670 Credit Score: Good Or Bad? And What Can I Get With A 670 Credit Score?

AL

Summary:

A 670 credit is considered a "Good" credit score. Having a "Good" credit score, specifically within the 670 to 739 range, signifies that you've been generally responsible in managing your financial obligations. This category, though not the highest, still opens up a variety of opportunities in terms of credit and loan approval.

Although a 670 credit score may not garner the most preferential interest rates and terms, it indicates a satisfactory creditworthiness that most lenders find appealing. Let's see what terms, loans, and rates you can expect to get with a 670 credit score. Remember that every bit of improvement matters, paving the way to better financial opportunities.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How is Your Credit Score of 670 Determined?

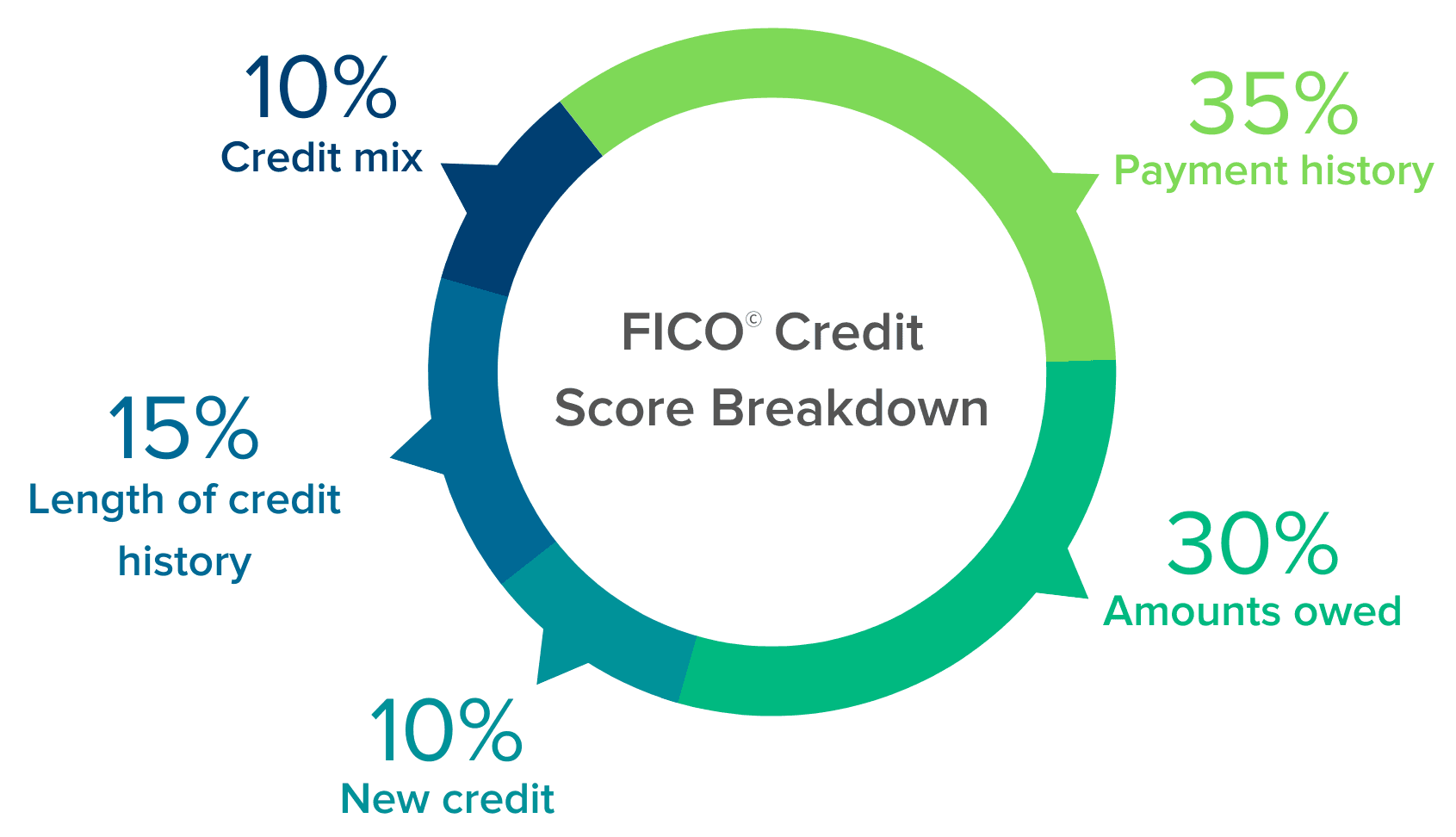

Before we delve into the significance of your 670 credit score, let's explore how credit scores are calculated. Your credit score is composed of different factors, each playing a distinct role in the overall score.

- Payment history. The most significant factor affecting your credit score is your payment history, which is simply a record of your bill and credit payments. This history tracks your on-time and late payments, whether they are loan repayments, credit card payments, utility bills, or other services.

- Amounts owed. This reflects your available credit compared to the amount of credit you owe. This is also known as your credit utilization ratio, which ideally should be kept below 30%. High credit utilization, such as maxing out your credit cards, can negatively impact your score.

- Length of credit history. The duration you've maintained a credit account is also important, even if you're not actively using that line of credit. This factor takes into account the age of your oldest and newest credit accounts and the average age of all your accounts.

- Credit mix. Contrary to what you might think, having a variety of credit accounts can be beneficial. A mix of credit cards, an auto loan, and a mortgage shows lenders your capability to manage different types of credit responsibly.

- New credit. The term "new" credit refers to the number of credit accounts you've recently opened and the number of inquiries made into your account. Each time you apply for a new loan or credit line, the lender makes an inquiry into your credit history to review your score and payment history.

Pro Tip

Remember, the categories mentioned above aren't exclusive to FICO credit scores. Other models, including VantageScore and PLUS, also consider these factors. While PLUS scores aren't often looked at by lenders, VantageScore is widely used. Therefore, when reviewing your credit score and history, ensure to check all your credit scores.

What Does Your Credit Score of 670 Imply?

A credit score of 670 is about average. While only a modest fraction of Americans (about a third) have scores below 669, Experian found that borrowers in this range were much more likely to become "seriously delinquent," or more than 90 days late on a payment. This tendency explains why lenders may be cautious when dealing with an applicant boasting a 670 credit score.| Credit score range | % of consumers | Delinquency rate |

|---|---|---|

| 300-579 | 16% | 61% |

| 580-669 | 17% | 28% |

| 670-739 | 21% | 8% |

| 740-799 | 25% | 2% |

| 800-850 | 21% | 1% |

How Does Your 670 Credit Score Stack Up?

Sadly, a 670 credit score is not considered impressive. You may struggle to get low interest rates on an auto loan or to obtain a high credit limit. As the data below indicates, the average credit score is continually rising.The table below links to in-depth articles for all credit scores.

| Credit score | Scale |

|---|---|

| 300 | Poor |

| 301 | Poor |

| 302 | Poor |

| 303 | Poor |

| 304 | Poor |

| 305 | Poor |

| 306 | Poor |

| 307 | Poor |

| 308 | Poor |

| 309 | Poor |

| 310 | Poor |

| 311 | Poor |

| 312 | Poor |

| 313 | Poor |

| 314 | Poor |

| 315 | Poor |

| 316 | Poor |

| 317 | Poor |

| 318 | Poor |

| 319 | Poor |

| 320 | Poor |

| 321 | Poor |

| 322 | Poor |

| 323 | Poor |

| 324 | Poor |

| 325 | Poor |

| 326 | Poor |

| 327 | Poor |

| 328 | Poor |

| 329 | Poor |

| 330 | Poor |

| 331 | Poor |

| 332 | Poor |

| 333 | Poor |

| 334 | Poor |

| 335 | Poor |

| 336 | Poor |

| 337 | Poor |

| 338 | Poor |

| 339 | Poor |

| 340 | Poor |

| 341 | Poor |

| 342 | Poor |

| 343 | Poor |

| 344 | Poor |

| 345 | Poor |

| 346 | Poor |

| 347 | Poor |

| 348 | Poor |

| 349 | Poor |

| 350 | Poor |

| 351 | Poor |

| 352 | Poor |

| 353 | Poor |

| 354 | Poor |

| 355 | Poor |

| 356 | Poor |

| 357 | Poor |

| 358 | Poor |

| 359 | Poor |

| 360 | Poor |

| 361 | Poor |

| 362 | Poor |

| 363 | Poor |

| 364 | Poor |

| 365 | Poor |

| 366 | Poor |

| 367 | Poor |

| 368 | Poor |

| 369 | Poor |

| 370 | Poor |

| 371 | Poor |

| 372 | Poor |

| 373 | Poor |

| 374 | Poor |

| 375 | Poor |

| 376 | Poor |

| 377 | Poor |

| 378 | Poor |

| 379 | Poor |

| 380 | Poor |

| 381 | Poor |

| 382 | Poor |

| 383 | Poor |

| 384 | Poor |

| 385 | Poor |

| 386 | Poor |

| 387 | Poor |

| 388 | Poor |

| 389 | Poor |

| 390 | Poor |

| 391 | Poor |

| 392 | Poor |

| 393 | Poor |

| 394 | Poor |

| 395 | Poor |

| 396 | Poor |

| 397 | Poor |

| 398 | Poor |

| 399 | Poor |

| 400 | Poor |

| 401 | Poor |

| 402 | Poor |

| 403 | Poor |

| 404 | Poor |

| 405 | Poor |

| 406 | Poor |

| 407 | Poor |

| 408 | Poor |

| 409 | Poor |

| 410 | Poor |

| 411 | Poor |

| 412 | Poor |

| 413 | Poor |

| 414 | Poor |

| 415 | Poor |

| 416 | Poor |

| 417 | Poor |

| 418 | Poor |

| 419 | Poor |

| 420 | Poor |

| 421 | Poor |

| 422 | Poor |

| 423 | Poor |

| 424 | Poor |

| 425 | Poor |

| 426 | Poor |

| 427 | Poor |

| 428 | Poor |

| 429 | Poor |

| 430 | Poor |

| 431 | Poor |

| 432 | Poor |

| 433 | Poor |

| 434 | Poor |

| 435 | Poor |

| 436 | Poor |

| 437 | Poor |

| 438 | Poor |

| 439 | Poor |

| 440 | Poor |

| 441 | Poor |

| 442 | Poor |

| 443 | Poor |

| 444 | Poor |

| 445 | Poor |

| 446 | Poor |

| 447 | Poor |

| 448 | Poor |

| 449 | Poor |

| 450 | Poor |

| 451 | Poor |

| 452 | Poor |

| 453 | Poor |

| 454 | Poor |

| 455 | Poor |

| 456 | Poor |

| 457 | Poor |

| 458 | Poor |

| 459 | Poor |

| 460 | Poor |

| 461 | Poor |

| 462 | Poor |

| 463 | Poor |

| 464 | Poor |

| 465 | Poor |

| 466 | Poor |

| 467 | Poor |

| 468 | Poor |

| 469 | Poor |

| 470 | Poor |

| 471 | Poor |

| 472 | Poor |

| 473 | Poor |

| 474 | Poor |

| 475 | Poor |

| 476 | Poor |

| 477 | Poor |

| 478 | Poor |

| 479 | Poor |

| 480 | Poor |

| 481 | Poor |

| 482 | Poor |

| 483 | Poor |

| 484 | Poor |

| 485 | Poor |

| 486 | Poor |

| 487 | Poor |

| 488 | Poor |

| 489 | Poor |

| 490 | Poor |

| 491 | Poor |

| 492 | Poor |

| 493 | Poor |

| 494 | Poor |

| 495 | Poor |

| 496 | Poor |

| 497 | Poor |

| 498 | Poor |

| 499 | Poor |

| 500 | Poor |

| 501 | Poor |

| 502 | Poor |

| 503 | Poor |

| 504 | Poor |

| 505 | Poor |

| 506 | Poor |

| 507 | Poor |

| 508 | Poor |

| 509 | Poor |

| 510 | Poor |

| 511 | Poor |

| 512 | Poor |

| 513 | Poor |

| 514 | Poor |

| 515 | Poor |

| 516 | Poor |

| 517 | Poor |

| 518 | Poor |

| 519 | Poor |

| 520 | Poor |

| 521 | Poor |

| 522 | Poor |

| 523 | Poor |

| 524 | Poor |

| 525 | Poor |

| 526 | Poor |

| 527 | Poor |

| 528 | Poor |

| 529 | Poor |

| 530 | Poor |

| 531 | Poor |

| 532 | Poor |

| 533 | Poor |

| 534 | Poor |

| 535 | Poor |

| 536 | Poor |

| 537 | Poor |

| 538 | Poor |

| 539 | Poor |

| 540 | Poor |

| 541 | Poor |

| 542 | Poor |

| 543 | Poor |

| 544 | Poor |

| 545 | Poor |

| 546 | Poor |

| 547 | Poor |

| 548 | Poor |

| 549 | Poor |

| 550 | Poor |

| 551 | Poor |

| 552 | Poor |

| 553 | Poor |

| 554 | Poor |

| 555 | Poor |

| 556 | Poor |

| 557 | Poor |

| 558 | Poor |

| 559 | Poor |

| 560 | Poor |

| 561 | Poor |

| 562 | Poor |

| 563 | Poor |

| 564 | Poor |

| 565 | Poor |

| 566 | Poor |

| 567 | Poor |

| 568 | Poor |

| 569 | Poor |

| 570 | Poor |

| 571 | Poor |

| 572 | Poor |

| 573 | Poor |

| 574 | Poor |

| 575 | Poor |

| 576 | Poor |

| 577 | Poor |

| 578 | Poor |

| 579 | Poor |

| 580 | Fair |

| 581 | Fair |

| 582 | Fair |

| 583 | Fair |

| 584 | Fair |

| 585 | Fair |

| 586 | Fair |

| 587 | Fair |

| 588 | Fair |

| 589 | Fair |

| 590 | Fair |

| 591 | Fair |

| 592 | Fair |

| 593 | Fair |

| 594 | Fair |

| 595 | Fair |

| 596 | Fair |

| 597 | Fair |

| 598 | Fair |

| 599 | Fair |

| 600 | Fair |

| 601 | Fair |

| 602 | Fair |

| 603 | Fair |

| 604 | Fair |

| 605 | Fair |

| 606 | Fair |

| 607 | Fair |

| 608 | Fair |

| 609 | Fair |

| 610 | Fair |

| 611 | Fair |

| 612 | Fair |

| 613 | Fair |

| 614 | Fair |

| 615 | Fair |

| 616 | Fair |

| 617 | Fair |

| 618 | Fair |

| 619 | Fair |

| 620 | Fair |

| 621 | Fair |

| 622 | Fair |

| 623 | Fair |

| 624 | Fair |

| 625 | Fair |

| 626 | Fair |

| 627 | Fair |

| 628 | Fair |

| 629 | Fair |

| 630 | Fair |

| 631 | Fair |

| 632 | Fair |

| 633 | Fair |

| 634 | Fair |

| 635 | Fair |

| 636 | Fair |

| 637 | Fair |

| 638 | Fair |

| 639 | Fair |

| 640 | Fair |

| 641 | Fair |

| 642 | Fair |

| 643 | Fair |

| 644 | Fair |

| 645 | Fair |

| 646 | Fair |

| 647 | Fair |

| 648 | Fair |

| 649 | Fair |

| 650 | Fair |

| 651 | Fair |

| 652 | Fair |

| 653 | Fair |

| 654 | Fair |

| 655 | Fair |

| 656 | Fair |

| 657 | Fair |

| 658 | Fair |

| 659 | Fair |

| 660 | Fair |

| 661 | Fair |

| 662 | Fair |

| 663 | Fair |

| 664 | Fair |

| 665 | Fair |

| 666 | Fair |

| 667 | Fair |

| 668 | Fair |

| 669 | Fair |

| 670 | Good |

| 671 | Good |

| 672 | Good |

| 673 | Good |

| 674 | Good |

| 675 | Good |

| 676 | Good |

| 677 | Good |

| 678 | Good |

| 679 | Good |

| 680 | Good |

| 681 | Good |

| 682 | Good |

| 683 | Good |

| 684 | Good |

| 685 | Good |

| 686 | Good |

| 687 | Good |

| 688 | Good |

| 689 | Good |

| 690 | Good |

| 691 | Good |

| 692 | Good |

| 693 | Good |

| 694 | Good |

| 695 | Good |

| 696 | Good |

| 697 | Good |

| 698 | Good |

| 699 | Good |

| 700 | Good |

| 701 | Good |

| 702 | Good |

| 703 | Good |

| 704 | Good |

| 705 | Good |

| 706 | Good |

| 707 | Good |

| 708 | Good |

| 709 | Good |

| 710 | Good |

| 711 | Good |

| 712 | Good |

| 713 | Good |

| 714 | Good |

| 715 | Good |

| 716 | Good |

| 717 | Good |

| 718 | Good |

| 719 | Good |

| 720 | Good |

| 721 | Good |

| 722 | Good |

| 723 | Good |

| 724 | Good |

| 725 | Good |

| 726 | Good |

| 727 | Good |

| 728 | Good |

| 729 | Good |

| 730 | Good |

| 731 | Good |

| 732 | Good |

| 733 | Good |

| 734 | Good |

| 735 | Good |

| 736 | Good |

| 737 | Good |

| 738 | Good |

| 739 | Good |

| 740 | Very Good |

| 741 | Very Good |

| 742 | Very Good |

| 743 | Very Good |

| 744 | Very Good |

| 745 | Very Good |

| 746 | Very Good |

| 747 | Very Good |

| 748 | Very Good |

| 749 | Very Good |

| 750 | Very Good |

| 751 | Very Good |

| 752 | Very Good |

| 753 | Very Good |

| 754 | Very Good |

| 755 | Very Good |

| 756 | Very Good |

| 757 | Very Good |

| 758 | Very Good |

| 759 | Very Good |

| 760 | Very Good |

| 761 | Very Good |

| 762 | Very Good |

| 763 | Very Good |

| 764 | Very Good |

| 765 | Very Good |

| 766 | Very Good |

| 767 | Very Good |

| 768 | Very Good |

| 769 | Very Good |

| 770 | Very Good |

| 771 | Very Good |

| 772 | Very Good |

| 773 | Very Good |

| 774 | Very Good |

| 775 | Very Good |

| 776 | Very Good |

| 777 | Very Good |

| 778 | Very Good |

| 779 | Very Good |

| 780 | Very Good |

| 781 | Very Good |

| 782 | Very Good |

| 783 | Very Good |

| 784 | Very Good |

| 785 | Very Good |

| 786 | Very Good |

| 787 | Very Good |

| 788 | Very Good |

| 789 | Very Good |

| 790 | Very Good |

| 791 | Very Good |

| 792 | Very Good |

| 793 | Very Good |

| 794 | Very Good |

| 795 | Very Good |

| 796 | Very Good |

| 797 | Very Good |

| 798 | Very Good |

| 799 | Very Good |

| 800 | Excellent |

| 801 | Excellent |

| 802 | Excellent |

| 803 | Excellent |

| 804 | Excellent |

| 805 | Excellent |

| 806 | Excellent |

| 807 | Excellent |

| 808 | Excellent |

| 809 | Excellent |

| 810 | Excellent |

| 811 | Excellent |

| 812 | Excellent |

| 813 | Excellent |

| 814 | Excellent |

| 815 | Excellent |

| 816 | Excellent |

| 817 | Excellent |

| 818 | Excellent |

| 819 | Excellent |

| 820 | Excellent |

| 821 | Excellent |

| 822 | Excellent |

| 823 | Excellent |

| 824 | Excellent |

| 825 | Excellent |

| 826 | Excellent |

| 827 | Excellent |

| 828 | Excellent |

| 829 | Excellent |

| 830 | Excellent |

| 831 | Excellent |

| 832 | Excellent |

| 833 | Excellent |

| 834 | Excellent |

| 835 | Excellent |

| 836 | Excellent |

| 837 | Excellent |

| 838 | Excellent |

| 839 | Excellent |

| 840 | Excellent |

| 841 | Excellent |

| 842 | Excellent |

| 843 | Excellent |

| 844 | Excellent |

| 845 | Excellent |

| 846 | Excellent |

| 847 | Excellent |

| 848 | Excellent |

| 849 | Excellent |

| 850 | Excellent |

What Can You Get with a 670 Credit Score?

A 670 credit score falls into the "Good" category, which means you have plenty of options:| Type of Credit | Eligibility |

|---|---|

| Secured Credit Card | Yes |

| Unsecured Credit Card | Yes |

| Best Rewards Credit Card | No |

| 0% APR Credit Card | Maybe |

| Personal Loan | Yes |

| Apartment Rental | Probably |

| Home Loan | Yes |

| Auto Loan | Yes |

IMPORTANT! Remember, the above information is not an absolute guarantee. You may get approval for an excellent rewards credit card, but chances are, you won't secure the most favorable conditions.

Common credit cards for a 670 credit score

There are numerous credit cards that you could apply for with a 670. Nonetheless, the best card for you hinges on your expenditure habits and financial objectives. With the comparison tool provided below, you can explore various credit cards designed for those with a 670. Alongside reviewing the APRs you're eligible for, ensure to familiarize yourself with the fees you may need to pay, including annual fees.Frequently chosen personal loans for a 670 credit score

Similar to credit cards, a 670 permits you to apply for a range of personal loans, including both secured and unsecured loans. However, to pinpoint the best personal loan for you, it's necessary to evaluate all your options.Auto loans with a 670 credit score

Fortunately, over half of all approved auto loans are made to applicants with FICO scores above 661, as per Experian. Although a score of 670 doesn't guarantee you an auto loan, you stand a good chance of being approved. Nevertheless, to ensure you secure the most favorable loan conditions, you may want to accumulate funds for a larger down payment or work on improving your credit score prior to applying for auto loans. As shown in the table below, a higher credit score can save you hundreds of dollars over the duration of the loan.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 720 - 850 | 6.511% | $237 | $1,386 |

| 690 - 719 | 7.744% | $243 | $1,661 |

| 660 - 689 | 9.573% | $252 | $2,076 |

| 620 - 659 | 10.739% | $257 | $2,345 |

| 590 - 619 | 15.055% | $279 | $3,372 |

| 500 - 589 | 16.484% | $286 | $3,723 |

| *Rates above for a $10,000 48-month used auto loan. |

Mortgages and home loans with a 670 credit score

Those with credit scores above 620 typically comprise a large percentage of successful mortgage applicants. Similarly to auto loans, enhancing your score can save you substantial amounts of money on a mortgage.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 760 - 850 | 6.129% | $304 | $59,416 |

| 700 - 759 | 6.351% | $311 | $62,014 |

| 680 - 699 | 6.528% | $317 | $64,104 |

| 660 - 679 | 6.742% | $324 | $66,652 |

| 640 - 659 | 7.172% | $338 | $71,841 |

| 620 - 639 | 7.718% | $357 | $78,556 |

| *Rates above for a $50,000 30-year fixed rate mortgage. |

Student loans with a 670 credit score

Fortunately, student loans are some of the most straightforward to obtain with a credit score of 670. As most students are still in the process of building credit, it's reasonable for student loans to have less rigorous credit prerequisites. Indeed, federal student loans typically don't require a minimum credit score. While private student loan lenders generally impose stricter requirements, a score of 670 should still allow you to secure the financing you need.Strategies to improve a 670 Credit Score

Even if your current score falls within the "Good" credit range, there's always room for improvement. Boosting your credit score can unlock better financial opportunities and offer you more favorable loan terms.Maintain Timely Debt Payments

Having a 670 indicates that you've likely established positive credit habits. To maintain and even improve your score, it's crucial to continue managing your debts effectively. This involves making all your debt payments on time. Even one missed payment could lead to a significant decrease in your score.

Remember, both FICO and VantageScore credit scoring models are designed to reward responsible financial behavior. With their latest versions (FICO® 9 and VantageScore 3.0 and 4.0), they've updated their scoring models to ignore collections that have been paid off, showing a zero balance. This means that if you manage to pay off or settle a collection and it's reported as a zero balance on your credit reports, these scores may see a significant increase.

Manage Your Credit Utilization

Credit utilization, which is the percentage of your available credit that you're using, is another key factor in determining your credit score. The lower your credit utilization ratio, the better for your credit score. It's often recommended to keep your credit utilization below 30% across all of your accounts, and to maintain this level consistently, not just right before applying for credit.

Regularly Review Your Credit Report

Errors on your credit report can negatively impact your credit score. By regularly reviewing your credit reports from all three credit bureaus (Experian, TransUnion, and Equifax), you can identify and dispute any inaccuracies that may be harming your score. You're entitled to a free credit report from each bureau every 12 months, which you can obtain via AnnualCreditReport.com.

FAQs

Can I get approved for credit with a 670 credit score?

Yes, a 670 credit score can help you get approved for various types of credit, such as credit cards, auto loans, personal loans, and even some home loans. However, the specific terms and interest rates you're offered will depend on the lender and other factors like your income and current debt levels.Is a 670 a good credit score for buying a house?

A 670 is generally considered a good credit score and may help you qualify for a home loan. However, factors like your debt-to-income ratio, employment history, and down payment size can also influence your ability to get approved for a mortgage.How much can I borrow with a 670 credit score?

The amount you can borrow doesn't solely depend on your credit score but also on your income, the type of loan, and the lender's policies. With a 670, you may qualify for larger loan amounts, but remember to borrow responsibly and only what you can afford to repay.What benefits does a 670 credit score offer?

A 670 credit score generally offers several benefits, such as potentially qualifying for lower interest rates on loans, easier approval for rentals, better car insurance rates, and access to better credit cards with more rewards.Is a 670 credit score rare?

Credit scores can range from 300 to 850. While a 670 is considered good, it's not necessarily rare. Many people have credit scores in this range.Why is it challenging to get a 670 credit score?

Achieving a 670 can be challenging because it requires consistently responsible credit behavior over a long period. This includes making all your payments on time, keeping your credit utilization low, and maintaining a healthy mix of credit accounts.How accurate are credit monitoring services like Credit Karma?

Credit monitoring services like Credit Karma provide a close approximation of your credit score and are useful for tracking changes and trends. However, lenders may use slightly different models or versions of credit scores when reviewing your creditworthiness.What is the highest credit score in America?

The highest possible credit score according to the FICO and VantageScore models is 850. However, achieving this score is rare, as it requires an exceptional level of credit management over a long period.Key Takeaways

- With a 670 credit score, you're in the "Good" credit range by FICO standards, and a fair number of Americans find themselves in this bracket.

- Your payment history holds a big chunk of influence when your credit score is calculated.

- If you're eyeing a higher score, consider knocking down some of your current debts, take a close look at your credit report for any mistakes, or think about getting a secured card or personal loan.

- Even though a 670 credit score is decent, securing a mortgage or car loan might not always be possible and you won't qualify for preferential terms and rates.

- Remember, boosting your credit score is more of a marathon than a sprint. It might take a bit to push your 670 up to the "Very Good" (+740) or "Excellent" (+800) ranges.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: