Home Equity Loan To Pay Off Mortgage

Last updated 01/02/2025 by

Benjamin Locke

Edited by

Andrew Latham

Summary:

A home equity loan is a financial product that allows homeowners to borrow against the equity in their property. This article will explain how home equity loans can be used to pay off your mortgage, the advantages and disadvantages of doing so, and how it can impact your personal finances in the long term.

When considering ways to pay off your mortgage faster, a home equity loan (HEL) may seem like an appealing option. By tapping into the value of your property, you could potentially reduce high mortgage interest rates or consolidate multiple debts into one manageable payment. However, taking out a home equity loan comes with its own set of risks and rewards. This guide will explore how home equity loans work, their pros and cons, and whether they are a good option for paying off your mortgage.

Compare Home Equity Loans

Compare rates from multiple Home Equity Loan providers. Discover your lowest eligible rate.

What is a home equity loan?

A home equity loan is a type of second mortgage where the borrower uses the equity in their home as collateral. Home equity is the difference between your home’s current market value and the outstanding balance of your mortgage. For example, if your home is worth $250,000 and you owe $150,000, you have $100,000 in equity. You can borrow against this equity, typically in a lump sum, and repay it over a fixed term with a fixed interest rate.

How does a home equity loan work?

Home equity loans work similarly to traditional mortgages. The lender will appraise your home to determine how much equity you have, and they will lend you a portion of that value. The loan is secured by your home, meaning that if you fail to repay the loan, the lender could foreclose on your property.

Can you use a home equity loan to pay off your mortgage?

Yes, you can use a home equity loan to pay off your existing mortgage, but it’s important to understand the implications. By doing so, you could refinance your mortgage and potentially lower your interest rate. If your current mortgage has a high interest rate, taking out a home equity loan could help you save money over the life of the loan. However, there are risks involved.

How to qualify for a home equity loan

To qualify for a home equity loan, lenders typically require that you meet certain criteria:

- Good credit score: Lenders will look at your credit score to determine your eligibility and the interest rate you’ll be offered.

- Equity in your home: You need to have enough equity in your home to secure the loan. Most lenders will allow you to borrow up to 85% of your home’s value.

- Stable income: Lenders want to ensure that you have the income necessary to repay the loan.

- Low debt-to-income ratio: Your debt-to-income ratio is an important factor in determining whether you can afford the loan.

Advantages and Disadvantages of Using a Home Equity Loan to Pay Off Your Mortgage

Using a home equity loan to pay off your mortgage can have several benefits, such as lower interest rates and improved cash flow. However, there are also risks involved, including the potential loss of your home and reduced equity. Below is a breakdown of the key advantages and disadvantages to consider:

| Advantages | Disadvantages |

|---|---|

| Lower interest rate: If the interest rate on your current mortgage is higher than the rate offered on a home equity loan, you could save money on interest payments over time. | Risk of losing your home: If you fail to repay the home equity loan, your home could be foreclosed upon. |

| Consolidation: If you have multiple debts (e.g., mortgage, credit card debt, personal loans), consolidating them with a home equity loan can simplify your payments and potentially reduce your interest rates. | Not always a long-term solution: While a home equity loan may provide immediate relief, it doesn’t address the underlying issues that caused financial strain in the first place. |

| Improved cash flow: A home equity loan can provide immediate cash that you can use for a variety of purposes, including paying off your mortgage. | Equity reduction: Borrowing against your home’s equity reduces the amount of ownership you have in your property, which could affect your long-term financial situation. |

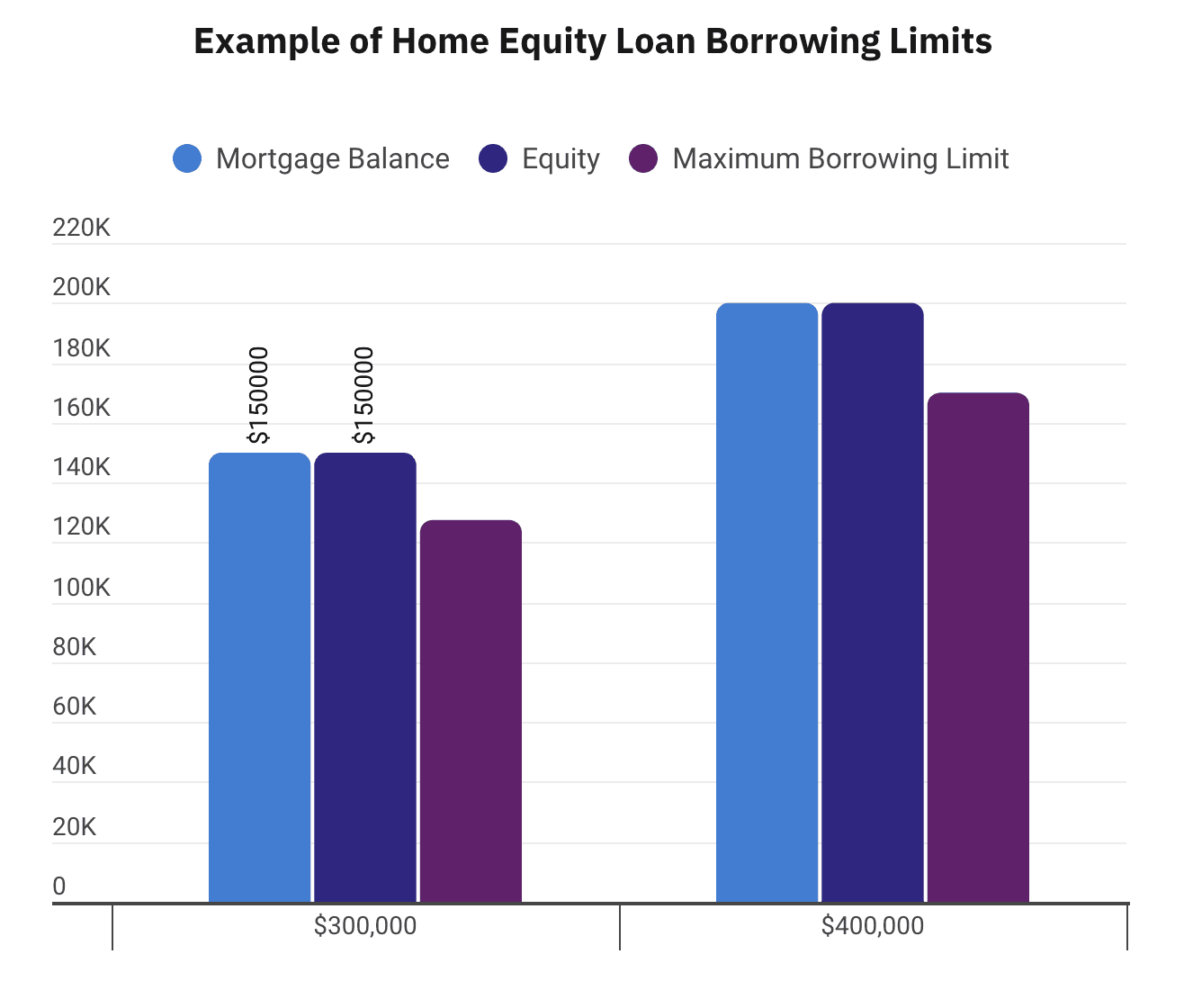

Calculating how much you can borrow

The amount you can borrow depends on the amount of equity you have in your home. Lenders typically allow you to borrow up to 85% of your home’s value, minus what you owe on your mortgage. For example, if your home is worth $300,000 and you owe $150,000 on your mortgage, you may be able to borrow up to $150,000.

Alternatives to using a home equity loan to pay off your mortgage

If you are considering a home equity loan to pay off your mortgage, it’s also worth exploring other options:

| Option | Description |

|---|---|

| Refinancing your mortgage | If interest rates have dropped since you originally took out your mortgage, refinancing could lower your monthly payment or shorten the term of your loan. |

| Personal loan | If you don’t want to risk your home, a personal loan could be a good alternative for consolidating debt. |

| Cash-out refinancing | This involves refinancing your mortgage for more than you owe and using the excess cash to pay off other debts. |

FAQ

How does a home equity loan differ from a home equity line of credit (HELOC)?

A home equity loan provides a lump sum of money that is paid back over a fixed term with a fixed interest rate. In contrast, a HELOC functions like a credit card, where you can borrow against your home’s equity up to a certain limit, with a variable interest rate. A HELOC offers more flexibility, but a home equity loan can offer more predictable payments.

Can I use a home equity loan to pay off my second mortgage?

Yes, you can use a home equity loan to pay off a second mortgage if you have enough equity in your home. This may help reduce your monthly payments, but it’s important to consider the terms of the home equity loan and ensure it’s a viable long-term solution.

What happens if I can’t repay a home equity loan?

If you fail to repay a home equity loan, the lender can take legal action to foreclose on your home, as the loan is secured by your property. It’s important to understand the risks before borrowing and to ensure you can afford the loan payments.

Can I pay off a home equity loan early?

Yes, you can typically pay off a home equity loan early without penalty, depending on the lender’s terms. Early repayment may reduce the total interest you pay over the life of the loan, but you should verify any prepayment penalties before proceeding.

Is a home equity loan a good option if I have bad credit?

It can be more difficult to qualify for a home equity loan with bad credit, as lenders typically look for a good credit score to determine eligibility and interest rates. However, if you have substantial equity in your home, you may still be able to secure a loan, but expect to pay a higher interest rate.

Key takeaways

- A home equity loan allows you to borrow against your home’s equity to pay off your mortgage or consolidate other debts.

- Using a home equity loan could lower your interest rate, consolidate debt, and improve cash flow, but it comes with the risk of foreclosure if payments are missed.

- To qualify for a home equity loan, you need a good credit score, sufficient equity, stable income, and a low debt-to-income ratio.

- Alternatives to a home equity loan, such as refinancing, personal loans, or cash-out refinancing, could also help with paying off your mortgage without tapping into your home’s equity.

Share this post:

AddTable of Contents