When Looking For Pre-approval on a car loan you should not…

Last updated 12/08/2025 by

Benjamin Locke

Fact checked by

Andrew Latham

Summary:

Getting pre-approved for a car loan is an essential step for many buyers, but mistakes during the process can lead to higher costs or missed opportunities. This article outlines what to avoid when seeking pre-approval and provides actionable tips to secure the best loan terms while making informed financial decisions.

Sometimes you should avoid doing things. When you are eating dinner, you should avoid putting your feet on the table. When it comes to car loan pre-approvals, that´s a whole other kettle of fish.

Get Competing Auto Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Why Getting Preapproved Matters

Getting preapproved for an auto loan helps you understand your budget, compare multiple lenders, and walk into the dealership with more negotiating power. It’s one of the smartest steps you can take before shopping for a car.

- Know your rate before you shop — prevents dealer markups.

- Understand your true budget — avoids overspending on monthly payments.

- Compare lenders fairly — find the lowest APR for your situation.

- Negotiate like a cash buyer — improves leverage at the dealership.

Friendly Tip: Aim to get preapproved with at least two or three lenders before visiting a dealership. It protects your wallet and helps you spot inflated APR offers.

Common mistakes to avoid when seeking pre-approval

When looking for pre-approval on a car loan, you should not overlook the potential pitfalls that can derail your financial plans. Pre-approval is a powerful tool that can simplify the car-buying process and secure better loan terms, but common mistakes can lead to higher costs, added stress, and missed opportunities.

From failing to compare lenders to focusing solely on monthly payments, understanding what to avoid is just as important as knowing what to do. By identifying these common missteps, you’ll be better equipped to make informed decisions and confidently navigate the pre-approval process.

1. Not shopping around for the best interest rates

Accepting the first loan offer might seem convenient, but it can lead to significantly higher costs over the life of the loan. Interest rates vary across banks, credit unions, and online lenders, so it’s essential to compare options.

2. Skipping pre-approval before visiting dealerships

Walking into a dealership without pre-approval puts you at a disadvantage. Dealers often push financing through their preferred lenders, which may not offer competitive rates. Pre-approval ensures you’re not relying solely on dealership financing, giving you more bargaining power.

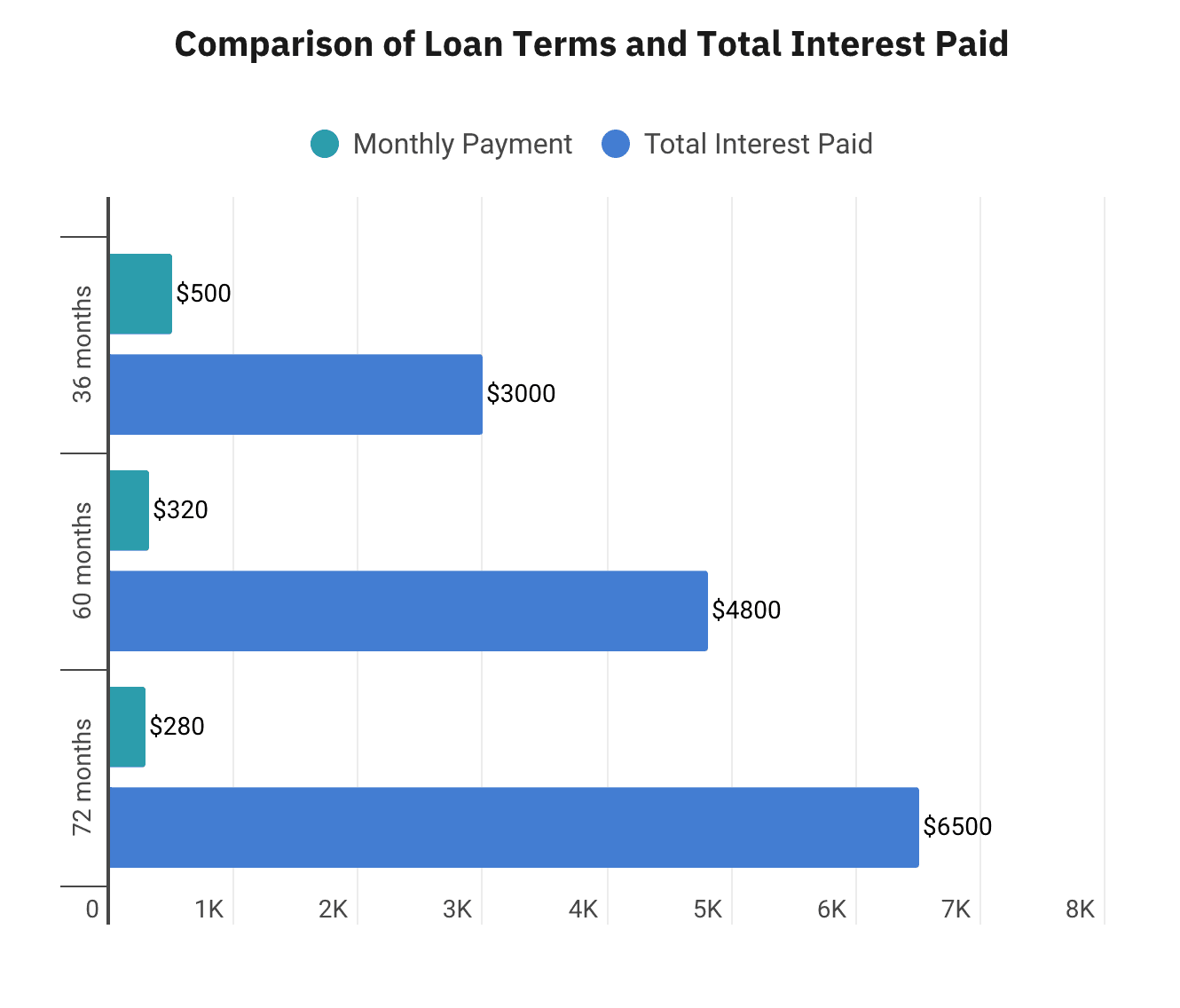

3. Focusing only on monthly payments

A common tactic used by dealerships is to present lower monthly payments by extending the loan term. While this may seem appealing, it often results in paying significantly more in interest. Focus on the total cost of the loan, not just the monthly payment, to ensure you’re making a sound financial decision.

4. Confusing pre-qualification with pre-approval

Pre-qualification and pre-approval are not the same. Pre-qualification provides an estimate based on self-reported information, while pre-approval involves a hard credit check and offers firm loan details. Relying on pre-qualification alone can lead to unrealistic expectations.

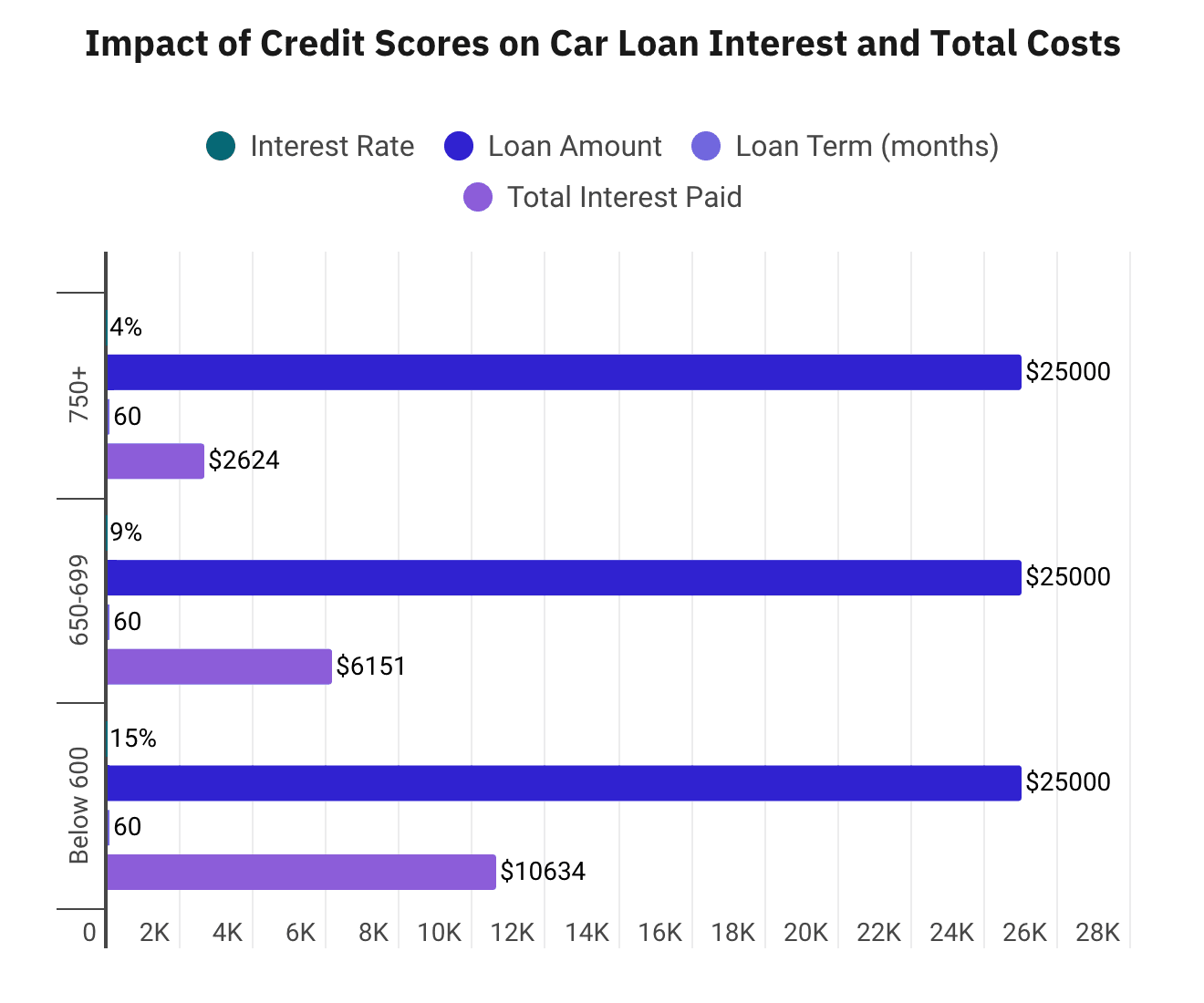

5. Neglecting your credit report

Your credit score plays a crucial role in determining the interest rate you qualify for on a car loan. A higher credit score can save you thousands in interest over the life of the loan, while a lower score may lead to significantly higher costs. Here are three scenarios that highlight the financial impact of different credit scores, demonstrating why even small improvements in your score can make a big difference.

Scenario 1: High Credit Score (750+)

A buyer with an excellent credit score of 750 or higher secures a competitive 4% interest rate on a $25,000 loan over 60 months. Thanks to their strong credit, they only pay $2,624 in total interest, keeping their overall costs low and manageable.

Scenario 2: Average Credit Score (650-699)

A buyer with an average credit score of 650-699 faces a higher interest rate of 9% on the same $25,000 loan over 60 months. This results in $6,151 in total interest, nearly triple the cost compared to someone with excellent credit.

Scenario 3: Low Credit Score (Below 600)

A buyer with a poor credit score below 600 qualifies for a steep 15% interest rate. On a $25,000 loan over 60 months, they pay $10,634 in total interest, making the car far more expensive in the long run.

6. Ignoring the loan agreement fine print

Hidden fees, prepayment penalties, and restrictive clauses are often buried in loan agreements, and failing to read the terms thoroughly can result in unexpected costs. Common hidden fees include loan origination fees, prepayment penalties, and gap insurance requirements. To avoid surprises, it’s essential to ask your lender for a detailed breakdown of all fees and charges before signing the agreement.

7. Overextending your budget

While pre-approval gives you a borrowing limit, it doesn’t mean you should spend the maximum amount. Consider your other financial obligations, such as insurance, maintenance, and fuel costs, when determining your car-buying budget.

What Lenders Look For During Preapproval

Before issuing a preapproval, lenders evaluate several factors to determine how much you can borrow and what interest rate you qualify for.

- Credit score: The biggest factor in determining your APR.

- Income stability: Lenders want to see consistent monthly income.

- Debt-to-income ratio: A lower DTI means you have room in your budget.

- Loan term: Shorter terms often qualify for lower rates.

- Down payment: A higher down payment reduces lender risk and can unlock better rates.

Good to Know: If your credit score is close to the next “tier,” improving it before applying can significantly reduce your APR.

Where to Get Preapproved for a Car Loan

Not all lenders treat preapprovals the same way. Here’s how banks, credit unions, and online lenders compare:

| Lender Type | Pros | Cons |

|---|---|---|

| Banks | Competitive rates, established institutions, strong borrower protections | Stricter requirements, slower approvals |

| Credit Unions | Often the lowest rates, member-friendly terms | Membership required |

| Online Lenders | Fast approvals, rate shopping tools, flexible terms | Rates vary widely across platforms |

Pro Tip: Always get at least one outside preapproval before going to a dealership — it helps you spot inflated dealer APRs and negotiate confidently.

Why pre-approval matters for car loans

Pre-approval for a car loan is more than a formality—it’s a tool to help you shop smarter, negotiate better, and avoid overextending your finances. By securing pre-approval, you can determine how much you can borrow and what interest rate you qualify for, giving you a clear picture of your car-buying budget.

Benefits of pre-approval

Pre-approval offers numerous advantages that can simplify the car-buying process and save you money. By securing pre-approval, you gain clarity on your budget, improve your negotiating power, and avoid surprises when finalizing your loan. Understanding these benefits can help you make smarter financial decisions.

Pre-approval provides several advantages

- Budget clarity: Knowing your borrowing limit helps you focus on cars within your price range.

- Better negotiation: Dealers often take pre-approved buyers more seriously, making it easier to negotiate on price.

- Lower interest rates: Pre-approval allows you to compare multiple lenders and secure competitive rates.

- Avoiding surprises: You’ll know your loan terms upfront, preventing last-minute issues during the purchase.

However, navigating the pre-approval process can be tricky, and mistakes at this stage may cost you time, money, and peace of mind. Let’s explore what to avoid when seeking pre-approval for a car loan.

How to avoid these mistakes

Avoiding common mistakes during the pre-approval process can save you time, money, and stress. By taking a proactive approach and following these key steps, you can secure the best loan terms and make confident financial decisions. Here’s how to ensure a smooth and successful pre-approval experience.

To ensure a smooth pre-approval process:

- Compare interest rates from multiple lenders to secure the best deal.

- Review your credit report and address any errors before applying.

- Get pre-approved before visiting dealerships to strengthen your negotiating position.

- Focus on the total loan cost, not just monthly payments.

- Thoroughly read and understand the loan agreement before signing.

- Set a realistic budget that accounts for additional car-related expenses.

Hard Inquiries vs. Soft Inquiries

A soft inquiry happens when a lender checks your credit for prequalification or preapproval — it does not affect your score.

A hard inquiry occurs when you officially apply for a loan, and it may temporarily lower your credit score by a few points.

Rate shopping for auto loans within a short window is typically treated as one hard inquiry.

A soft inquiry happens when a lender checks your credit for prequalification or preapproval — it does not affect your score.

A hard inquiry occurs when you officially apply for a loan, and it may temporarily lower your credit score by a few points.

Rate shopping for auto loans within a short window is typically treated as one hard inquiry.

The process of pre-approval for a car loan

Understanding the steps involved in the pre-approval process can make it smoother and more efficient. Here’s a breakdown of what to expect:

Check your credit score

Before applying, review your credit report to ensure it’s accurate. A higher credit score can qualify you for better interest rates. Correct any errors and, if possible, take steps to improve your score.

Determine your budget

Assess your income and expenses to decide how much you can comfortably spend on monthly car payments. Don’t forget to include additional costs such as insurance, maintenance, and fuel.

Real-Life Scenarios for Car Loan Pre-Approval

Below are two real-life scenarios with narratives and calculations. These examples can help visualize how different loan terms and monthly payment budgets affect the total loan amount and overall costs.

Scenario 1: John’s Budget-Friendly Plan

John is a recent college graduate looking to buy a reliable used car. He has a strict monthly budget of $350 for car payments and prefers to pay off the loan within 60 months. The interest rate offered to him is 6%.

| Loan Detail | Value |

|---|---|

| Monthly Payment | $350 |

| Loan Term | 60 months (5 years) |

| Interest Rate | 6% |

| Total Loan Amount | $18,870 |

| Total Interest Paid | $3,870 |

Calculation: Using the formula for calculating loan amounts with interest:

John can borrow up to $18,870 with his budget. He must also account for taxes, fees, and insurance separately.

Scenario 2: Emily’s Accelerated Payoff

Emily is a working professional who wants to minimize her total interest payments. She can afford $600 per month and aims to pay off her loan within 36 months. Her interest rate is slightly better at 4.5%.

| Loan Detail | Value |

|---|---|

| Monthly Payment | $600 |

| Loan Term | 36 months (3 years) |

| Interest Rate | 4.5% |

| Total Loan Amount | $20,282 |

| Total Interest Paid | $2,282 |

Calculation: Using the same formula, where:

Emily can borrow up to $20,282 while minimizing the total interest paid due to the shorter loan term.

Gather necessary documents

Lenders typically require the following documentation to process your pre-approval application:

| Required Documentation | Description |

|---|---|

| Proof of identity | Driver’s license or passport |

| Proof of income | Recent pay stubs or tax returns |

| Proof of residency | Utility bills or lease agreement |

| Employment verification | Verification of current employment status |

| Details of debts | Information about other financial obligations |

Shop around for lenders

When exploring loan options, consider various sources such as banks, credit unions, online lenders, and dealership financing departments. Each option offers unique benefits, so it’s essential to compare interest rates, loan terms, and fees to determine which best fits your financial needs and goals.

Submit your application

Complete the application with your chosen lender. Be prepared for a hard credit inquiry, which may cause a slight dip in your credit score. The lender will evaluate your creditworthiness and provide a decision.

Pro Tip

Submitting applications to multiple lenders within a short period (usually 14-45 days, depending on the credit scoring model) counts as a single inquiry, minimizing the impact on your score.

Review your loan terms

Once approved, the lender will provide your loan terms, including:

| Loan Term Details | Description |

|---|---|

| Approved loan amount | The total amount of money the lender agrees to lend you. |

| Interest rate | The percentage rate charged on the loan impacts overall cost. |

| Loan term | The duration of the loan is typically expressed in months or years. |

| Estimated monthly payments | The projected amount you will pay each month toward the loan. |

How to Get a Strong Preapproval

- Check your credit score first so you know what to expect.

- Gather documents early — pay stubs, income info, and ID.

- Compare offers from at least two lenders before choosing.

- Avoid unnecessary hard inquiries outside the rate-shopping window.

- Decide on your budget before visiting a dealership.

A solid preapproval positions you as an informed buyer and can save you thousands over the life of your auto loan.

What’s Next

Once you’re comfortable with the preapproval process, the next step is to compare lender options and find the most competitive auto loan offer.

Smart Move: Compare personalized offers on our Best Auto Loans page to find the lender with the lowest APR and most flexible terms for your budget.

Related Auto Loan Articles

- How Do Car Loans Work? – Understand the full path from application to payoff.

- What Is an Auto Loan? – A beginner-friendly guide to how car financing actually works.

- What Is a Good APR for a Car Loan? – Learn how to compare rates and identify a competitive offer.

- Personal Loan vs. Auto Loan – Compare borrowing options and choose the right one for your budget.

- Paying Cash vs. Auto Loan – See which approach saves more depending on your financial situation.

FAQ

Can I get pre-approved for a car loan with no credit history?

Yes, some lenders specialize in working with individuals with no credit history, but the terms may include higher interest rates or require a co-signer. Establishing a credit history or improving your credit score can help you secure better loan terms.

What happens if my pre-approval expires?

If your pre-approval expires, you’ll need to reapply with your lender. This may involve a new credit inquiry and updated financial documentation to ensure your situation hasn’t changed.

Does pre-approval lock in my interest rate?

Pre-approval typically locks in your interest rate for the validity period (30-60 days). However, rate locks may vary by lender, so it’s important to confirm this detail during the pre-approval process.

Can I use pre-approval for a used car purchase?

Yes, pre-approval can be used for both new and used car purchases. However, some lenders may have specific requirements or restrictions on the age and mileage of used vehicles they finance.

Is pre-approval available for private seller transactions?

Yes, many lenders offer pre-approval for private seller purchases. You’ll need to provide additional documentation, such as the vehicle’s title and inspection report, to complete the loan process.

Key takeaways

- Pre-approval simplifies the car-buying process by providing a clear understanding of your budget and loan terms.

- Shopping around for lenders can help you secure better interest rates and avoid costly mistakes.

- Avoiding pitfalls like skipping pre-approval or focusing solely on monthly payments ensures smarter financial decisions.

- Understanding the impact of credit scores can save you thousands in interest over the life of the loan.

Share this post:

AddTable of Contents