How to Remove an IRS Levy: The Definitive Guide

JW

Last updated 03/19/2024 by

Jessica WalrackHas the IRS threatened to levy your assets, bringing your daily life to a screeching halt? It’s a stressful situation, but there is still hope. The IRS wants to collect as much as they can from taxpayers without causing so much hardship they can’t afford basic living expenses. That means they’re often willing to negotiate. How can you make that happen? Read on to learn what you need to know about getting a levy release and who can help you along the way.

End Your IRS Tax Problems

Get a free consultation from a leading tax expert.

It's quick, easy and won’t cost you anything.

What is an IRS tax levy?

An IRS tax levy allows for the legal seizure of a person’s assets to cover their tax debt. These assets can include the funds in a bank account (bank levy), wages (wage levy), personal property, real estate, and vehicles. While a lien is a claim to a person’s assets, a levy gives the IRS the power to take possession of them.

The IRS uses a stick and carrot approach with taxpayers. Tax relief programs, such as offers in compromise and installment agreements, are the carrot. They encourage taxpayers to pay as much of their tax debt as possible without causing undue hardship. Tax liens and levies are the stick that provides taxpayers with an additional incentive to repay their taxes.

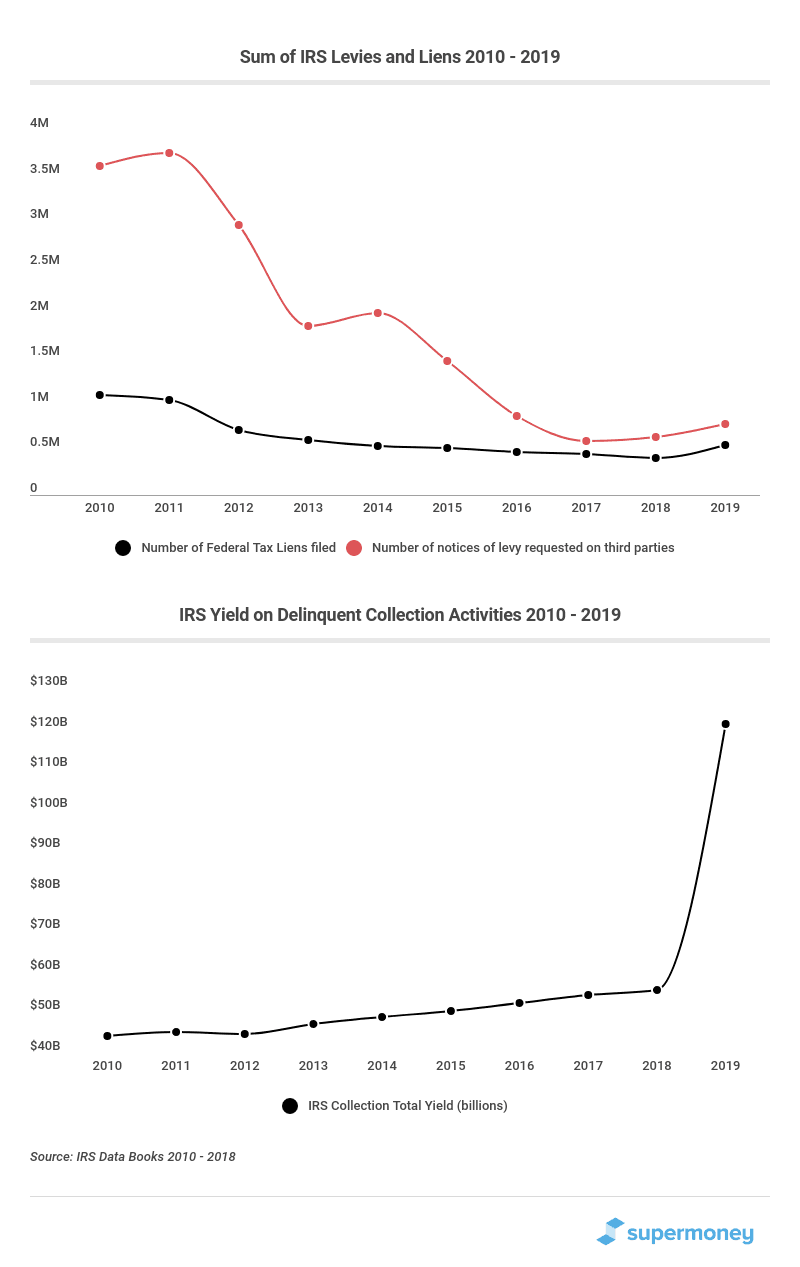

The good news is that in the last 10 years, the IRS has reduced the number of liens and levies filed. This has not affected the IRS’s ability to collect taxes. On the contrary, the IRS’ collection yield has increased dramatically. However, that’s little comfort if you have been hit with an IRS levy.

Should you be worried about a tax levy? Learn about the IRS collection myths vs. realities.

What’s the difference between tax liens and tax levies?

Sometimes the two terms – tax lien and tax levy – get confused. While they are related, they are actually two different steps in the same process.

Tax lien

A tax lien is a legal claim against your property. This property may include real estate, personal property, and financial assets like a bank account. When you have a tax lien against your property, you cannot sell it without first paying the IRS whatever monies you owe.

Tax levy

A tax levy is the actual seizure of the asset to pay off a tax debt. If you don’t pay your taxes or arrange to settle your debt, the IRS may seize and sell any of your real or personal property. This includes both property and your current and/or future income.

What are the different types of levies?

When speaking about levies, you may hear of different types. Here’s a quick overview of the different types of levies the IRS may issue.

- Bank levy: When the IRS issues a bank levy, it places a hold on the money in your bank account. After the hold begins, you have 21 days to pay the back taxes before the bank sends the funds to the IRS.

- Wage levy: A wage levy occurs when the IRS contacts your employer or client and requires they pay part of your wages to it.

- Property levy: The IRS can seize your property or house and sell it to pay off your tax debt. After seizing it, it will provide a notice of sale and announce the sale to the public. You typically have 10 days from that public notice before the sale is made. The profit of the sale goes first to the costs involved with seizing and selling the property. Then, it will go to your tax debt. If you are entitled to a refund, there is a process through which you can request it.

These are three of the most common type of IRS levies. Typically, the IRS will go for the bank levy and wage levy first. They will track down your accounts using your name and social security number (SSN) or taxpayer identification number (tin).

Why does the IRS prefer cash to personal property?

The answer lies in Section 6331(f) of the Internal Revenue Code, which stops the IRS from levying when “the taxpayer has insufficient equity in the property.” To illustrate, if you own a $20k car and you owe $20k on it, the IRS will not seize it. The same applies if you’re upside down on your mortgage. Even if you own an asset outright, such as jewelry or an expensive painting, agents need to request managerial approval and send the request to an IRS liquidation expert. Needless to say, IRS agents prefer to avoid the additional time and expense and look for ways to get taxpayers to pay in cash.

Can the IRS take your whole paycheck?

Unfortunately, yes, the IRS can levy your bank and take your whole paycheck. However, it should never be a surprise. This only happens to taxpayers who owe back taxes and failed to respond to a series of persistent notices that state the intent to levy (see more on this below).

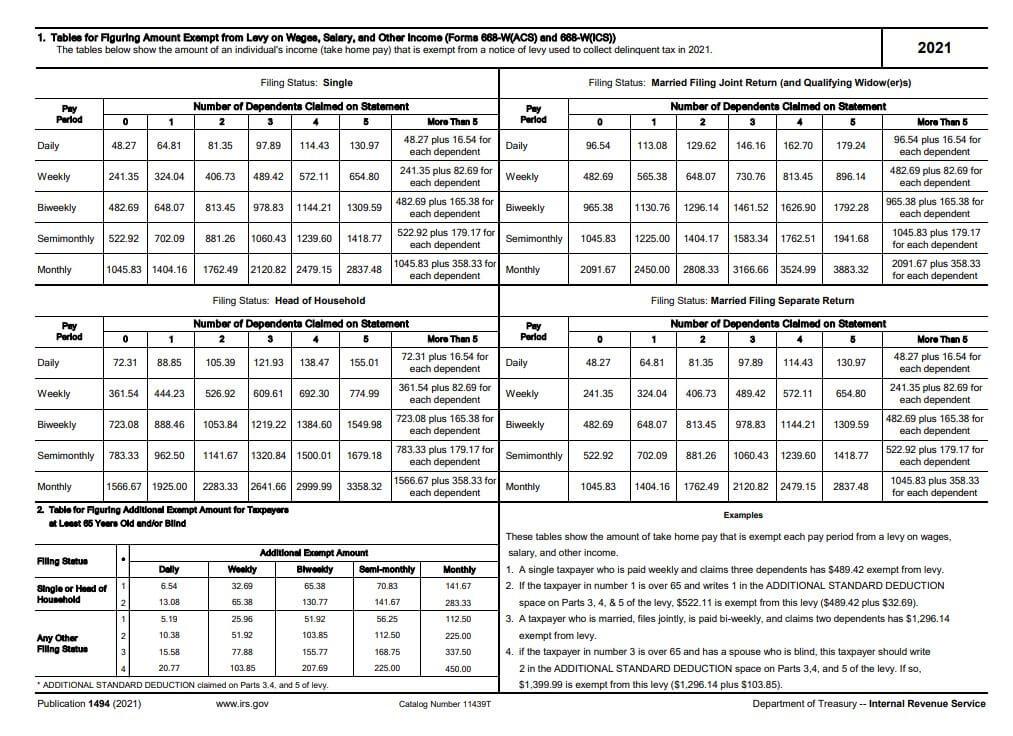

The IRS can also levy your wages directly from your employer. When they do, they’ll contact your employer and request part of your paycheck. You can review the amount exempt from the levy here.

How much can the IRS take from my paycheck?

The percentage of your wages you’ll keep during an IRS garnishment is based on the standard deduction and the number of personal exemptions you can claim. The IRS uses the tables in Publication 1494 to calculate how much of a taxpayer’s income (take-home pay) is exempt from a wage garnishment (or a notice of levy) to collect delinquent tax in 2021.

The IRS bases its guidelines on what it deems will leave you enough money for regular living expenses. Typically, the IRS will garnish up to 15% of your wages. However, if you have other income sources, the IRS may allocate the exemptions to your other income sources and levy on 100% of your wages from a particular employer. The IRS can also levy any extraneous income supplements, such as bonuses or commissions.

That’s why it’s essential to contact the IRS to make other arrangements if possible. Garnishment can upend your lifestyle and shatter your budget — you should pursue alternatives if possible.

If you’re unsure how to set up an alternate payment plan, consider hiring a tax attorney to help you negotiate with the IRS.

How to stop an IRS levy

If you begin receiving notices about being levied, you can stop the proceedings by getting in touch with the IRS as soon as possible. Make contact and work out a payment agreement. Even if you are facing economic hardship and can’t pay, it’s better to get in touch. There are many tax relief programs to help taxpayers who are unable to pay their full debt load. For example, you could try the following:

- Set up an installment plan. An installment plan is an agreement to repay your tax debt in an extended period of up to six years. Agreeing to the plan will halt other collection activities, like a lien or levy.

- Submit an offer in compromise.When you can’t afford to pay a tax debt in full, you can offer the IRS to pay as much as possible. When you do so, collection activities will pause. However, if the offer is declined, they will resume, and you will have to make another arrangement.

- Currently not collectible status (CNC). If you are going through economic hardship and can prove it to the IRS, they may put you on this status, temporarily pausing collection efforts. You will need to prove that it’s not worth the effort to collect.

When facing an impending levy, get in touch sooner rather than later. If you work with any of the above programs, the IRS may approve a levy release.

How long does an IRS bank levy last?

How long until the IRS will release the levy? It lasts until you’ve paid off your tax debt or until you come to another agreement with the IRS. It is possible to get a levy released in the time it takes to call the IRS and come to a payment extension agreement.

With a bank levy, for example, the IRS will freeze the funds in your bank account for 21 days before taking them. But if you call the IRS and make an agreement before this time is up, you’ll immediately regain access to the funds.

However, some agreements take longer than others. If your situation is complicated and you need to provide extensive documentation, it can take months to get the levy released.

It’s best to contact the IRS right away and see what your options are. Also, consider hiring a tax professional to do so on your behalf.

How to get an IRS tax levy release

Once the IRS has placed a levy on your bank account, wages, or other property, you need to get in contact immediately to request a levy release. The IRS may release you from the levy for any of the following reasons:

- The IRS tax levy prevents you from meeting your basic necessary living expenses (financial hardship).

- You already paid the amount in full.

- The statute of limitations on the debt has expired.

- Releasing the levy will enable you to pay the amount owed.

- You agreed to an installment arrangement.

- The amount collected is more than the amount you owe.

If your request is denied, you can appeal it. You can also file claims to have your property, or other assets returned to you.

If you get a levy release but still owe the tax debt, you will need to make arrangements to pay it.

What can the IRS levy?

When you owe a tax debt, the IRS can levy everything a person owns or earns. This includes wages, money in bank accounts, retirement funds, vehicles, boats, real estate, tax refunds, and anything else that could be liquidated for value.

What property is exempt from IRS levies?

The existence of equity is not the only limitation the IRS faces. Section 6334 of the Internal Revenue Code specifically lists types of property excluded from IRS collection procedures.

These exemptions include:

- “Necessary clothing.” Unfortunately, your Gucci handbag and your Louis Vuitton loafers don’t qualify as necessary.

- Fuel, provisions, furniture, and personal effects are exempt as long as they don’t exceed $6,250 in value.

- Unemployment benefits and workmen’s compensation.

- Investment real estate. Your home and your rental properties are exempt as long as the amount you owe is $5,000 or less. For larger amounts, real estate can be seized.

- Principal residences are exempt unless a judge or magistrate of a district court of the United States approves the levy in writing.

This is by no means an exhaustive list, but it gives you an idea of the restrictions IRS agents must follow when seizing property.

Regardless of what IRS agents may tell you, it is unlikely the IRS will place a levy on a home, car, furniture, or other types of equipment, which tends the be the stuff taxpayers are more concerned about losing. Although you shouldn’t be complacent, there are options available for those who want to resolve their tax debt problems.

IRS Collections Process: The Five Final Notices

The IRS must follow due process and provide notice of intent before initiating a levy on your property. According to the Internal Revenue Code (Sections 6330 and 6331), this includes sending a final notice to taxpayers. The IRS likes to keep taxpayers guessing, so it sends a series of five collection notices that, to the layman, all look like a final notice.

- CP 14: This is the first “final” tax levy notice you’ll get. It simply tells you your balance is due.

- CP 501: Just in case you missed the first letter, here’s a reminder that your balance is due.

- CP 503: Anyone home? 2nd notice that your balance is due.

- CP 504: Final notice of balance due. Except it isn’t really the final notice.

- CP 90: “The” final notice of intent to levy and notice of your right to a hearing. This is the real deal. It is the only notice that enables the IRS to garnish your wages, levy your banks, and take possession of your properties.

Going through this correspondence cycle can take six months to complete. The IRS typically sends a follow-up letter every five weeks. Notice the IRS is not required to send all those letters. The first four are courtesy notices.

Why is this important? If you still haven’t received the CP 90, any negotiations with the IRS will be without the direct threat of a levy.

Even after you receive a CP 90, the IRS still has to wait 30 days to give you time to file an appeal.

Notice: In cases where there is a large balance due, the IRS will sometimes send the CP 90 right off the bat.

A Levy Notice will be:

- Delivered in person;

- Left at your home;

- Left at your place of business; or

- Mailed to your last known address by certified or registered mail return receipt requested.

The IRS may levy your state tax refund as well. If they do, you will receive a Notice of Levy on Your State Tax Refund.

Know your rights—Resolve an issue with the IRS

You have the right to speak with an IRS manager to review your case or request a Collection Due Process hearing. You must file a request within 30 days with the IRS office listed on your notice(s).

The purpose of this hearing is to discuss the following issues:

- You paid all you owed before you received the levy notice.

- The IRS assessed the tax and sent the levy notice when you were in bankruptcy.

- The IRS made a procedural error in an assessment.

- The statute of limitations expired.

- You lacked the opportunity to dispute the assessed liability.

- You wish to discuss the collection options.

- You wish to make an innocent spousal defense.

This last one, an innocent spousal defense, only applies if you meet all four of the following criteria:

- You filed a joint income tax return.

- There was a “substantial understatement” of tax due to “grossly erroneous items” of one spouse.

- You didn’t know about the substantial understatement and had no reason to.

- It is inequitable to hold you liable.

After your hearing, the Office of Appeals will issue a determination. You then have 30 days to contest that determination.

Bank charges you pay due to an IRS mistake may be reimbursable. Use Form 8546 to file an appeal.

Two reasons to take the IRS seriously

As of 2015, the U.S. Tax Code has over 10 million words in length, and that doesn’t include tax-related case law, which is vital to understand how the tax code should be interpreted (Source). That’s crazy. A diligent taxpayer would need to spend eight hours a day for three and a half months just to skim through the tax code at 200 words a minute. What’s even more depressing is the tax code grows every year. If the current pace holds, it will have 100,000 pages by 2050.

However, based on those rules, the IRS can arrest you and put you in prison for tax evasion. In 2015, the IRS sentenced 3,092 taxpayers out of 3,208 indicted. That is a 96% conviction rate for those keeping score (source).

So it is no wonder the IRS has become the nation’s bogeyman, a quasi-mythical monster that can snatch you away for the slightest misstep.

Many of our readers express concern about the IRS showing up one day and seizing their home, placing a levy on their income, or shutting down their business.

Debt, particularly tax debt, generates so much fear and stress it has serious effects on health. According to a 2014 report published by the BMC Public Health journal, being seriously behind on debt repayments is a predictor of mental and physical health problems (source).

Get help from a tax expert

Owing money to the IRS is never fun. When you start hearing about tax levies, the problem is about to become seriously disruptive to your life. But that doesn’t mean you always need a tax lawyer and a CPA holding your hand. If your debt is small or you’re 100% sure you have nothing to fear from an audit, it may be safe to give it a shot. However, if you owe a lot ($10,000 or more) or there is a chance your financial statements could trigger an audit, it would be wisest to ask for help.

Hiring a tax relief expert can take some of the stress out of the situation while helping you to get the best results. When facing the IRS alone, you are at a disadvantage. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee and charge competitive rates. Check out which tax relief company is the best fit for you.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: