Is a 810 Credit Score Good Or Bad? + Your Loan & Credit Card Options

AL

Summary:

A credit score of 810 falls in the "Excellent" range (800 to 850) and signifies an impressive record of financial responsibility. With a 810 credit score, you can expect to enjoy access to a broad range of credit products and the best available terms. However, bear in mind that though an excellent score increases your chances, credit approval is not a sure thing and depends on various other factors such as your income, existing debts, and more.

With an "Excellent" credit score, you are already at the pinnacle of credit ratings. Your primary focus should be on maintaining this top-tier credit score to continue enjoying the best interest rates and terms. But how do you ensure your credit score remains at the top? While there's no secret formula, there are several proven strategies that can help you maintain your excellent credit score. Continue reading to understand more about the components of a credit score, what a 810 score indicates for your financing options, and how you can keep your score at its current high level.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How is Your Credit Score of 810 Determined?

Before we dive into what your 810 credit score means, let's first understand how credit scores are determined. Your credit score is based on various factors, each with its own importance in the total score.

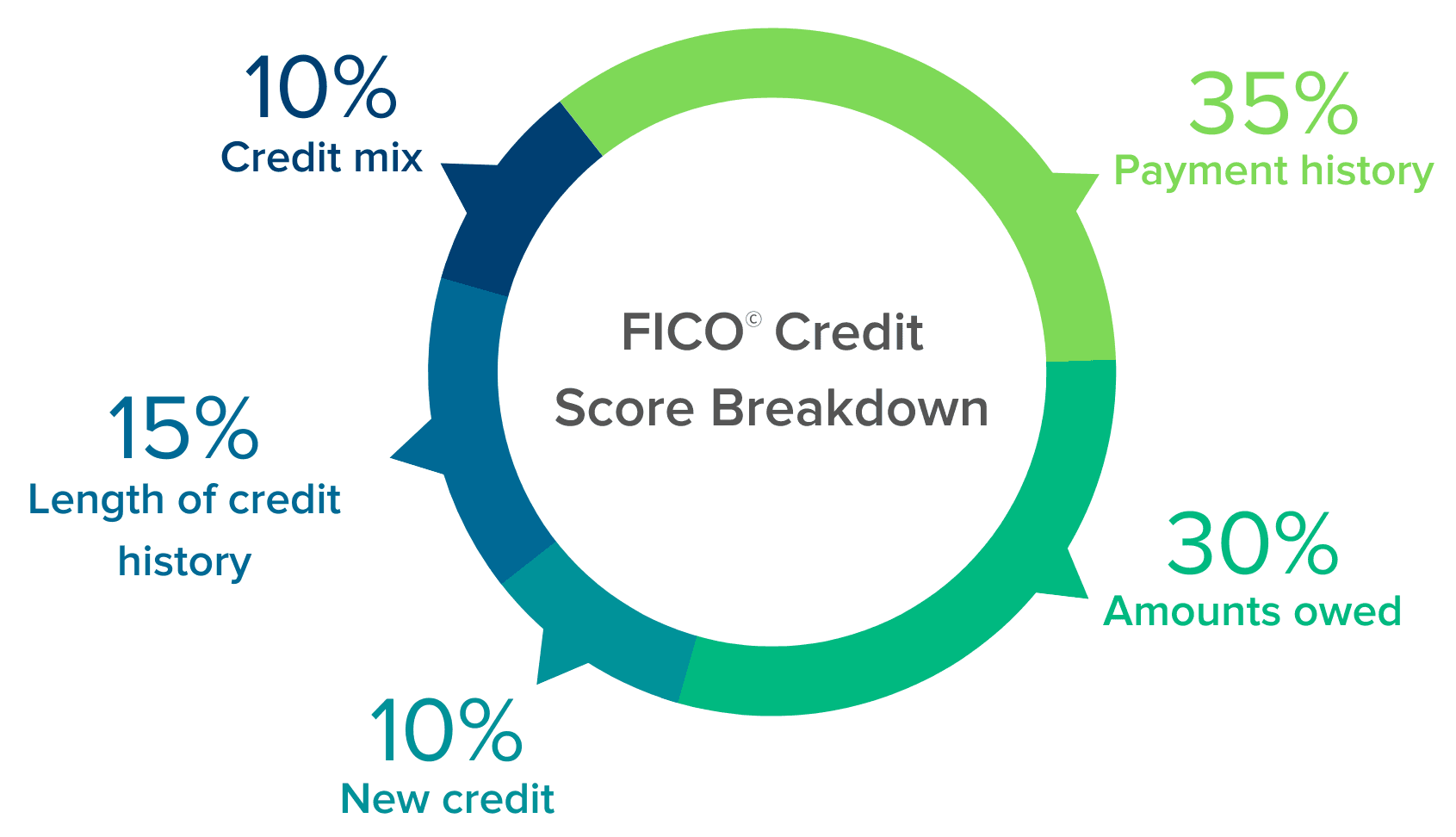

- Payment history. Your payment history, or the record of your bill and credit payments, is the most significant factor affecting your credit score. This history documents your on-time and late payments, whether they be loan repayments, credit card payments, utility bills, or other services.

- Amounts owed. This factor looks at your available credit in comparison to the amount of credit you owe, also known as your credit utilization ratio. Ideally, this should be below 30%. High credit utilization, such as maxing out your credit cards, can negatively impact your score.

- Length of credit history. The length of time you've maintained a credit account matters, even if you're not actively using that line of credit. This factor considers the age of your oldest and newest credit accounts and the average age of all your accounts.

- Credit mix. Having a variety of credit accounts can be beneficial. A mix of credit cards, an auto loan, and a mortgage shows lenders your ability to manage different types of credit responsibly.

- New credit. "New" credit refers to the number of credit accounts you've recently opened and the number of inquiries made into your account. Each time you apply for a new loan or credit line, the lender checks your credit history to review your score and payment history.

Pro Tip

Keep in mind that these categories aren't unique to FICO credit scores. Other models, such as VantageScore and PLUS, also consider these factors. While PLUS scores aren't often looked at by lenders, VantageScore is widely used. So when you review your credit score and history, make sure to check all your credit scores.

What Does Your Credit Score of 810 Imply?

A credit score of 810 is considered excellent. This score means you've demonstrated a long history of responsible credit management, timely payments, and a healthy credit mix. Lenders see you as a very low risk borrower, and you will often be offered the best terms and lowest interest rates. You are among the top tier of consumers for creditworthiness.| Credit score range | % of consumers | Delinquency rate |

|---|---|---|

| 300-579 | 16% | 61% |

| 580-669 | 17% | 28% |

| 670-739 | 21% | 8% |

| 740-799 | 25% | 2% |

| 800-850 | 21% | 1% |

How Does Your 810 Credit Score Compare?

A 810 credit score is considered top tier. You are among a small percentage of consumers who have managed their credit so responsibly. Your score significantly surpasses the average credit score, which continues to rise as consumers become more credit-savvy.The table below links to in-depth articles for all credit scores.

| Credit score | Scale |

|---|---|

| 300 | Poor |

| 301 | Poor |

| 302 | Poor |

| 303 | Poor |

| 304 | Poor |

| 305 | Poor |

| 306 | Poor |

| 307 | Poor |

| 308 | Poor |

| 309 | Poor |

| 310 | Poor |

| 311 | Poor |

| 312 | Poor |

| 313 | Poor |

| 314 | Poor |

| 315 | Poor |

| 316 | Poor |

| 317 | Poor |

| 318 | Poor |

| 319 | Poor |

| 320 | Poor |

| 321 | Poor |

| 322 | Poor |

| 323 | Poor |

| 324 | Poor |

| 325 | Poor |

| 326 | Poor |

| 327 | Poor |

| 328 | Poor |

| 329 | Poor |

| 330 | Poor |

| 331 | Poor |

| 332 | Poor |

| 333 | Poor |

| 334 | Poor |

| 335 | Poor |

| 336 | Poor |

| 337 | Poor |

| 338 | Poor |

| 339 | Poor |

| 340 | Poor |

| 341 | Poor |

| 342 | Poor |

| 343 | Poor |

| 344 | Poor |

| 345 | Poor |

| 346 | Poor |

| 347 | Poor |

| 348 | Poor |

| 349 | Poor |

| 350 | Poor |

| 351 | Poor |

| 352 | Poor |

| 353 | Poor |

| 354 | Poor |

| 355 | Poor |

| 356 | Poor |

| 357 | Poor |

| 358 | Poor |

| 359 | Poor |

| 360 | Poor |

| 361 | Poor |

| 362 | Poor |

| 363 | Poor |

| 364 | Poor |

| 365 | Poor |

| 366 | Poor |

| 367 | Poor |

| 368 | Poor |

| 369 | Poor |

| 370 | Poor |

| 371 | Poor |

| 372 | Poor |

| 373 | Poor |

| 374 | Poor |

| 375 | Poor |

| 376 | Poor |

| 377 | Poor |

| 378 | Poor |

| 379 | Poor |

| 380 | Poor |

| 381 | Poor |

| 382 | Poor |

| 383 | Poor |

| 384 | Poor |

| 385 | Poor |

| 386 | Poor |

| 387 | Poor |

| 388 | Poor |

| 389 | Poor |

| 390 | Poor |

| 391 | Poor |

| 392 | Poor |

| 393 | Poor |

| 394 | Poor |

| 395 | Poor |

| 396 | Poor |

| 397 | Poor |

| 398 | Poor |

| 399 | Poor |

| 400 | Poor |

| 401 | Poor |

| 402 | Poor |

| 403 | Poor |

| 404 | Poor |

| 405 | Poor |

| 406 | Poor |

| 407 | Poor |

| 408 | Poor |

| 409 | Poor |

| 410 | Poor |

| 411 | Poor |

| 412 | Poor |

| 413 | Poor |

| 414 | Poor |

| 415 | Poor |

| 416 | Poor |

| 417 | Poor |

| 418 | Poor |

| 419 | Poor |

| 420 | Poor |

| 421 | Poor |

| 422 | Poor |

| 423 | Poor |

| 424 | Poor |

| 425 | Poor |

| 426 | Poor |

| 427 | Poor |

| 428 | Poor |

| 429 | Poor |

| 430 | Poor |

| 431 | Poor |

| 432 | Poor |

| 433 | Poor |

| 434 | Poor |

| 435 | Poor |

| 436 | Poor |

| 437 | Poor |

| 438 | Poor |

| 439 | Poor |

| 440 | Poor |

| 441 | Poor |

| 442 | Poor |

| 443 | Poor |

| 444 | Poor |

| 445 | Poor |

| 446 | Poor |

| 447 | Poor |

| 448 | Poor |

| 449 | Poor |

| 450 | Poor |

| 451 | Poor |

| 452 | Poor |

| 453 | Poor |

| 454 | Poor |

| 455 | Poor |

| 456 | Poor |

| 457 | Poor |

| 458 | Poor |

| 459 | Poor |

| 460 | Poor |

| 461 | Poor |

| 462 | Poor |

| 463 | Poor |

| 464 | Poor |

| 465 | Poor |

| 466 | Poor |

| 467 | Poor |

| 468 | Poor |

| 469 | Poor |

| 470 | Poor |

| 471 | Poor |

| 472 | Poor |

| 473 | Poor |

| 474 | Poor |

| 475 | Poor |

| 476 | Poor |

| 477 | Poor |

| 478 | Poor |

| 479 | Poor |

| 480 | Poor |

| 481 | Poor |

| 482 | Poor |

| 483 | Poor |

| 484 | Poor |

| 485 | Poor |

| 486 | Poor |

| 487 | Poor |

| 488 | Poor |

| 489 | Poor |

| 490 | Poor |

| 491 | Poor |

| 492 | Poor |

| 493 | Poor |

| 494 | Poor |

| 495 | Poor |

| 496 | Poor |

| 497 | Poor |

| 498 | Poor |

| 499 | Poor |

| 500 | Poor |

| 501 | Poor |

| 502 | Poor |

| 503 | Poor |

| 504 | Poor |

| 505 | Poor |

| 506 | Poor |

| 507 | Poor |

| 508 | Poor |

| 509 | Poor |

| 510 | Poor |

| 511 | Poor |

| 512 | Poor |

| 513 | Poor |

| 514 | Poor |

| 515 | Poor |

| 516 | Poor |

| 517 | Poor |

| 518 | Poor |

| 519 | Poor |

| 520 | Poor |

| 521 | Poor |

| 522 | Poor |

| 523 | Poor |

| 524 | Poor |

| 525 | Poor |

| 526 | Poor |

| 527 | Poor |

| 528 | Poor |

| 529 | Poor |

| 530 | Poor |

| 531 | Poor |

| 532 | Poor |

| 533 | Poor |

| 534 | Poor |

| 535 | Poor |

| 536 | Poor |

| 537 | Poor |

| 538 | Poor |

| 539 | Poor |

| 540 | Poor |

| 541 | Poor |

| 542 | Poor |

| 543 | Poor |

| 544 | Poor |

| 545 | Poor |

| 546 | Poor |

| 547 | Poor |

| 548 | Poor |

| 549 | Poor |

| 550 | Poor |

| 551 | Poor |

| 552 | Poor |

| 553 | Poor |

| 554 | Poor |

| 555 | Poor |

| 556 | Poor |

| 557 | Poor |

| 558 | Poor |

| 559 | Poor |

| 560 | Poor |

| 561 | Poor |

| 562 | Poor |

| 563 | Poor |

| 564 | Poor |

| 565 | Poor |

| 566 | Poor |

| 567 | Poor |

| 568 | Poor |

| 569 | Poor |

| 570 | Poor |

| 571 | Poor |

| 572 | Poor |

| 573 | Poor |

| 574 | Poor |

| 575 | Poor |

| 576 | Poor |

| 577 | Poor |

| 578 | Poor |

| 579 | Poor |

| 580 | Fair |

| 581 | Fair |

| 582 | Fair |

| 583 | Fair |

| 584 | Fair |

| 585 | Fair |

| 586 | Fair |

| 587 | Fair |

| 588 | Fair |

| 589 | Fair |

| 590 | Fair |

| 591 | Fair |

| 592 | Fair |

| 593 | Fair |

| 594 | Fair |

| 595 | Fair |

| 596 | Fair |

| 597 | Fair |

| 598 | Fair |

| 599 | Fair |

| 600 | Fair |

| 601 | Fair |

| 602 | Fair |

| 603 | Fair |

| 604 | Fair |

| 605 | Fair |

| 606 | Fair |

| 607 | Fair |

| 608 | Fair |

| 609 | Fair |

| 610 | Fair |

| 611 | Fair |

| 612 | Fair |

| 613 | Fair |

| 614 | Fair |

| 615 | Fair |

| 616 | Fair |

| 617 | Fair |

| 618 | Fair |

| 619 | Fair |

| 620 | Fair |

| 621 | Fair |

| 622 | Fair |

| 623 | Fair |

| 624 | Fair |

| 625 | Fair |

| 626 | Fair |

| 627 | Fair |

| 628 | Fair |

| 629 | Fair |

| 630 | Fair |

| 631 | Fair |

| 632 | Fair |

| 633 | Fair |

| 634 | Fair |

| 635 | Fair |

| 636 | Fair |

| 637 | Fair |

| 638 | Fair |

| 639 | Fair |

| 640 | Fair |

| 641 | Fair |

| 642 | Fair |

| 643 | Fair |

| 644 | Fair |

| 645 | Fair |

| 646 | Fair |

| 647 | Fair |

| 648 | Fair |

| 649 | Fair |

| 650 | Fair |

| 651 | Fair |

| 652 | Fair |

| 653 | Fair |

| 654 | Fair |

| 655 | Fair |

| 656 | Fair |

| 657 | Fair |

| 658 | Fair |

| 659 | Fair |

| 660 | Fair |

| 661 | Fair |

| 662 | Fair |

| 663 | Fair |

| 664 | Fair |

| 665 | Fair |

| 666 | Fair |

| 667 | Fair |

| 668 | Fair |

| 669 | Fair |

| 670 | Good |

| 671 | Good |

| 672 | Good |

| 673 | Good |

| 674 | Good |

| 675 | Good |

| 676 | Good |

| 677 | Good |

| 678 | Good |

| 679 | Good |

| 680 | Good |

| 681 | Good |

| 682 | Good |

| 683 | Good |

| 684 | Good |

| 685 | Good |

| 686 | Good |

| 687 | Good |

| 688 | Good |

| 689 | Good |

| 690 | Good |

| 691 | Good |

| 692 | Good |

| 693 | Good |

| 694 | Good |

| 695 | Good |

| 696 | Good |

| 697 | Good |

| 698 | Good |

| 699 | Good |

| 700 | Good |

| 701 | Good |

| 702 | Good |

| 703 | Good |

| 704 | Good |

| 705 | Good |

| 706 | Good |

| 707 | Good |

| 708 | Good |

| 709 | Good |

| 710 | Good |

| 711 | Good |

| 712 | Good |

| 713 | Good |

| 714 | Good |

| 715 | Good |

| 716 | Good |

| 717 | Good |

| 718 | Good |

| 719 | Good |

| 720 | Good |

| 721 | Good |

| 722 | Good |

| 723 | Good |

| 724 | Good |

| 725 | Good |

| 726 | Good |

| 727 | Good |

| 728 | Good |

| 729 | Good |

| 730 | Good |

| 731 | Good |

| 732 | Good |

| 733 | Good |

| 734 | Good |

| 735 | Good |

| 736 | Good |

| 737 | Good |

| 738 | Good |

| 739 | Good |

| 740 | Very Good |

| 741 | Very Good |

| 742 | Very Good |

| 743 | Very Good |

| 744 | Very Good |

| 745 | Very Good |

| 746 | Very Good |

| 747 | Very Good |

| 748 | Very Good |

| 749 | Very Good |

| 750 | Very Good |

| 751 | Very Good |

| 752 | Very Good |

| 753 | Very Good |

| 754 | Very Good |

| 755 | Very Good |

| 756 | Very Good |

| 757 | Very Good |

| 758 | Very Good |

| 759 | Very Good |

| 760 | Very Good |

| 761 | Very Good |

| 762 | Very Good |

| 763 | Very Good |

| 764 | Very Good |

| 765 | Very Good |

| 766 | Very Good |

| 767 | Very Good |

| 768 | Very Good |

| 769 | Very Good |

| 770 | Very Good |

| 771 | Very Good |

| 772 | Very Good |

| 773 | Very Good |

| 774 | Very Good |

| 775 | Very Good |

| 776 | Very Good |

| 777 | Very Good |

| 778 | Very Good |

| 779 | Very Good |

| 780 | Very Good |

| 781 | Very Good |

| 782 | Very Good |

| 783 | Very Good |

| 784 | Very Good |

| 785 | Very Good |

| 786 | Very Good |

| 787 | Very Good |

| 788 | Very Good |

| 789 | Very Good |

| 790 | Very Good |

| 791 | Very Good |

| 792 | Very Good |

| 793 | Very Good |

| 794 | Very Good |

| 795 | Very Good |

| 796 | Very Good |

| 797 | Very Good |

| 798 | Very Good |

| 799 | Very Good |

| 800 | Excellent |

| 801 | Excellent |

| 802 | Excellent |

| 803 | Excellent |

| 804 | Excellent |

| 805 | Excellent |

| 806 | Excellent |

| 807 | Excellent |

| 808 | Excellent |

| 809 | Excellent |

| 810 | Excellent |

| 811 | Excellent |

| 812 | Excellent |

| 813 | Excellent |

| 814 | Excellent |

| 815 | Excellent |

| 816 | Excellent |

| 817 | Excellent |

| 818 | Excellent |

| 819 | Excellent |

| 820 | Excellent |

| 821 | Excellent |

| 822 | Excellent |

| 823 | Excellent |

| 824 | Excellent |

| 825 | Excellent |

| 826 | Excellent |

| 827 | Excellent |

| 828 | Excellent |

| 829 | Excellent |

| 830 | Excellent |

| 831 | Excellent |

| 832 | Excellent |

| 833 | Excellent |

| 834 | Excellent |

| 835 | Excellent |

| 836 | Excellent |

| 837 | Excellent |

| 838 | Excellent |

| 839 | Excellent |

| 840 | Excellent |

| 841 | Excellent |

| 842 | Excellent |

| 843 | Excellent |

| 844 | Excellent |

| 845 | Excellent |

| 846 | Excellent |

| 847 | Excellent |

| 848 | Excellent |

| 849 | Excellent |

| 850 | Excellent |

What Can You Get with a 810 Credit Score?

With an excellent 810, you have nearly unrestricted access to financial products:| Type of Credit | Eligibility |

|---|---|

| Secured Credit Card | Yes |

| Unsecured Credit Card | Yes |

| Best Rewards Credit Card | Yes |

| 0% APR Credit Card | Yes |

| Best Personal Loan | Yes |

| Mortgage | Yes |

| Auto Loan | Yes |

Common credit cards for a 810 credit score

There are numerous credit cards that you could apply for with a 810. Nonetheless, the best card for you hinges on your expenditure habits and financial objectives. With the comparison tool provided below, you can explore various credit cards designed for those with a 810. Alongside reviewing the APRs you're eligible for, ensure to familiarize yourself with the fees you may need to pay, including annual fees.Frequently chosen personal loans for a 810 credit score

Similar to credit cards, a 810 permits you to apply for a range of personal loans, including both secured and unsecured loans. However, to pinpoint the best personal loan for you, it's necessary to evaluate all your options.Auto loans with a 810 credit score

Fortunately, over half of all approved auto loans are made to applicants with FICO scores above 661, as per Experian. Although a score of 810 doesn't guarantee you an auto loan, you stand a good chance of being approved. Nevertheless, to ensure you secure the most favorable loan conditions, you may want to accumulate funds for a larger down payment or work on improving your credit score prior to applying for auto loans. As shown in the table below, a higher credit score can save you hundreds of dollars over the duration of the loan.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 720 - 850 | 6.511% | $237 | $1,386 |

| 690 - 719 | 7.744% | $243 | $1,661 |

| 660 - 689 | 9.573% | $252 | $2,076 |

| 620 - 659 | 10.739% | $257 | $2,345 |

| 590 - 619 | 15.055% | $279 | $3,372 |

| 500 - 589 | 16.484% | $286 | $3,723 |

| *Rates above for a $10,000 48-month used auto loan. |

Mortgages and home loans with a 810 credit score

Those with credit scores above 620 typically comprise a large percentage of successful mortgage applicants. Similarly to auto loans, enhancing your score can save you substantial amounts of money on a mortgage.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 760 - 850 | 6.129% | $304 | $59,416 |

| 700 - 759 | 6.351% | $311 | $62,014 |

| 680 - 699 | 6.528% | $317 | $64,104 |

| 660 - 679 | 6.742% | $324 | $66,652 |

| 640 - 659 | 7.172% | $338 | $71,841 |

| 620 - 639 | 7.718% | $357 | $78,556 |

| *Rates above for a $50,000 30-year fixed rate mortgage. |

Student loans with a 810 credit score

Fortunately, student loans are some of the most straightforward to obtain with a credit score of 810. As most students are still in the process of building credit, it's reasonable for student loans to have less rigorous credit prerequisites. Indeed, federal student loans typically don't require a minimum credit score. While private student loan lenders generally impose stricter requirements, a score of 810 should still allow you to secure the financing you need.Strategies to Maintain a 810 Credit Score

When your score is already excellent, your primary focus should be maintaining your score. Here are a few tips to keep your credit score in the excellent range:

- Consistently make payments on time: Continued timely payment of your bills and debts is crucial for maintaining your credit score.

- Keep a low credit utilization ratio: Even if you have high credit limits, aim to use a small percentage of your available credit. A low credit utilization ratio can help maintain your excellent score.

- Avoid opening too many new credit accounts at once: Each time you apply for new credit, it can lead to a hard inquiry on your credit report, which can temporarily lower your score. Even though you may qualify for new credit, consider the potential impact on your score before applying.

- Regularly check your credit report: Regularly review your credit report for errors. If you find any, dispute them as soon as possible. Even small errors can have a significant impact on your credit score.

FAQs

Can I get approved for credit with an 810 credit score?

Absolutely! An 810 credit score is excellent and can unlock doors to various types of credit, including credit cards, auto loans, and personal loans. Even some of the most attractive mortgage rates could be within your reach. But remember, the specific terms and interest rates you receive depend on more than just your credit score. Lenders will also consider your income and how much debt you currently have.

Is an 810 a good credit score for buying a house?

You bet! An 810 is a top-notch score that could help you secure a mortgage for your dream home. But keep in mind, getting approved for a home loan isn't only about your credit score. Lenders will also look at things like your debt-to-income ratio, employment history, and how much money you're putting down.

How much can I borrow with an 810 credit score?

While an 810 gives you a strong standing to qualify for substantial loans, the exact amount you can borrow will also depend on your income, the type of loan, and each lender's specific rules. Even with a great score like yours, always remember the golden rule of borrowing - only take on what you can comfortably pay back.

What perks come with an 810 credit score?

With an 810, you're looking at a whole host of benefits. Think lower interest rates on loans, smooth-sailing approval for rentals, potentially better rates on car insurance, and access to the best credit cards with top-tier rewards.

Is an 810 credit score rare?

While an 810 credit score is certainly something to be proud of, it's not exactly a unicorn. There are plenty of people out there with scores in this top-tier range.

Why is it tricky to achieve an 810 credit score?

Getting your hands on an 810 is no walk in the park because it takes time, patience, and super responsible credit behavior. This means always paying your bills on time, keeping your credit utilization down, and managing a healthy mix of credit accounts.

Key Takeaways

- With a 810, you're in the "Excellent" credit range according to FICO standards, which is an achievement only a select percentage of Americans manage.

- Your payment history plays a vital role in your score calculation, but maintaining this high score also relies heavily on keeping credit utilization low and managing a diverse portfolio of credit.

- Maintaining an "Excellent" score doesn't require as much "improvement" as it does "sustenance." This means keeping up with all payments, not maxing out your credit cards, and managing a mix of credit accounts responsibly.

- An "Excellent" credit score like a 810 should allow you to get approved for most loans or credit cards with the most favorable terms, including the lowest interest rates.

- Once you've reached this credit score range, the focus should be on maintenance and not letting your score slip. Remember, even small financial mishaps can cause larger dips when your score is this high.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: