A Personal Loan With A Cosigner? It Can Lower Your Rates and More

Last updated 02/12/2026 by

Andrew Latham

Summary:

Finding a cosigner can be a great way to qualify for a personal loan with better rates and terms, but it can be risky. If someone agrees to cosign your personal loan, the loan will show up on both of your credit reports. Your co-signer will also be on the hook for the loan payments if you default on the loan. This guide will help you lower your rates (and improve your terms) with a cosigner while avoiding some of the pitfalls that go with the territory.

selLooking to sidestep high interest rates and expensive fees on your personal loans to qualify for a higher loan amount or better monthly payments? Unless your credit score is above 720 and you have a prolific credit history, you won’t qualify for the best rates and terms. Nearly one in three consumers (31%) have subprime credit, according to a recent study by Experian. Subprime is here defined as any score under 670 (out of a range of 350 to 850). Borrowers with a poor or subprime score often find it difficult to qualify for a personal loan. When such borrowers do qualify, their interest rate is typically much higher than the rate lenders will offer consumers with good credit. As of January 2018, the average APR for a 48-month auto loan was 5.30%.

One solution is to have a cosigner with good or excellent credit, with superior credit reports and FICO score, help you obtain more favorable terms. A loan with a cosigner provides a layer of insurance for the lender because if you default, your co-signer must pay the debt.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is a cosigner?

A cosigner is a trusted peer, usually, a close friend or family member, who promises to pay for a loan if the main borrower doesn’t. Cosigners are beneficial for both the lender and the borrower. Lenders love cosigners because they reduce the risk of a loan default. And borrowers benefit because they qualify for lower interest rates and fees.

Who provides cosigned personal loans?

Most types of loans can include a cosigner, and cosigning is common with mortgages, auto loans, and student loans. However, not every lender accepts cosigners, and only a few online lenders will allow a cosigner on an unsecured personal loan. Some banks, and more than one credit union, also allow a cosigner for a personal loan. The table below includes lenders that do allow cosigners.

Few major banks offer personal loans these days, though Citibank and Wells Fargo still do, and both allow cosigners. Credit unions are often an excellent source of credit because they work with consumers to qualify and secure lower interest rates. In addition to banks and credit unions, you also have the option of going with the online lenders listed above.

When is a cosigner a good idea?

There are several instances where you’ll want to consider looking for a cosigner. The first is where you have bad credit or no credit at all. If you have a poor or subprime credit history or you don’t yet have a FICO score because you’ve never applied for credit, a loan with a cosigner may raise your odds of getting a loan with competitive rates and terms.

Another instance is when you’ve already failed to qualify for a personal loan. If your loan application was just denied, bringing a cosigner on board gives you a shot at getting approved.

Finally, if a lender offers you a loan with unattractive loan terms, such as a very high interest rate or a smaller loan amount than you need, finding a cosigner may improve your loan options.

However, your first step should always be to see what kinds of offers you can prequalify for when applying alone. This process won’t affect your credit score, and it will be a useful reference point if you decide to re-apply with a cosigner. Ready to see what you might qualify for? This information is free.

Can a lender require cosigners?

Yes and no. Lenders cannot require that you have a cosigner on a personal loan if you meet their income requirement and have a sufficiently good credit score to qualify for the loan on your own. However, if a review of your application shows you don’t qualify, a lender can ask that you find a cosigner. In nearly all cases, you will get better loan terms, particularly a better interest rate, with a cosigner who has a good credit report and stable income.

Who can be a cosigner on a loan?

A cosigner can be almost anyone you trust, including a parent, guardian, spouse, another relative, or even a close friend. Your loan cosigner should have a good to excellent credit score and a steady income (and an employment history indicating income will remain steady) and should understand the risks associated with serving as your cosigner. Namely, anyone who cosigns your personal loan agrees to make payments should you fail to do so.

Of course, only cosigners with excellent credit and a long credit history will qualify you for the lowest rates. But even the most reputable cosigner won’t entirely negate your own credit situation. Even if your cosigner has great credit, having never missed a credit card payment, or been overdrawn on a bank or credit union account, you may not qualify for the best rates if your credit history and debt-to-income ratio are considered high-risk. Spotty payment history, large debt from student loans or credit cards might make even a loan with a cosigner insufficient.

And remember—if you fail to make your payments, responsibility for the debt will fall to your cosigner. This can seriously strain your relationship. Make sure your cosigner understands this risk and trusts you enough to take it.

The difference between a cosigner and co-borrower

Both cosigners and co-borrowers share responsibility for paying the loan. However, a co-borrower (also known as a joint applicant) also receives a share of the loan money and usually shares the responsibility of paying the loan from the start. A loan with a co-borrower is a joint loan, a different loan type than cosigned loans from personal loan lenders.

In contrast to co-borrowers, Cosigners do not receive any money from the loan and (ideally) won’t have to make any payments. Only if the primary borrower defaults will the cosigner become responsible for the debt.

This distinction is particularly clear with a secured loan, such as a mortgage or a car loan. In these cases, a co-borrower appears on the property’s title and shares ownership of the security, while a cosigner does not.

The pros and cons of having a cosigner on your personal loan

Loans with a cosigner get you access to credit and borrowing terms that wouldn’t be available to you as a solo applicant, including a lower interest rate. However, it also has its disadvantages. Here is a summary of the pros and cons of applying for a loan with a cosigner.

Should you cosign a personal loan?

Only if you really trust the borrower. A personal loan with a co-applicant is good for the borrower but not always for the cosigner. If the worst happens and your co-applicant defaults on the loan, you’ll be responsible for paying it off in full.

Whether you’re the borrower or the cosigner, cosigning a loan is not something you should take lightly. You have more to lose than money and your credit score. Sometimes, close friendships and family ties become collateral damage when a cosigned loan goes bad.

Before cosigning a loan application (or recruiting a cosigner to so do), consider the following:

Cosigning a loan is risky business

According to a 2016 report, 38% of cosigners had to repay the loans they guaranteed. Those are scary odds. No matter how much you trust the borrower, unforeseen circumstances can get in the way of timely payments. You should only cosign a loan you could afford to pay if the borrower stopped making payments. After all, there’s a good chance you’ll have to do so.

Negotiate the terms

As a cosigner, you can negotiate the terms of your liability with the creditor. The Federal Trade Commission recommends cosigners include a clause that limits liability to the principal of the loan. Consider a clause like: “The cosigner will be responsible only for the principal balance on this loan at the time of default.” It could save you from paying interest for a long time.

Cosigning a loan will affect your credit score

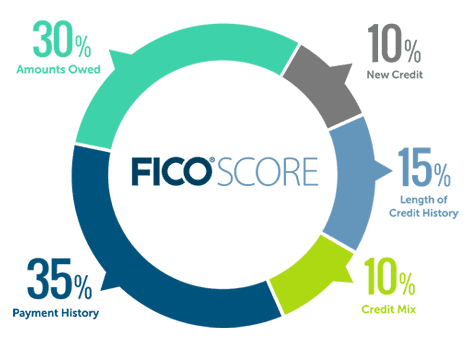

Lenders consider loans you cosign as debt. This will increase your debt-to-income ratio, which determines 30% of your credit score (FICO). Be sure not to cosign any loan amount that will drastically throw off your ratio.

Request monthly statements

Cosigners have the right to receive monthly statements for the loans they guarantee. If you cosign a loan, ask the lender to send you monthly statements. The statements will alert you to any missed payments that could further damage your credit score.

Steps to getting a personal loan with co-signer

Getting a cosigned loan is a two-step process. First, you need to find a lender who offers cosigned personal loans (see below). Second, you need to find someone to cosign on your behalf.

The first place you should look is to relatives who are invested in your success and your financial independence. Let them know that you understand the risk and that you take paying back the loan seriously. When you have a cosigner in your corner, it’s time to consider lenders and the terms they offer.

A comparison of a single-signed loan vs. a cosigned loan

Let’s assume that you’re not sure that the best personal loans use cosigners. If you use a cosigner, that individual’s superior creditworthiness and your combined debt-to-income ratio should cause your application to be viewed more favorably by personal loan lenders. That means a lower interest rate. How much lower? It depends on the lender as well as you and your cosigner’s combined credit application.

For example, let’s say that you seek a loan amount of $10,000 to be repaid over 3 years, your credit score is 610, and your annual income is $35,000.

Your co-signer has a credit score of 775, an annual income of $75,000, and low overall debt.

Using a lender such as LendingClub, you apply both with and without a co-signer.

- Without a cosigner: APR 32% Monthly Payment $435.54 Total Cost $15,679.44

- With a cosigner: APR 7% Monthly Payment $308.77 Total Cost $11,115.72

Bottom line: With a cosigner, you would save $126.77 on monthly payments and $4,563.72 over the life of the loan.

As you can see from this example, getting the best personal loans means getting the best terms; the details are essential. Often, a cosigner can help you both access credit and do so at the best rates. Learn more about these online personal loan lenders and read reviews from recent customers before you apply. Different personal loans come with different rates, fees, and requirements, so check out what the best personal loans are to ensure that you choose the best option for you.

How to get a personal loan without a cosigner

Even without a cosigner, there are ways for borrowers with bad credit to get a loan. The rates will be higher, but on the bright side, paying off a new loan on time can improve your credit going forward.

Of course, there are cheaper ways to improve your credit than getting a personal loan. If you don’t need money straight away, consider getting a credit-building account.

If you need the money now, several online lenders offer joint personal loans to people with bad credit and limited credit histories. SuperMoney’s personal loans database allows you to filter lenders based on the features that matter to you.

However, different personal loans come with different rates, fees, and requirements, so check out what the best personal loans are to ensure that you choose the best option for you.

Here are our top lenders for borrowers with bad credit:

Getting started

Ready to get started? Your first step is to determine what kinds of rates and terms you can qualify for without a cosigner. Compare recommended lenders with competitive rates with SuperMoney, or find out what you prequalify for just by answering a few questions. And if you can’t qualify for the personal loan of your dreams alone, talk to your financially stable friends and family about cosigning.

Curious about how personal loans can benefit you and your spouse? Explore our in-depth guide on joint personal loans, including tips, benefits, and key considerations: Personal Loans for Married Couples.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

AddTable of Contents