If you can convince your lenders you cannot afford to pay your debt in full, they may agree to a discounted payment instead. How much of a discount are lenders willing to give? It all depends on your negotiating skills and your financial situation. You should also be aware that some of your creditors may refuse to work with the debt relief company you choose.

When should you consider a debt settlement?

As we mentioned above, there are no hard rules about when you should pursue debt settlement, but these are some useful guidelines we discussed above that are worth remembering.

You may want to consider it if:

- Your debt-to-income ratio is higher than 0.5. In other words, if your unsecured debt is 50% or more of your annual income.

- If it will take more than 5 years to repay your debts with your current discretionary income and you can´t increase your income or further reduce your living expenses significantly.

Here are a couple of things to consider when looking for a debt relief company.

Do they have minimum and maximum limits on the amount of debt you can enroll?

Most companies require you to have a minimum amount of debt, which is usually around $10,000. Some lenders, such as Freedom Debt Relief, accept lower amounts. Other companies also have a maximum amount of debt you can enroll, such as $100,000. You will need to find a company with requirements that match your needs.

What is their customer service like?

We typically don’t care about a company’s customer service until we run into problems or have questions. It is important to find out ahead of time about the level and quality of support provided by a company. You can do so by researching the support channels they offer (phone, email, live chat, etc.) and by reading reviews from past customers. Look for companies like Debtmerica Relief and Rescue One Financial, which are recommended by our community of users.

This guide will help you decide whether debt settlement is a smart option for you.

How does bankruptcy work?

Bankruptcy is a legal process by which individuals and businesses can eliminate or repay debts under the protection of the federal bankruptcy court. There are two types of bankruptcies: liquidation and reorganization.

Chapter 7 is the classic liquidation bankruptcy. As its name implies, it requires debtors to liquidate or sell their property to pay some of their debt. However, some types of property are protected by state and federal bankruptcy laws. In certain cases, debtors may have little to pay once state exceptions (i.e., protected property) are applied.

Chapter 13 is the most common reorganization bankruptcy. With this type of bankruptcy, debtors get to keep all, or most, of their property. However, unsecured debt is not always discharged. Instead, it is reorganized into affordable payments. If a debtor completes the repayment plan (three to five years of monthly payments), pending unsecured debt is discharged. The catch is unsecured debt is generally not discharged until debtors complete the three to five years repayment plan. However, the completion rates of Chapter 13 bankruptcies are extremely low. Only a third of debtors complete the repayment plan.

This guide teaches you everything you need to know before you decide about bankruptcy before you make up your mind.

Getting out of debt guide for servicemembers

It is particularly important for members of the military to keep their finances in order because failing to do so could hurt their career. For instance, if you have a bad credit history, you could lose your security clearance or not qualify for a promotion (source). The unique challenges of military life can make it particularly difficult for servicemembers to manage their personal finances during their time in the service. Federal and state legislatures acknowledge this by providing special protections to active duty military members.

If you are an active-duty servicemember and you’re struggling with debt, follow the steps set out above. They apply to both servicemembers and civilians. However, you should also take into account the following laws before you make any important decisions. They provide special protections that could save you a lot of money.

The Servicemembers Civil Relief Act (SCRA) and debt

The SCRA offers extra protections to servicemembers facing financial difficulties during uniformed service. Here is a summary of the key protections included in the Servicemembers Civil Relief Act:

1: You can reduce the interest rate of any pre-service loan to a maximum of 6%

You just need to notify your lender in writing. Include a copy of your active duty service orders or a letter from your commanding officer with the date you start active duty service. If you qualify, this is an excellent opportunity to reduce your interest payments and focus on paying off your debt while you’re away.

2: Servicemembers receive additional protections against default judgments in civil cases

For example, if you are being sued in a civil action, courts can issue a default judgment against you if you fail to appear. If you are an active-duty servicemember, courts cannot issue a default judgment before it appoints an attorney to represent you.

3: Protection from foreclosure

Servicemembers cannot be foreclosed without a court order, as long as they took out the mortgage before entering active duty service. Upon request from the servicemember, courts are required to pause or stay a foreclosure if the active duty service is affecting the homeowner’s ability to pay the mortgage.

4: SCRA prohibits creditors from repossessing your personal property

This protection would prevent lenders from repossessing the property, such as a car, a boat, or a TV if it was purchased or leased before entering active duty service. The protection also applies if the servicemember made a deposit or installment payment on the item before leaving for active service.

5: Servicemembers have the right to terminate residential and vehicle leases without penalty

If you receive deployment orders or a Permanent Change of Station (PCS) for at least 90 days, you can terminate a housing lease without penalty. If the deployment is for longer than 180 days, you may also be able to terminate a vehicle lease without penalty.

The Miltary Lending Act and your debt

The MLA is a federal law that provides special financial protection to borrowers who are active-duty servicemembers (source). These protections include:

A 36% interest cap

The Military Lending Act sets a maximum Military Annual Percentage Rate of 36%. The MAPR is similar to a regular annual percentage rate but with more restrictions on the fees that must be included in the rate. This cap applies to most loans, including payday loans, tax refund loans, auto title loans, unsecured personal loans, and lines of credit

No mandatory allotments

Lenders cannot require a servicemember to set up a voluntary military allotment to pay for a loan.

No prepayment penalty fees

Creditors cannot charge a penalty for paying a loan or part of the loan early.

No mandatory waivers of legal rights

Lenders cannot require borrowers to accept mandatory arbitration or give up their Servicemembers Civil Relief Act protections.

What’s next?

To get out of debt is only the beginning. Once you’re free of debt, it’s time to save and invest in your future. If you’re like most people, the final goal is to be financially independent and retire early.

Read our investment guide and start working toward financial independence today.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: