How Much Money Do You Need To Live Off Interest?

SL

Summary:

How much money you need to live off interest depends as much on your desired lifestyle as it does on the fundamentals of your investments. Also, how big those investment accounts get and how much interest they generate depends a lot on the strategies you chose to employ to build your wealth.

For the vast majority of people, having enough money to live off the interest and never do another day of work is the holy grail of personal finance. It actually takes a remarkably small amount of capital to produce the annual income necessary to survive.

However, everyone has a different standard of what “living” means when it comes to personal finance. And once you decide to retire and live off your investment interest, there are many other factors to take into consideration as you move toward your golden years.

In this article, we’ll take a look at how much interest you may need to retire comfortably, where you may be able to earn this interest income, and the additional taxes and fees you may have to pay on your interest and investments.

Compare Brokerage Services

Compare multiple vetted providers. Discover your best option.

The basics of an interest-only retirement strategy

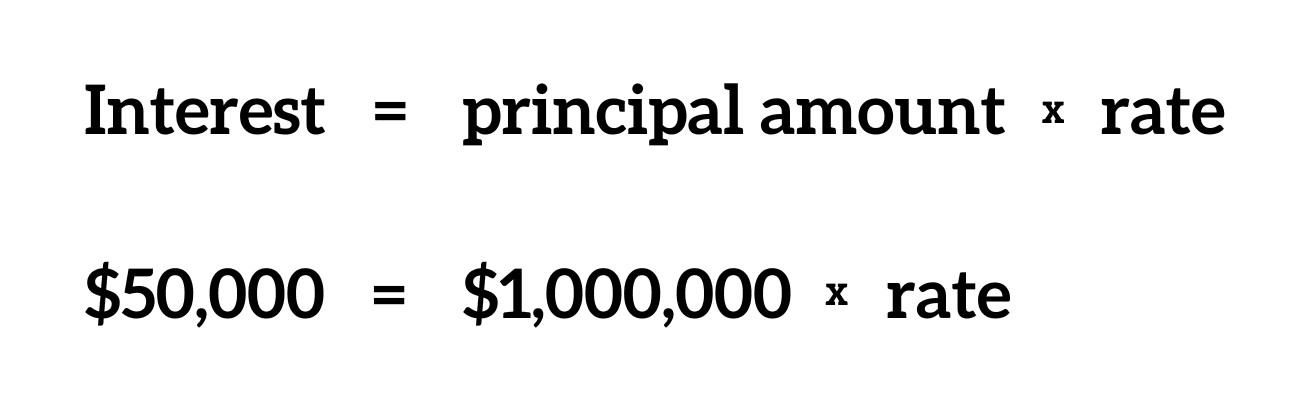

The basic equation is pretty simple: You calculate how much money you want to spend on your life every year, and your investment interest needs to produce at least that amount after taxes.

Let’s say you spend $50,000 on personal expenses and you have $1,000,000 in the bank. That means you need an interest rate that produces $50k from your principal amount minus taxes and fees.

Using this equation, you can determine that you need at least 5% interest every year to comfortably live off of interest. But there’s a slight problem with this equation: Where can you earn that much interest? And how will you earn that million dollars? Even if you can bank $20,000 a year from the time you turn 18 — a very unsafe assumption — it’s going to take you until you’re 68 years old.

How to earn the principal for your retirement income

It can be intimidating to think about the income you’ll have to produce to reach your retirement dreams. Luckily, there’s more than one way to earn the interest you need.

Compound interest income

One secret to making the money you need comes from investment accounts and their interest earnings. Compound interest — earning interest on your interest — is key to making the money you need to retire early and live comfortably.

Let’s say you have $1,000 at a 10% interest rate paid once as a lump sum on the principal amount. In 10 years, you’ll have $1,100 dollars.

However, compound interest is paid out continually — sometimes by the day, sometimes by the month — and because of that, you end up with even more money. So that $1,000 paid in compound interest over 10 years actually makes you $2,707.04.

Investing with the Rule of 72

Another important way to earn income faster is by investing. Stocks don’t pay interest, but they do pay dividends and can increase in value. Though the risk level is higher, without the stock market, it’s going to be much harder to get your bank account where it needs to be before your golden years.

Fortunately, if you invest wisely, you’ll get some additional help from the Rule of 72. This rule says that, provided your stocks rise in value by 10% every year, you’ll double your money about every 7 years. Let’s say you start with $10,000 at 10% when you’re 18. If you maintain that level of performance, you’ll have $20,000 by the time you’re 25, $40,000 when you’re 32, $80,000 at 39, and so on. By the time you’re 60, you’ll be sitting pretty on $640,000.

And that’s if you add nothing to that initial investment ever. That’s a lot of money and more than halfway to that million dollars a few years before your expected retirement. But before you start investing, you’ll have to open a brokerage account. Take a look at some of the brokerages below to get started.

Pro Tip

Naturally, if you keep adding to that initial investment, you’ll reach your ideal number a lot sooner. And as you get older, you can expect to add more money, not less money.

Plus, with an excellent financial advisor or certified financial planner, you may be able to do much better than 10% with quality growth and dividend stocks in your investment portfolio. The secret? Start as early as you can.

Utilize mutual funds and other portfolio options

Of course, achieving a reasonable fixed income that covers annual living expenses from interest alone doesn’t mean taking a Wild West investment strategy. Your market gains may be enough to set up a nest egg, but the nest itself should include a variety of secure assets. This could include some of the following as well as a healthy mix of stocks:

- Certificates of deposit (CDs). CDs are low-risk investment accounts that can earn around 3% interest on your principal amount. However, you can’t touch that money until the term ends.

- Mutual funds. These funds can include exchange-traded funds (ETFs) and index funds, both of which are baskets of securities. Since they aren’t individual stocks, you won’t experience such severe volatility.

- Money market accounts. Think of a money market account as a savings accounts with some features of a checking account, like checks and a debit card.

- Treasury bonds. Treasury bonds are offered by the government and pay you interest on a regular basis, usually once or twice a year.

- High-yield online savings accounts. One of the lowest-risk places to stash your money is a high-yield savings account, which tends to offer between 1% and 3% interest on your savings. To get the highest interest rates, you’ll likely have to look for an online-only account.

Pro Tip

Remember that your financial goals should never be to make as much money as you can without regard to risk. If you can retire early living off interest, fantastic, but that shouldn’t come with the possibility of going broke.

To get some further advice on where to invest your money for retirement, speak with one of the investment advisors below.

How do you know when you have enough money?

This is the big question for interest-only retirement, and a great deal of that has to do with the level of financial freedom you’re comfortable with. Some people have very few desired expenses like traveling or fine wine, and they’re happy as long as they have enough income to meet current expenses.

However, you may prefer to have a larger nest egg should the worst happen. Or you may want to live below your means day-to-day so you can splurge on a fabulous vacation down the road. No matter what you want, there are some basic practical realities that everyone should take into account regardless of their lifestyle if they want to retire early.

Pro Tip

To figure out your yearly expenses, start tracking how much money you spend daily and monthly. From there, you can create a budget if you feel you’re spending too much or simply use your tracking as a guide for how much you should have each month during retirement.

Inflation rate

Inflation means your income needs will go up over time to maintain your standard of living. A conservative estimate of about 2% average inflation per year means that $10,000 in today’s money will require $80,000 twenty years from now. Your retirement investments will need to keep pace with that, or your monthly income will buy less and less every year.

That means increasing your principal amount in your accounts, increasing account performance, or reducing expenses. Make sure you have a plan in place. A simple strategy to live off of interest alone won’t get the job done for any early retirement strategy unless you really accumulate assets aggressively beforehand. Instead, make sure your money works for you at a rate that keeps up with inflation.

IMPORTANT! Don’t be afraid to reach out to a financial advisor for further guidance on how to plan for inflation. Not only can they help you plan your future expenses, but they can also offer advice on how to start saving or investing today.

Taxes, fees, and expenses

In addition to planning for unexpected expenses, don’t forget to account for the taxes and fees charged on your interest income and investments. While investing in the stock market is free, you may have to pay capital gains taxes on any earnings you get. Also, unless you do all the work yourself, you may owe fees to any brokerages you use when investing. And if your brokerage actively manages your accounts, expect to pay a little extra.

Any money you have in an individual retirement account (IRA) will also be taxed. However, when you’ll be taxed depends on the retirement account you set up. You can fund traditional IRAs with pre-tax dollars, though you’ll have to pay taxes on any withdrawals you receive. On the other hand, you can contribute after-tax dollars to Roth IRAs, meaning you won’t be taxed on them again.

IMPORTANT! Remember that you can have money in both a traditional and Roth IRA, which could help you balance your tax dollars.

So how much money do you need to live off interest?

As you can see, this is a highly personal question, but there are some general guidelines to shoot for. First, since you’re retired, you won’t have as many expenses. Plan on needing about 70% to 90% of your current monthly expenses covered to be safe.

Second, reduce your expected expenses to a number you’re comfortable with and do some basic math. If you need $5,000 a month, then you need $1,000,000 at 0.05% interest. But remember that in order to rely on compound interest, you can’t take any interest payments.

Finally, your investments and savings will probably not stay stable after you call it quits. Make sure your financial advisor understands your goals and helps you craft a retirement strategy that will account for time and market fluctuations.

FAQs

How much interest does $500,000 earn a year?

You’ll earn different amounts of interest depending on what you do with this money. If it’s in a savings account, you might get as little as 0.05%. In the stock market, anything is theoretically possible. Ask a financial advisor to provide advice about your overall portfolio performance.

Can you live off the interest of one million dollars?

If you’ve invested well, then yes, you can live off the interest income from one million dollars. It is very reasonable to expect 3% interest on your investments, and many investors — even non-professionals — are able to achieve that level of income. It’s possible an excellent online savings account may even offer that return.

Can I retire at 55 with $500k?

Generally speaking, it would not be advisable to retire at 55 with only $500,000 in the bank. An investment account that performs well in excellent times may make it feasible for a period of time, but any dip in account performance will likely take a serious toll on your financial independence.

Key Takeaways

- It is very possible to live off of interest if you invest wisely and start with a large enough principal.

- Concentrate on accumulating a sufficient base of capital with enough time to mature.

- Your investments will need to produce reliable returns at a rate that matches your principal investment to your retirement goals.

- There are many factors, such as inflation and taxes to consider before comfortably retiring.

- Like all investments, it’s important to plan how they will continue to produce steady income over time as market conditions change even after you retire.

Share this post: