Home Equity Loan To Buy Land

Last updated 05/19/2026 by

Benjamin Locke

Edited by

Andrew Latham

Summary:

A home equity loan allows homeowners to borrow against the equity in their property. For those looking to buy land, this can be an effective option. The most common alternative is a dedicated land loan, which uses the purchased land itself as collateral instead of your home. This article explores what home equity loans are, how they work, and their potential for financing land purchases. We also cover the pros, cons, and key considerations to keep in mind when using this financial product for land acquisition.

Thinking about a home equity loan to buy land? You have come to the right place. Let´s break it down below.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

What is a home equity loan?

A home equity loan is a type of loan where the borrower uses the equity of their property as collateral. Home equity is the difference between the current market value of your home and the outstanding mortgage balance. It allows homeowners to borrow a lump sum, typically with fixed interest rates and repayment terms, based on the amount of equity they have in their property.

How does a home equity loan work?

Home equity loans work by allowing homeowners to borrow a percentage of their equity, which is calculated by subtracting the remaining mortgage balance from the home’s current value. The lender typically offers a fixed loan amount, and the borrower is required to make monthly payments over a set period. These loans are often easier to obtain for homeowners with significant equity in their homes.

Using a home equity loan to buy land

Using a home equity loan to buy land is one option for homeowners looking to invest in property or expand their real estate portfolio. The process is similar to any other real estate purchase, but with the added benefit of leveraging your existing home equity for funding. To use a home equity loan to buy land, you’ll need to follow these steps:

- Determine your home’s equity: First, calculate the equity in your home by subtracting your remaining mortgage balance from the current market value of your property. This equity will determine how much you can borrow.

- Apply for a home equity loan: Contact lenders to apply for the loan. You’ll need to provide information about your financial situation and the land you’re purchasing. Some lenders may require a property appraisal to determine the land’s value.

- Use the loan for the land purchase: Once approved, you’ll receive the loan amount, which can then be used to buy the land. Depending on the terms of your loan, you may receive the funds as a lump sum.

Advantages and disadvantages of using a home equity loan to buy land

When considering a home equity loan to purchase land, it’s important to weigh the benefits and potential drawbacks. Below is a breakdown of the key advantages and disadvantages to help you make an informed decision:

| Advantages | Disadvantages |

|---|---|

| Lower interest rates: Since the loan is secured by your home, home equity loans typically offer lower interest rates than unsecured loans or credit cards. | Risk of foreclosure: Since your home is used as collateral, failure to repay the loan could result in foreclosure, potentially losing both your home and the land you purchased. |

| Fixed payment terms: Most home equity loans come with fixed interest rates and payment terms, making it easier to plan your budget and manage repayments. | Property value considerations: Buying land with a home equity loan can be risky if the land does not appreciate in value or if you struggle to sell it later. |

| Access to a lump sum: If you’re buying land, having a lump sum can help with the entire purchase or cover a significant portion of it, without needing to apply for multiple loans. | Limited availability for vacant land: Some lenders may be hesitant to approve home equity loans for land purchases, especially if the land is undeveloped or considered a riskier investment. |

Factors to consider before using a home equity loan for land purchase

1. Loan-to-value ratio (LTV)

The LTV ratio is a key factor in determining how much you can borrow. Most lenders allow you to borrow up to 80% to 85% of the value of your home. This means that if your home is worth $300,000 and you owe $150,000, you may be able to borrow up to $105,000 (80% of $300,000 minus $150,000).

2. Land value and appraisal

Lenders typically require a property appraisal to determine the value of the land you’re purchasing. If the land is not fully developed or lacks certain features, the appraisal value might not be as high as you expect, potentially limiting the amount you can borrow.

Appraised values vary dramatically by region — land in the cheapest states may not require as large a loan, making a home equity line more than sufficient.

3. Interest rates

Interest rates for home equity loans can vary depending on the lender and your creditworthiness. Typically, fixed rates are available, but rates may be higher for land purchases than for traditional home improvements or other uses. Compare rates and terms from different lenders before committing.

4. Risk tolerance

Buying land with a home equity loan is a higher-risk investment, especially if the land is undeveloped or you don’t have a clear plan for future use. Undeveloped land carries risks beyond financing — review the full pros and cons of buying undeveloped land before committing equity from your home. If the investment doesn’t pay off, you risk both your home and the land you bought. Carefully assess your financial stability and future prospects before proceeding.

Borrowers without significant home equity may consider using a personal loan to buy land, though interest rates tend to run higher.

How much can I borrow with a home equity loan to buy land?

The amount you can borrow with a home equity loan depends on the equity in your home and the lender’s loan-to-value (LTV) ratio.

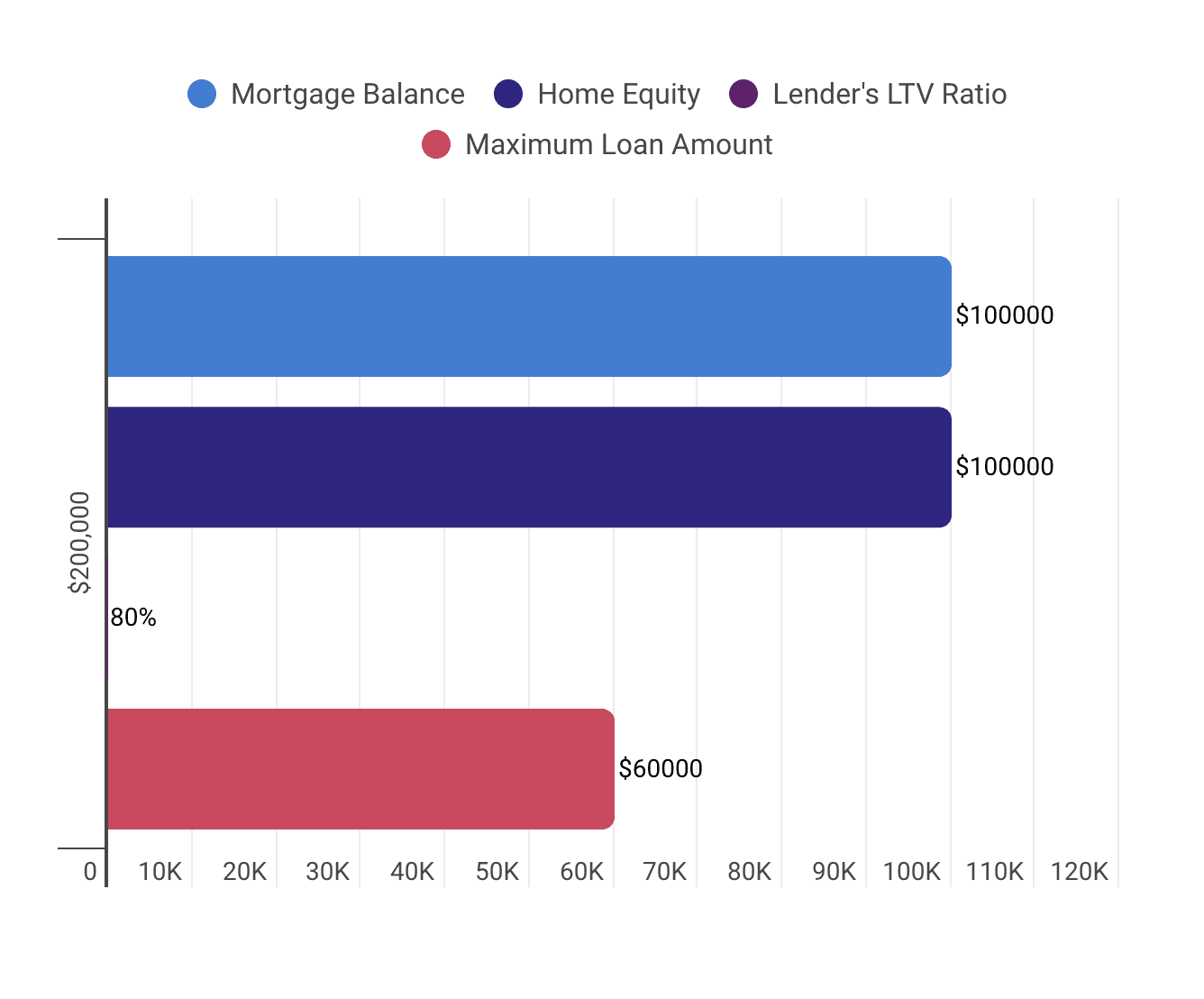

Priya owns a home valued at $200,000 and has a remaining mortgage balance of $100,000, leaving her with $100,000 in equity. She’s considering using a home equity loan to purchase a nearby plot of land for future development.

After approaching a lender, Priya learns that their loan-to-value (LTV) ratio is 80%. The lender calculates 80% of her home’s value as $160,000. Subtracting her $100,000 mortgage balance from this amount, the lender determines she is eligible to borrow up to $60,000 through a home equity loan. With this loan, Priya can fund her land purchase while maintaining manageable monthly payments.

| Home Value | Mortgage Balance | Home Equity | Lender’s LTV Ratio | Maximum Loan Amount |

|---|---|---|---|---|

| $200,000 | $100,000 | $100,000 | 80% | $60,000 |

In this example, Priya could borrow up to $60,000 with a home equity loan to purchase land. However, keep in mind that the amount you can borrow may be limited if the land’s value isn’t high or if your credit score and financial situation don’t meet the lender’s requirements.

How to apply for a home equity loan

Applying for a home equity loan to buy land involves a few simple steps:

- Check your credit score: A higher score can secure better terms.

- Determine your home’s equity: Subtract your mortgage balance from your home’s value.

- Shop around for lenders: Compare interest rates and fees.

- Submit your application: Provide personal financial details and land information.

- Close the loan: Sign the agreement and receive the funds for your land purchase.

What fees are involved in a home equity loan for land?

When using a home equity loan to buy land, there are various fees you should be aware of. These fees are often similar to the ones involved in traditional home purchases and can include:

- Origination fees: These are the fees charged by the lender for processing the loan application. Typically, these fees range from 0.5% to 1% of the total loan amount.

- Appraisal fees: Lenders often require an appraisal to determine the value of your home and the land you plan to purchase. The cost of an appraisal can range from $300 to $600 or more, depending on the complexity of the property.

- Closing costs: These are one-time charges for finalizing the loan. Closing costs can include title insurance, attorney fees, recording fees, and other administrative charges. These costs can range from 2% to 5% of the loan amount.

- Inspection fees: If the lender requires a land inspection to assess the property’s suitability for development or its condition, this could incur an additional cost.

- Prepayment penalties: Some lenders may charge a fee if you pay off your loan early. Check your loan terms to see if there are any penalties for early repayment.

FAQ

What are the risks of using a home equity loan for land investment?

Using a home equity loan for land investment carries certain risks. If you fail to repay the loan, you risk losing your home because it is used as collateral. Additionally, the land may not appreciate in value as expected, leaving you with a property worth less than the loan amount. Zoning issues can also impact the land’s usability, affecting its value and your ability to use it for intended purposes.

How long does it take to get a home equity loan for buying land?

The approval and disbursement process for a home equity loan typically takes between 4 to 6 weeks. This includes submitting your application, the lender processing and approving the loan, and completing an appraisal. After approval, you’ll close the loan and receive the funds to purchase the land. Make sure to factor in this timeframe when planning your land purchase.

Are there alternatives to home equity loans for purchasing land?

Yes, there are alternatives to home equity loans for purchasing land. Land loans are available from some lenders, offering terms tailored for land purchases. If you don’t have enough equity, a personal loan may be an option, though it may come with higher interest rates. Additionally, some land sellers offer seller financing, which can simplify the process without needing a traditional lender.

Can I use a home equity loan to buy land and develop it?

Yes, you can use a home equity loan to buy land and develop it. However, it’s crucial to check with your lender to ensure they allow this. Some lenders may restrict how the loan funds can be used, while others may permit both the purchase and development costs. Be sure to confirm these details during the loan application process to avoid any surprises.

What happens if the value of the land drops?

If the value of the land drops, you may owe more than the land is worth, especially if you’ve used your home as collateral. This could be risky if you need to sell the land or repay the loan early. In the worst-case scenario, if you default on the loan, the lender could foreclose on both your home and the land. It’s important to carefully assess the land’s potential before committing to the loan.

Key Takeaways

- Understanding Home Equity Loans: A home equity loan allows you to borrow against the equity in your home, providing a lump sum with fixed interest rates and repayment terms.

- Advantages and Risks: While home equity loans offer lower interest rates and fixed payments, they carry the risk of foreclosure if not repaid, and the land purchased may not appreciate as expected.

- Borrowing Limits: The amount you can borrow depends on your home’s value, existing mortgage balance, and the lender’s loan-to-value ratio, typically up to 80%.

- Application Process: Applying involves assessing your credit score, determining your home’s equity, comparing lenders, submitting an application, and closing the loan.

Share this post:

AddTable of Contents