658 Credit Score: Good Or Bad? And What Can I Get With A 658 Credit Score?

AL

Summary:

A 658 credit score is considered "Fair" by the FICO mmodel. Falling within the "Fair" credit score range, specifically a score between 580 and 669, suggests that you have a somewhat mixed credit history. While a 658 credit score is not the lowest, it can limit your access to some credit products, and you may face higher interest rates compared to those with higher scores.

Nonetheless, a "Fair" credit score is not a dead end. This guide will walk you through the intricacies of a "Fair" credit score, highlighting the opportunities and challenges it presents, as well as strategies to improve your credit standing. Remember, the journey to a better credit score is possible with patience, persistence, and responsible financial behaviors.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

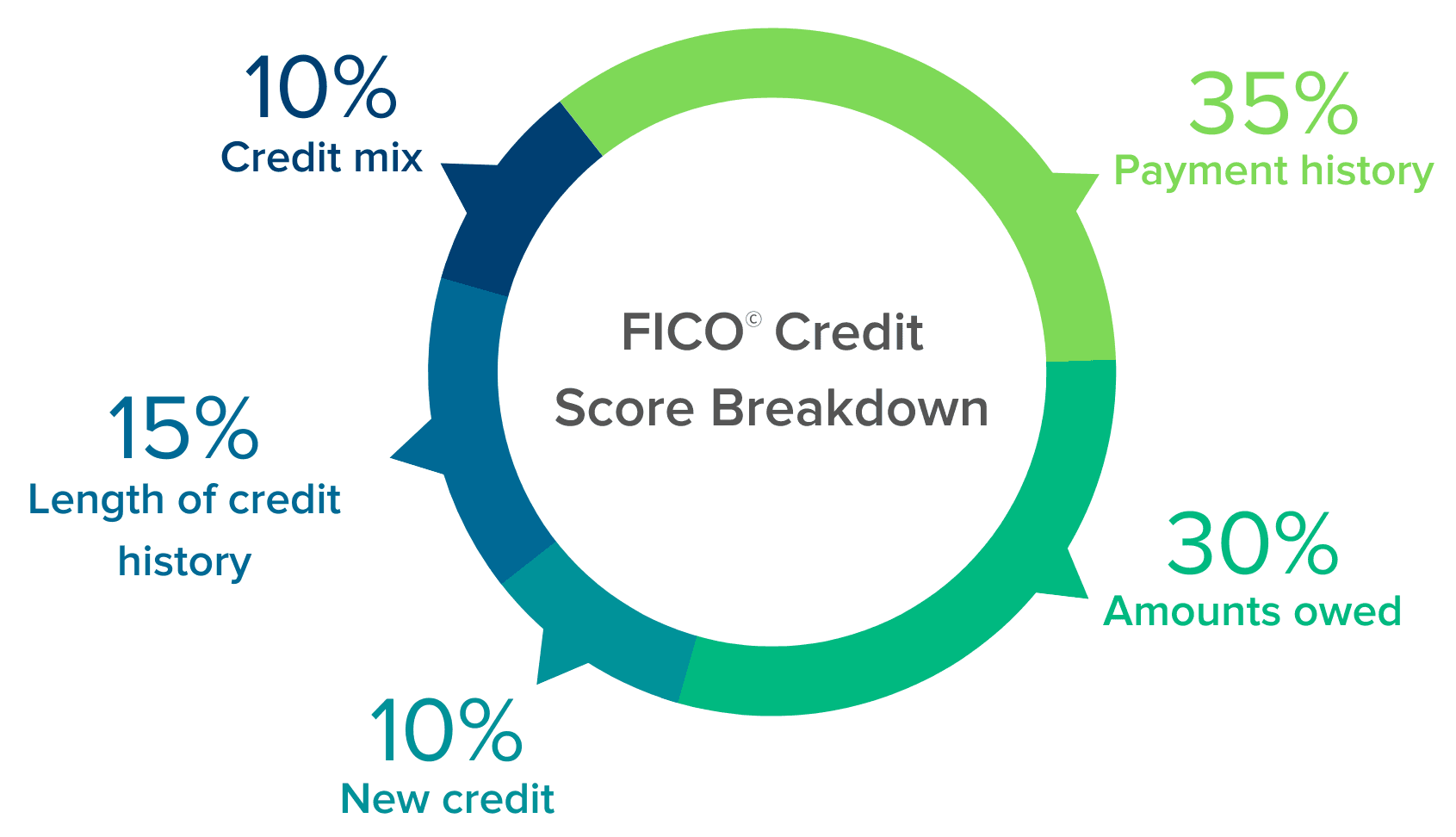

What determines your credit score?

Before we get into what this credit score means for you and your finances, let's take a brief look at what credit scores actually are. Your credit score is broken into a few different categories, each of which contributes to the total score.

- Payment history. Your payment history has the biggest effect on your credit score and is exactly what it says: a record of your bill and credit payments. This tracks the number of on-time and late payments you make, whether on loans, credit card accounts, utility bills or other services.

- Amounts owed. This refers to how much available credit you have compared to how much credit you owe. You can also think of this as your credit utilization ratio, which should ideally be kept below 30%. For instance, if you've reached the credit limit on numerous credit cards, this will likely lower your score.

- Length of credit history. How long you keep a credit account open matters, even if you don't actively use that credit line. This factor considers the age of your oldest and newest credit accounts as well as the average age of all your accounts together.

- Credit mix. While it may sound counterproductive to have multiple credit accounts, a mix of different accounts is actually a good thing. Having a couple of credit cards, an auto loan, and a mortgage shows lenders that you can manage several types of credit responsibly.

- New credit. "New" credit specifically looks at how many credit accounts you opened recently and the number of credit inquiries made into your account. Each time you apply for a new loan or line of credit, the lender will make an inquiry into your credit history to review your score and payment history.

Pro Tip

Keep in mind that the categories above are used to calculate FICO credit scores, but these categories are also used in other models. There are two other models for calculating credit scores — VantageScore and PLUS. While lenders don't typically look at PLUS scores, many lenders and loan officers check VantageScore. So when reviewing your score and credit history, don't forget to check all of your credit scores.

What does it mean to have a 658 credit score?

A 658 credit score is below the average credit score. Though a small percentage of Americans have credit scores below 669, Experian found that these borrowers were likely to become "seriously delinquent," or more than 90 days late on a bill or debt payment. With this in mind, it makes sense that lenders would be hesitant to offer financing to an applicant with a 658 credit score.| Credit score range | % of consumers | Delinquency rate |

|---|---|---|

| 300-579 | 16% | 61% |

| 580-669 | 17% | 28% |

| 670-739 | 21% | 8% |

| 740-799 | 25% | 2% |

| 800-850 | 21% | 1% |

Related reading: Though fair credit scores can make it difficult to receive loans or credit cards, having no credit isn't great either. To learn more about this, take a look at our article on the topic.

How does this score compare to others?

Unfortunately, as we mentioned above, a 658 credit score isn't great. You may have a difficult time getting an auto loan, and you may not have access to a high credit limit on a secured credit card either. And as you can see from the data below, the average credit score is only increasing with time.The table below links to in-depth articles for all credit scores.

| Credit score | Scale |

|---|---|

| 300 | Poor |

| 301 | Poor |

| 302 | Poor |

| 303 | Poor |

| 304 | Poor |

| 305 | Poor |

| 306 | Poor |

| 307 | Poor |

| 308 | Poor |

| 309 | Poor |

| 310 | Poor |

| 311 | Poor |

| 312 | Poor |

| 313 | Poor |

| 314 | Poor |

| 315 | Poor |

| 316 | Poor |

| 317 | Poor |

| 318 | Poor |

| 319 | Poor |

| 320 | Poor |

| 321 | Poor |

| 322 | Poor |

| 323 | Poor |

| 324 | Poor |

| 325 | Poor |

| 326 | Poor |

| 327 | Poor |

| 328 | Poor |

| 329 | Poor |

| 330 | Poor |

| 331 | Poor |

| 332 | Poor |

| 333 | Poor |

| 334 | Poor |

| 335 | Poor |

| 336 | Poor |

| 337 | Poor |

| 338 | Poor |

| 339 | Poor |

| 340 | Poor |

| 341 | Poor |

| 342 | Poor |

| 343 | Poor |

| 344 | Poor |

| 345 | Poor |

| 346 | Poor |

| 347 | Poor |

| 348 | Poor |

| 349 | Poor |

| 350 | Poor |

| 351 | Poor |

| 352 | Poor |

| 353 | Poor |

| 354 | Poor |

| 355 | Poor |

| 356 | Poor |

| 357 | Poor |

| 358 | Poor |

| 359 | Poor |

| 360 | Poor |

| 361 | Poor |

| 362 | Poor |

| 363 | Poor |

| 364 | Poor |

| 365 | Poor |

| 366 | Poor |

| 367 | Poor |

| 368 | Poor |

| 369 | Poor |

| 370 | Poor |

| 371 | Poor |

| 372 | Poor |

| 373 | Poor |

| 374 | Poor |

| 375 | Poor |

| 376 | Poor |

| 377 | Poor |

| 378 | Poor |

| 379 | Poor |

| 380 | Poor |

| 381 | Poor |

| 382 | Poor |

| 383 | Poor |

| 384 | Poor |

| 385 | Poor |

| 386 | Poor |

| 387 | Poor |

| 388 | Poor |

| 389 | Poor |

| 390 | Poor |

| 391 | Poor |

| 392 | Poor |

| 393 | Poor |

| 394 | Poor |

| 395 | Poor |

| 396 | Poor |

| 397 | Poor |

| 398 | Poor |

| 399 | Poor |

| 400 | Poor |

| 401 | Poor |

| 402 | Poor |

| 403 | Poor |

| 404 | Poor |

| 405 | Poor |

| 406 | Poor |

| 407 | Poor |

| 408 | Poor |

| 409 | Poor |

| 410 | Poor |

| 411 | Poor |

| 412 | Poor |

| 413 | Poor |

| 414 | Poor |

| 415 | Poor |

| 416 | Poor |

| 417 | Poor |

| 418 | Poor |

| 419 | Poor |

| 420 | Poor |

| 421 | Poor |

| 422 | Poor |

| 423 | Poor |

| 424 | Poor |

| 425 | Poor |

| 426 | Poor |

| 427 | Poor |

| 428 | Poor |

| 429 | Poor |

| 430 | Poor |

| 431 | Poor |

| 432 | Poor |

| 433 | Poor |

| 434 | Poor |

| 435 | Poor |

| 436 | Poor |

| 437 | Poor |

| 438 | Poor |

| 439 | Poor |

| 440 | Poor |

| 441 | Poor |

| 442 | Poor |

| 443 | Poor |

| 444 | Poor |

| 445 | Poor |

| 446 | Poor |

| 447 | Poor |

| 448 | Poor |

| 449 | Poor |

| 450 | Poor |

| 451 | Poor |

| 452 | Poor |

| 453 | Poor |

| 454 | Poor |

| 455 | Poor |

| 456 | Poor |

| 457 | Poor |

| 458 | Poor |

| 459 | Poor |

| 460 | Poor |

| 461 | Poor |

| 462 | Poor |

| 463 | Poor |

| 464 | Poor |

| 465 | Poor |

| 466 | Poor |

| 467 | Poor |

| 468 | Poor |

| 469 | Poor |

| 470 | Poor |

| 471 | Poor |

| 472 | Poor |

| 473 | Poor |

| 474 | Poor |

| 475 | Poor |

| 476 | Poor |

| 477 | Poor |

| 478 | Poor |

| 479 | Poor |

| 480 | Poor |

| 481 | Poor |

| 482 | Poor |

| 483 | Poor |

| 484 | Poor |

| 485 | Poor |

| 486 | Poor |

| 487 | Poor |

| 488 | Poor |

| 489 | Poor |

| 490 | Poor |

| 491 | Poor |

| 492 | Poor |

| 493 | Poor |

| 494 | Poor |

| 495 | Poor |

| 496 | Poor |

| 497 | Poor |

| 498 | Poor |

| 499 | Poor |

| 500 | Poor |

| 501 | Poor |

| 502 | Poor |

| 503 | Poor |

| 504 | Poor |

| 505 | Poor |

| 506 | Poor |

| 507 | Poor |

| 508 | Poor |

| 509 | Poor |

| 510 | Poor |

| 511 | Poor |

| 512 | Poor |

| 513 | Poor |

| 514 | Poor |

| 515 | Poor |

| 516 | Poor |

| 517 | Poor |

| 518 | Poor |

| 519 | Poor |

| 520 | Poor |

| 521 | Poor |

| 522 | Poor |

| 523 | Poor |

| 524 | Poor |

| 525 | Poor |

| 526 | Poor |

| 527 | Poor |

| 528 | Poor |

| 529 | Poor |

| 530 | Poor |

| 531 | Poor |

| 532 | Poor |

| 533 | Poor |

| 534 | Poor |

| 535 | Poor |

| 536 | Poor |

| 537 | Poor |

| 538 | Poor |

| 539 | Poor |

| 540 | Poor |

| 541 | Poor |

| 542 | Poor |

| 543 | Poor |

| 544 | Poor |

| 545 | Poor |

| 546 | Poor |

| 547 | Poor |

| 548 | Poor |

| 549 | Poor |

| 550 | Poor |

| 551 | Poor |

| 552 | Poor |

| 553 | Poor |

| 554 | Poor |

| 555 | Poor |

| 556 | Poor |

| 557 | Poor |

| 558 | Poor |

| 559 | Poor |

| 560 | Poor |

| 561 | Poor |

| 562 | Poor |

| 563 | Poor |

| 564 | Poor |

| 565 | Poor |

| 566 | Poor |

| 567 | Poor |

| 568 | Poor |

| 569 | Poor |

| 570 | Poor |

| 571 | Poor |

| 572 | Poor |

| 573 | Poor |

| 574 | Poor |

| 575 | Poor |

| 576 | Poor |

| 577 | Poor |

| 578 | Poor |

| 579 | Poor |

| 580 | Fair |

| 581 | Fair |

| 582 | Fair |

| 583 | Fair |

| 584 | Fair |

| 585 | Fair |

| 586 | Fair |

| 587 | Fair |

| 588 | Fair |

| 589 | Fair |

| 590 | Fair |

| 591 | Fair |

| 592 | Fair |

| 593 | Fair |

| 594 | Fair |

| 595 | Fair |

| 596 | Fair |

| 597 | Fair |

| 598 | Fair |

| 599 | Fair |

| 600 | Fair |

| 601 | Fair |

| 602 | Fair |

| 603 | Fair |

| 604 | Fair |

| 605 | Fair |

| 606 | Fair |

| 607 | Fair |

| 608 | Fair |

| 609 | Fair |

| 610 | Fair |

| 611 | Fair |

| 612 | Fair |

| 613 | Fair |

| 614 | Fair |

| 615 | Fair |

| 616 | Fair |

| 617 | Fair |

| 618 | Fair |

| 619 | Fair |

| 620 | Fair |

| 621 | Fair |

| 622 | Fair |

| 623 | Fair |

| 624 | Fair |

| 625 | Fair |

| 626 | Fair |

| 627 | Fair |

| 628 | Fair |

| 629 | Fair |

| 630 | Fair |

| 631 | Fair |

| 632 | Fair |

| 633 | Fair |

| 634 | Fair |

| 635 | Fair |

| 636 | Fair |

| 637 | Fair |

| 638 | Fair |

| 639 | Fair |

| 640 | Fair |

| 641 | Fair |

| 642 | Fair |

| 643 | Fair |

| 644 | Fair |

| 645 | Fair |

| 646 | Fair |

| 647 | Fair |

| 648 | Fair |

| 649 | Fair |

| 650 | Fair |

| 651 | Fair |

| 652 | Fair |

| 653 | Fair |

| 654 | Fair |

| 655 | Fair |

| 656 | Fair |

| 657 | Fair |

| 658 | Fair |

| 659 | Fair |

| 660 | Fair |

| 661 | Fair |

| 662 | Fair |

| 663 | Fair |

| 664 | Fair |

| 665 | Fair |

| 666 | Fair |

| 667 | Fair |

| 668 | Fair |

| 669 | Fair |

| 670 | Good |

| 671 | Good |

| 672 | Good |

| 673 | Good |

| 674 | Good |

| 675 | Good |

| 676 | Good |

| 677 | Good |

| 678 | Good |

| 679 | Good |

| 680 | Good |

| 681 | Good |

| 682 | Good |

| 683 | Good |

| 684 | Good |

| 685 | Good |

| 686 | Good |

| 687 | Good |

| 688 | Good |

| 689 | Good |

| 690 | Good |

| 691 | Good |

| 692 | Good |

| 693 | Good |

| 694 | Good |

| 695 | Good |

| 696 | Good |

| 697 | Good |

| 698 | Good |

| 699 | Good |

| 700 | Good |

| 701 | Good |

| 702 | Good |

| 703 | Good |

| 704 | Good |

| 705 | Good |

| 706 | Good |

| 707 | Good |

| 708 | Good |

| 709 | Good |

| 710 | Good |

| 711 | Good |

| 712 | Good |

| 713 | Good |

| 714 | Good |

| 715 | Good |

| 716 | Good |

| 717 | Good |

| 718 | Good |

| 719 | Good |

| 720 | Good |

| 721 | Good |

| 722 | Good |

| 723 | Good |

| 724 | Good |

| 725 | Good |

| 726 | Good |

| 727 | Good |

| 728 | Good |

| 729 | Good |

| 730 | Good |

| 731 | Good |

| 732 | Good |

| 733 | Good |

| 734 | Good |

| 735 | Good |

| 736 | Good |

| 737 | Good |

| 738 | Good |

| 739 | Good |

| 740 | Very Good |

| 741 | Very Good |

| 742 | Very Good |

| 743 | Very Good |

| 744 | Very Good |

| 745 | Very Good |

| 746 | Very Good |

| 747 | Very Good |

| 748 | Very Good |

| 749 | Very Good |

| 750 | Very Good |

| 751 | Very Good |

| 752 | Very Good |

| 753 | Very Good |

| 754 | Very Good |

| 755 | Very Good |

| 756 | Very Good |

| 757 | Very Good |

| 758 | Very Good |

| 759 | Very Good |

| 760 | Very Good |

| 761 | Very Good |

| 762 | Very Good |

| 763 | Very Good |

| 764 | Very Good |

| 765 | Very Good |

| 766 | Very Good |

| 767 | Very Good |

| 768 | Very Good |

| 769 | Very Good |

| 770 | Very Good |

| 771 | Very Good |

| 772 | Very Good |

| 773 | Very Good |

| 774 | Very Good |

| 775 | Very Good |

| 776 | Very Good |

| 777 | Very Good |

| 778 | Very Good |

| 779 | Very Good |

| 780 | Very Good |

| 781 | Very Good |

| 782 | Very Good |

| 783 | Very Good |

| 784 | Very Good |

| 785 | Very Good |

| 786 | Very Good |

| 787 | Very Good |

| 788 | Very Good |

| 789 | Very Good |

| 790 | Very Good |

| 791 | Very Good |

| 792 | Very Good |

| 793 | Very Good |

| 794 | Very Good |

| 795 | Very Good |

| 796 | Very Good |

| 797 | Very Good |

| 798 | Very Good |

| 799 | Very Good |

| 800 | Excellent |

| 801 | Excellent |

| 802 | Excellent |

| 803 | Excellent |

| 804 | Excellent |

| 805 | Excellent |

| 806 | Excellent |

| 807 | Excellent |

| 808 | Excellent |

| 809 | Excellent |

| 810 | Excellent |

| 811 | Excellent |

| 812 | Excellent |

| 813 | Excellent |

| 814 | Excellent |

| 815 | Excellent |

| 816 | Excellent |

| 817 | Excellent |

| 818 | Excellent |

| 819 | Excellent |

| 820 | Excellent |

| 821 | Excellent |

| 822 | Excellent |

| 823 | Excellent |

| 824 | Excellent |

| 825 | Excellent |

| 826 | Excellent |

| 827 | Excellent |

| 828 | Excellent |

| 829 | Excellent |

| 830 | Excellent |

| 831 | Excellent |

| 832 | Excellent |

| 833 | Excellent |

| 834 | Excellent |

| 835 | Excellent |

| 836 | Excellent |

| 837 | Excellent |

| 838 | Excellent |

| 839 | Excellent |

| 840 | Excellent |

| 841 | Excellent |

| 842 | Excellent |

| 843 | Excellent |

| 844 | Excellent |

| 845 | Excellent |

| 846 | Excellent |

| 847 | Excellent |

| 848 | Excellent |

| 849 | Excellent |

| 850 | Excellent |

What does a 658 credit score get you?

Even though a 658 credit score is considered "Fair," you'll still have some financing options available to you, as you can see below.| Type of credit | Qualify? |

|---|---|

| Secured credit card | Yes |

| Unsecured credit card | Yes |

| Best rewards credit card | No |

| 0% APR credit card | Unlikely |

| Personal loan | Yes |

| Apartment rent | Probably |

| Home loan | Yes (especially VA and FHA mortgages) |

| Auto loan | Probably |

IMPORTANT! Keep in mind that the information above isn't absolute. For instance, your application for an auto loan may be accepted, but you probably won't receive the best terms or interest rate.

Popular credit cards for a 658 credit score

Most of the best credit cards to apply for with a 658 credit score are secured cards. However, that's not the only type available to applicants with fair credit scores. Using our comparison tool below, you can compare different credit cards that accept applicants with a 658 credit score. In addition to reviewing what APRs you qualify for, make sure you know what fees you'll pay as well, such as an annual fee.Popular personal loans for a 658 credit score

Just as with credit cards, the most popular personal loans for consumers with scores around 658 will mostly be secured personal loans. While these aren't the only personal loans available, they'll probably offer applicants with fair credit scores the best loan terms.IMPORTANT! Though you may be tempted to apply for a payday loan, it's usually best to avoid them. Payday loans have very high interest rates and can push borrowers into a cycle of debt and could result in an even worse credit score.

Auto loans with a 658 credit score

Unfortunately, applicants with FICO scores around 658 may have a tough time getting auto loans. Though this score doesn't outright prevent you from getting an auto loan, you may have poor loan terms with a high interest rate. Instead, you may be better off saving up and improving your credit score before applying for auto loans. As you can see from the table below, a higher credit score can save you hundreds of dollars over the life of the loan.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 720 - 850 | 6.511% | $237 | $1,386 |

| 690 - 719 | 7.744% | $243 | $1,661 |

| 660 - 689 | 9.573% | $252 | $2,076 |

| 620 - 659 | 10.739% | $257 | $2,345 |

| 590 - 619 | 15.055% | $279 | $3,372 |

| 500 - 589 | 16.484% | $286 | $3,723 |

| *Rates above for a $10,000 48-month used auto loan. |

Mortgages and home loans with a 658 credit score

Consumers with credit scores below 620 typically make up a small percentage of successful mortgage applicants. This means mortgage lenders may refuse to work with applicants that have credit scores around 658. By creating a savings plan and improving your credit score first, you may receive better financing down the line. For example, if you get your credit score above 620, you may qualify for a conventional home loan instead. Just as higher credit scores save you money in auto loan interest rates, improving your score can save you even more money on a mortgage.| Credit score | APR | Monthly payment | Total interest paid |

|---|---|---|---|

| 760 - 850 | 6.129% | $304 | $59,416 |

| 700 - 759 | 6.351% | $311 | $62,014 |

| 680 - 699 | 6.528% | $317 | $64,104 |

| 660 - 679 | 6.742% | $324 | $66,652 |

| 640 - 659 | 7.172% | $338 | $71,841 |

| 620 - 639 | 7.718% | $357 | $78,556 |

| *Rates above for a $50,000 30-year fixed rate mortgage. |

Student loans with a 658 credit score

Fortunately, student loans are some of the easiest loans to receive with a credit score of 658. Since most students are still building credit at this time, it makes sense that student loans would have less strict credit requirements. In fact, federal student loans generally don't have credit requirements at all. However, private student loan lenders usually have more stringent requirements and may not accept an applicant with a 658 credit score. Because of this, your chances will be much better if you have a cosigner.How to improve a 658 credit score

With all of this in mind, there is some good news if you fall in the "Fair" credit range: You have a lot of room to achieve a higher credit score over time.Catch up on past-due payments

We know it's easier said than done, but repaying your old bills and debts can help improve your credit score. This is especially true when it comes to the most recent versions of FICO and VantageScore credit scores. Newer credit scoring models ignore collections that have a zero balance. So, if you pay or settle a collection and it's updated to reflect the zero balance on your credit reports, your FICO® 9 and VantageScore 3.0 and 4.0 scores may improve. However, scores generated by older models that do not ignore zero-balance accounts will not improve. However, it can be tricky to know how to best tackle your debts when you first start out. Luckily, you have a few options available to you:- Do it yourself. This is the most obvious plan. Using a calendar, day planner, or money management tool, start budgeting and tracking your payments regularly. It won't be easy, but by creating a solid repayment strategy you can chip away at your debts and lower your credit utilization ratio. You should also consider which debt repayment strategy is right for you before starting.

- Apply for a debt consolidation loan. If you have multiple debts to pay off, consolidating your debts into one payment can make repayment easier to track and manage. While you may have to search for a secured loan, consolidating your debts can help debt payments feel more manageable.

- Consult a debt settlement company. If your debts seem too large to tackle, talking to a debt settlement company may help you reduce your debts to something more doable. While they won't pay your debts for you, a debt settlement company can help reduce the amount you owe to a particular creditor.

Review your credit reports for errors

Sometimes, a poor credit score isn't your fault. Though we'd all like to believe mistakes won't be made when it comes to our credit, there's always a chance you could have an error on your credit report. It could be the result of fraud, where your information was stolen and used to open a credit line or loan, or a simple mistake by the major credit bureaus. Regardless of what happened, make sure to regularly review your credit report for any errors. If you don't have the time to monitor your credit score yourself, consider hiring a credit repair company instead. Their job is to review your credit history and report any false information on your behalf, which could end up improving your score.Pro Tip

You can request a free credit report from each of the three credit bureaus once a year. If you haven't done so already, visit AnnualCreditReport.com to get your free credit report today.

Be patient after a foreclosure or repossession

After a foreclosure or repossession, you may feel like you need to work quickly to better your credit score. The reality is that a foreclosure or repossession typically happens after multiple missed payments and attempts to collect those payments. Because of those attempts, a foreclosure won't be the only bad mark on your credit report. And once a repossession is part of your credit history, you'll likely see your score drop significantly, often 100 or more points. What does this mean for you? Patience. Instead of scrambling to repay every debt you have and anxiously monitoring your score, understand that repairing poor credit doesn't happen overnight. It may take several months or years to return your credit score to its previous glory. On top of that, repossession may stay on your credit report for up to seven years. That doesn't mean stop trying, but rather be patient and take small steps towards your debt repayment goal. If you're not sure where to start, read this guide. You can also reach out to a certified financial planner or a credit counseling company. They can help you budget and create a debt repayment strategy that works with your finances.Open a secured credit card account

One way to show your creditworthiness is through a secured credit card. To use a secured card, you first have to pay a security deposit, which the card issuer holds onto. If you ever miss a card payment, the card issuer uses the security deposit towards your balance. This can be a great way to improve your credit score and manage credit card debt more effectively. Take a look at some of the secured credit cards below and compare card features to find the best one for your spending habits.FAQs

How long does it take to go from 658 to an 800 credit score?

Raising a credit score from 658 to 800 is a significant jump and takes time. Depending on your specific situation, it could take anywhere from a couple of years to a decade or more. Improvement depends on many factors, including paying off debt, making payments on time, and avoiding new debt.How to get my credit from 658 to 700?

Improving your credit score from 658 to 700 involves making consistent on-time payments, paying off debt, keeping low credit card balances, not applying for new credit frequently, and rectifying any inaccuracies on your credit report. It's a process that may take several months to a year.What credit score do you start with?

When you're new to credit, you don't start with a credit score. Only after about six months of credit activity will a FICO score be generated for you. Initial scores often range from the mid-600s to the mid-700s.How to raise your credit score 200 points in 30 days?

Raising your credit score by 200 points in 30 days is unlikely. Credit improvement takes time, usually a few months to several years. It involves making on-time payments, paying off debt, and maintaining low balances on your credit cards.What is a perfect credit score?

The highest possible score under the FICO scoring model is 850, which is considered a perfect credit score. However, anything above 800 is usually categorized as exceptional and can qualify you for the best interest rates and credit terms.Can you get anything with a 658 credit score?

Yes, with a 658 credit score, you can still qualify for some types of credit, such as personal loans or auto loans, but expect less favorable terms and higher interest rates. You may also be eligible for certain credit cards, particularly those designed for individuals with fair or average credit.Is 658 a good credit score?

A 658 credit score is typically considered "fair". It's not in the poor range, but it's also not in the good or excellent range. It may limit your options and result in higher interest rates.What is the difference between FICO credit scores, VantageScore, and PLUS?

FICO and VantageScore are the two most popular credit scoring models in the United States. They are both used by lenders to assess your creditworthiness, and they both have a range of 300 to 850, with higher scores indicating better credit.

Here are some of the key differences between FICO and VantageScore:

- FICO scores are more widely used by lenders. About 90% of lenders use FICO scores, while only about 60% use VantageScore. FICO scores are more complex than VantageScore. FICO scores use a variety of factors to calculate your score, including your payment history, credit utilization, length of credit history, and recent inquiries. VantageScore uses a simpler model that focuses on your payment history and credit utilization.

- Also, VantageScore scores are more forgiving of recent inquiries. VantageScore counts multiple inquiries, even for different types of loans, within a 14-day period as a single inquiry. FICO scores only dedupe multiple inquiries from student loan, auto loan, and mortgage applications.

- PLUS is a newer credit scoring model that is still gaining traction. It is designed to be more transparent than FICO and VantageScore, and it uses a variety of factors to calculate your score, including your payment history, credit utilization, length of credit history, and credit mix.

Here is a table that summarizes the key differences between FICO, VantageScore, and PLUS:

| Feature | FICO | VantageScore | PLUS |

|---|---|---|---|

| Range | 300 to 850 | 300 to 850 | 250 to 900 |

| Popularity | Most widely used | Less widely used | Newer model |

| Complexity | More complex | Simpler model | More transparent |

| Inquiries | Multiple inquiries within a 14-day period count as a single inquiry | Multiple inquiries within a 14-day period count as multiple inquiries | Multiple inquiries within a 14-day period count as a single inquiry |

| Factors used | Payment history, credit utilization, length of credit history, and recent inquiries | Payment history, credit utilization, length of credit history | Payment history, credit utilization, length of credit history, and credit mix |

Can you get approved for a loan with a 658 credit score?

Yes, you can get approved for a loan with a 658 credit score, but it may be more challenging and potentially more expensive. Your credit score is a key factor that lenders consider when assessing your creditworthiness. A score of 658 is typically considered "fair", which means you're seen as a higher risk borrower compared to someone with a better score. As a result, while you may still qualify for certain loans such as personal loans, auto loans, or even mortgages, you're likely to face higher interest rates and less favorable terms. In some cases, you might be asked to provide a co-signer or secure your loan with collateral. It's advisable to improve your credit score before applying for large loans to secure better terms.

How can I raise my credit score from 658 to 700?

To boost your credit score from 658 to 700, first, regularly review your credit report and dispute any inaccuracies. Aim to pay all your bills on time, as timely payments significantly influence your score. Try to pay down credit card balances to lower your credit utilization rate - ideally, keep it under 30%. Avoid taking on new debt that's not necessary, but maintain a mix of credit types (like credit cards, auto loans, mortgages) to show you can handle different types of credit. Finally, establish a long history of good credit habits, and avoid actions that could result in negative marks on your credit report. Patience is key; improving a credit score doesn't happen overnight.

What credit score do you start with?

There technically isn't a "starting" credit score, at least not one that everyone starts with. If you haven't ever applied for a loan or credit card, you won't have a credit score at all. Once you apply for your first loan or card, the three major credit bureaus will begin building a credit file based on how you manage your account.

What is the lowest credit score?

Technically, the lowest credit score possible is 300, but you'll only have this score if you manage your finances extremely poorly.

Key Takeaways

- A 658 credit score is considered "Fair" by FICO score standards and represents a small percentage of Americans.

- The most influential factor when calculating a credit score is the consumer's payment history.

- To improve your score, try paying down current debts, reviewing your credit report, or applying for secured cards or personal loans.

- Applicants with a 658 credit score may have a tough time receiving a mortgage or car loan.

- Repairing your credit score doesn't happen overnight. It may take some time to raise your credit score from 658 to 700 or above.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: