I Need $5,000 Dollars Now With Bad Credit

Last updated 01/13/2025 by

Benjamin Locke

Edited by

Andrew Latham

Summary:

If you need $5,000 quickly but have bad credit, this guide outlines accessible options such as personal loans, credit unions, and secured lending. It also provides alternative strategies to raise funds, avoid predatory lending, and improve your credit score for better financial outcomes.

Facing a financial emergency is stressful, and needing $5,000 when you have bad credit can feel like an impossible challenge. Many traditional lenders may reject your application or charge you high interest rates. However, you still have options. This article explores various ways to secure a loan or raise funds, even with a poor credit score. It also provides practical steps to improve your credit, avoid predatory lending, and regain financial stability.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What does it mean to have bad credit?

Bad credit refers to a low credit score, typically below 580 on the FICO scale. A poor credit score can result from several factors, including late payments, high credit card balances, defaulted loans, or bankruptcy. Having bad credit signifies to lenders that you may pose a higher risk of default, which can make it more challenging to secure loans, credit cards, or even rental agreements.

The effects of bad credit extend beyond higher interest rates or loan denials. Bad credit can:

- Limit your ability to access favorable loan terms.

- Increase costs for utilities or insurance premiums.

- Lead to rejection for housing or job applications in certain cases.

Understanding what contributes to bad credit and how it impacts your financial life is essential. By identifying the root causes of a low credit score, you can take steps to improve it over time, opening doors to better financial opportunities.

How bad credit impacts borrowing terms

Borrowers with bad credit often face higher costs and stricter loan terms. Below is a comparison of average APRs based on credit score:

| Credit Score Range | Average APR | Loan Term |

|---|---|---|

| 300-579 | 25% – 36% | 12 – 36 months |

| 580-669 | 18% – 25% | 24 – 48 months |

| 670-739 | 10% – 15% | 36 – 60 months |

Understanding your financial options

If you have bad credit and need $5,000, knowing your options can make all the difference. While some traditional lenders may be hesitant to approve your application, several alternatives cater to individuals with low credit scores. These include:

| Option | Description |

|---|---|

| Personal Loans | Many online lenders specialize in personal loans for bad credit borrowers. Though the interest rates might be higher, these loans provide fast access to funds and flexible repayment terms. |

| Credit Unions | Credit unions are member-focused institutions that often consider factors beyond credit scores, such as your financial history with them. They may offer lower rates and tailored loan options for bad credit individuals. |

| Secured Loans | By offering collateral such as a car or savings account, you can qualify for a secured loan. These loans typically feature lower interest rates but come with the risk of losing the collateral if you fail to repay. |

| Peer-to-Peer Lending Platforms | These platforms connect you directly with individual investors who may be more willing to lend to someone with a poor credit score. The terms and interest rates can vary, so comparison shopping is key. |

| Alternative Income Strategies | If loans aren’t a viable option, you can explore other ways to raise $5,000, such as freelancing, selling valuable items, or starting a side hustle. These options allow you to avoid incurring additional debt while meeting your financial needs. |

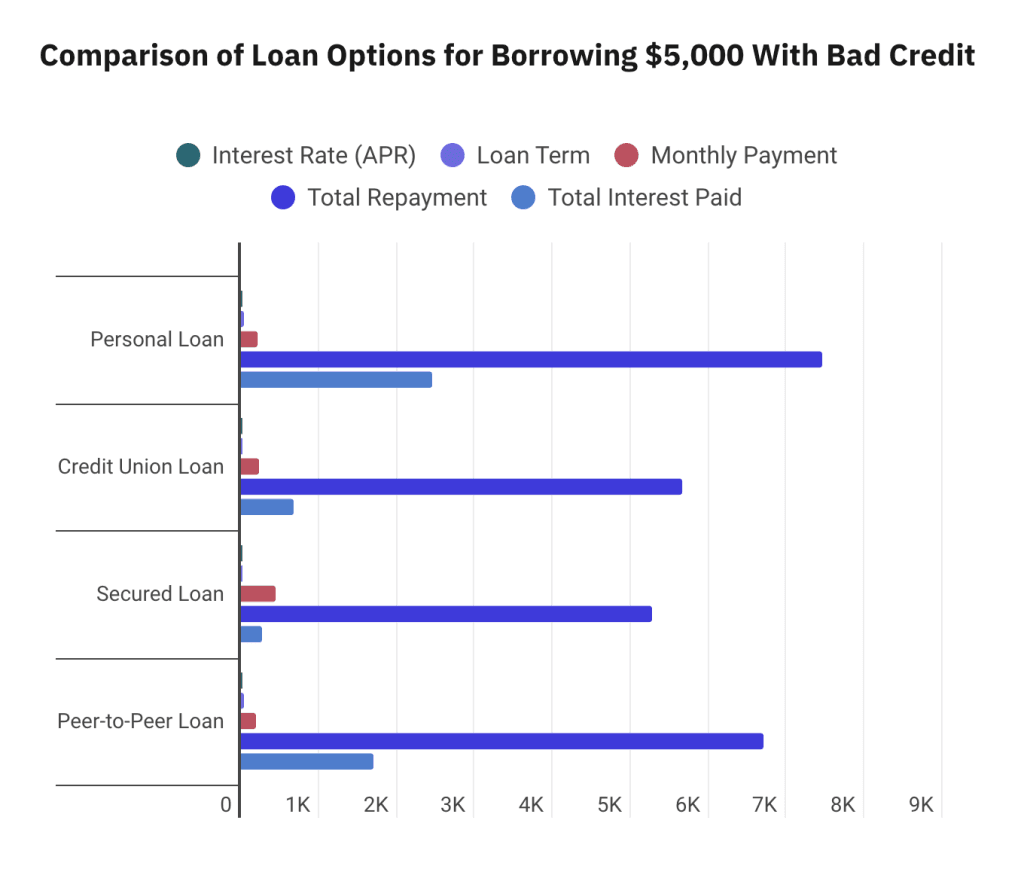

Personal loans

Personal loans are one of the fastest and most accessible ways to borrow money. Many lenders specialize in helping individuals with low credit scores. However, expect higher interest rates and stricter repayment terms:

- Interest rates: Generally range from 15% to 36% for bad credit borrowers.

- Loan terms: Typically range from 12 to 60 months.

- Loan amounts: Start as low as $1,000 and can go up to $50,000, depending on the lender.

Emily’s personal loan

To illustrate how a personal loan can help someone with bad credit, let’s consider a real-life example. Personal loans are often chosen for their flexibility and relatively quick approval process, even for individuals with less-than-perfect credit. However, borrowers must be prepared for higher interest rates and total repayment costs. Below, we’ll explore Emily’s story—a freelancer with bad credit—and calculate how a $5,000 personal loan impacts her finances over three years.

Emily, a 32-year-old freelancer with a FICO score of 570, needs $5,000 for unexpected medical expenses. She applies for a personal loan from an online lender that specializes in loans for individuals with bad credit.

| Loan Details | Value |

|---|---|

| Loan Amount | $5,000 |

| APR | 28% |

| Loan Term | 36 months |

| Monthly Payment | $207.10 |

| Total Repayment | $7,455.60 |

| Total Interest | $2,455.60 |

Monthly Payment Calculation:

Using the loan formula for monthly payments:

Using the loan formula for monthly payments:

Emily’s monthly payment is approximately $207.10, and over three years, she will repay $7,455.60, which includes $2,455.60 in interest.

Credit unions

Credit unions offer loans tailored for their members, often with more favorable terms than banks. They are especially helpful for bad credit borrowers because they consider your overall financial situation rather than just your credit score. Key benefits include:

- Lower interest rates compared to traditional lenders.

- Flexible eligibility criteria, including bad credit borrowers.

- Emergency small-dollar loans designed to help in urgent situations.

Carlos’ credit union loan

Carlos, a teacher with a FICO score of 590, needs $5,000 to replace his car. He decides to apply for a personal loan at his local credit union, where he has been a member for three years.

| Loan Details | Value |

|---|---|

| Loan Amount | $5,000 |

| APR | 15% |

| Loan Term | 24 months |

| Monthly Payment | $236.10 |

| Total Repayment | $5,666.40 |

| Total Interest | $666.40 |

Monthly Payment Calculation:

Using the loan formula:

Using the loan formula:

Outcome:

Carlos’ monthly payment is approximately $236.10, and over two years, he will repay $5,666.40, which includes $666.40 in interest.

Carlos’ monthly payment is approximately $236.10, and over two years, he will repay $5,666.40, which includes $666.40 in interest.

Secured personal loans

Secured loans require collateral, such as a car, savings account, or other valuable assets. These loans often feature lower interest rates and higher approval odds for borrowers with bad credit. However, there’s a risk of losing the collateral if you fail to repay. Since these loans pose less risk to lenders, they often come with better terms:

- Lower interest rates compared to unsecured loans.

- Higher approval rates for individuals with bad credit.

Jasmine’s secured loan

Jasmine, a small business owner with a FICO score of 540, needs $5,000 to repair her store after a flood. She uses her car, valued at $12,000, as collateral for a secured loan.

| Loan Details | Value |

|---|---|

| Loan Amount | $5,000 |

| APR | 10% |

| Loan Term | 12 months |

| Monthly Payment | $439.50 |

| Total Repayment | $5,274.00 |

| Total Interest | $274.00 |

Monthly Payment Calculation:

Outcome:

Jasmine’s monthly payment is approximately $439.50, and over one year, she will repay $5,274.00, which includes $274.00 in interest. If she defaults, her lender may repossess her car.

Jasmine’s monthly payment is approximately $439.50, and over one year, she will repay $5,274.00, which includes $274.00 in interest. If she defaults, her lender may repossess her car.

Peer-to-peer lending

Peer-to-peer (P2P) platforms connect borrowers directly with individual investors. These platforms often consider alternative data, such as your employment history or monthly income, rather than relying solely on credit scores. Examples of popular P2P lending platforms include:

- Prosper

- Upstart

- LendingClub

Mark’s P2P loan

Mark, a graphic designer with a FICO score of 560, needs $5,000 to consolidate high-interest credit card debt. He applies for a loan on a peer-to-peer lending platform.

| Loan Details | Value |

|---|---|

| Loan Amount | $5,000 |

| APR | 20% |

| Loan Term | 36 months |

| Monthly Payment | $186.00 |

| Total Repayment | $6,696.00 |

| Total Interest | $1,696.00 |

Monthly Payment Calculation:

Outcome:

Mark’s monthly payment is approximately $186.00, and over three years, he will repay $6,696.00, which includes $1,696.00 in interest.

Mark’s monthly payment is approximately $186.00, and over three years, he will repay $6,696.00, which includes $1,696.00 in interest.

Expert Insight

”Obtaining a $5,000 loan with bad credit can be challenging, but it’s not impossible. One option is to approach credit unions, as they often have more lenient lending standards compared to traditional banks and may be more willing to work with borrowers who have less-than-perfect credit. If you’re not already a member, consider joining a local credit union, as they might offer personal loans with more favorable terms. Another route is to explore online lenders specializing in bad credit, such as Upstart, Avant, or LendingPoint, which cater specifically to individuals with lower credit scores. However, be sure to compare APRs and fees carefully, as interest rates for bad credit loans tend to be higher. Additionally, secured personal loans could be an option, where you use collateral like a vehicle, savings account, or other assets to secure the loan. Just be cautious—ensure you can meet repayment obligations to avoid losing your collateral.” – Iqbal Ahmad, Founder & CEO | Britannia School of Academics

Obtaining a $5,000 loan with bad credit can be challenging, but it’s not impossible. One option is to approach credit unions, as they often have more lenient lending standards compared to traditional banks and may be more willing to work with borrowers who have less-than-perfect credit. If you’re not already a member, consider joining a local credit union, as they might offer personal loans with more favorable terms. Another route is to explore online lenders specializing in bad credit, such as Upstart, Avant, or LendingPoint, which cater specifically to individuals with lower credit scores. However, be sure to compare APRs and fees carefully, as interest rates for bad credit loans tend to be higher. Additionally, secured personal loans could be an option, where you use collateral like a vehicle, savings account, or other assets to secure the loan. Just be cautious—ensure you can meet repayment obligations to avoid losing your collateral.

Steps to secure $5,000 with bad credit

Securing $5,000 with bad credit may seem daunting, but it’s entirely possible with the right approach. While traditional lenders often hesitate to approve applications from individuals with poor credit, understanding alternative options and taking strategic steps can increase your chances of success. By being proactive—such as reviewing your credit report, exploring tailored loan products, or considering creative income solutions—you can access the funds you need while minimizing costs and avoiding financial pitfalls. Below, we outline actionable steps to help you navigate this challenge effectively.

1. check your credit report

Start by obtaining a free copy of your credit report from services like AnnualCreditReport.com. Check for errors or outdated information that could be dragging down your score. Dispute inaccuracies promptly to improve your chances of loan approval.

2. research lenders

Not all lenders have the same requirements or offer the same terms. Focus on lenders that specialize in bad credit loans. Compare factors like interest rates, loan terms, and fees before applying.

3. apply with a co-signer

A co-signer with good credit can strengthen your application and help you qualify for better rates and terms. However, ensure both parties fully understand the financial responsibilities involved.

4. explore secured loan options

If you own valuable assets, consider using them as collateral for a secured loan. This approach may make it easier to qualify and obtain lower interest rates.

5. consider alternative income streams

If taking out a loan isn’t feasible, explore ways to earn extra income. Options like side hustles or selling valuable items can help you raise funds quickly.

Alternative ways to raise $5,000

Credit card cash advances

If you have a credit card, a cash advance can provide immediate funds. However, these advances often carry high fees and interest rates, so use them sparingly.

Selling assets

Consider selling items of value, such as jewelry, electronics, or collectibles. Online marketplaces or pawn shops can provide quick cash without taking on debt.

Starting a side hustle

Side hustles can generate extra income quickly. Popular options include:

- Ridesharing: Drive for platforms like Uber or Lyft.

- Delivery services: Work with apps like DoorDash or Instacart.

- Freelancing: Offer skills like graphic design, writing, or virtual assistance online.

FAQ

Can I improve my credit score while repaying a loan?

Yes, repaying a loan on time consistently can positively impact your credit score. Lenders report your payments to credit bureaus, and timely payments help improve your payment history, which is a key factor in credit scoring.

What is the difference between secured and unsecured loans?

A secured loan requires collateral, such as a car or savings account, which the lender can seize if you default. Unsecured loans don’t require collateral but typically come with higher interest rates since they are riskier for the lender.

Are payday loans a good option for bad credit borrowers?

Payday loans should generally be avoided due to their extremely high interest rates and short repayment terms. These loans often trap borrowers in cycles of debt, making them a risky option even in emergencies.

How do co-signers affect loan eligibility and terms?

A co-signer with good credit can help you qualify for a loan with better terms, such as lower interest rates and longer repayment periods. However, the co-signer is equally responsible for the debt, so any missed payments could harm their credit score.

Can I negotiate better terms with lenders for bad credit loans?

Yes, you can often negotiate better terms by demonstrating steady income, offering a larger down payment, or improving your credit score slightly before applying. Some lenders are willing to customize loan terms based on individual circumstances.

Key takeaways

- Securing $5,000 with bad credit is possible through personal loans, credit unions, secured loans, or peer-to-peer lending platforms tailored for low-credit borrowers.

- Alternative income strategies like freelancing, selling assets, or starting a side hustle can provide non-debt solutions to financial emergencies.

- Understanding your loan’s APR, term, and repayment schedule is critical to managing costs and avoiding financial pitfalls.

- Proactively improving your credit score by addressing errors on your credit report and making timely payments can enhance future borrowing opportunities.

Share this post:

Table of Contents