Is a Home Equity Loan a Good Idea

Last updated 12/13/2024 by

Benjamin Locke

Edited by

Andrew Latham

Summary:

A home equity loan allows homeowners to borrow against the value of their home. It’s a useful option for accessing large amounts of money, but it comes with risks. This article covers the advantages, disadvantages, and scenarios where a home equity loan might or might not be a good idea for personal finance.

Compare Home Equity Loans

Compare rates from multiple Home Equity Loan providers. Discover your lowest eligible rate.

What is a home equity loan?

A home equity loan, often referred to as a second mortgage, allows you to borrow against the value of your home. It is a lump sum loan that uses the equity in your home as collateral. Equity is the difference between what you owe on your mortgage and the current market value of your home.

For example, if your home is worth $300,000 and you owe $150,000 on your mortgage, your home equity would be $150,000. Lenders may offer a loan based on this equity, typically up to 80% of the appraised value of your home.

How does a home equity loan work?

A home equity loan works similarly to a traditional mortgage. You borrow a lump sum, and then you repay the loan over a set period with interest. The interest rates on home equity loans are generally lower than those on credit cards or personal loans because the loan is secured by your home.

The loan term can range from 5 to 30 years, with fixed interest rates and monthly payments. The amount you can borrow is typically based on the equity you have in your home, and you are required to make regular payments to repay the loan.

| Factor | Details |

|---|---|

| Loan Amount | Typically up to 80% of your home’s appraised value minus any existing mortgage balance |

| Interest Rates | Generally lower than unsecured loans because the loan is secured by your home |

| Loan Term | Usually 5 to 30 years |

| Repayment | Fixed monthly payments over the term of the loan |

How to calculate how much you can borrow: Real-life scenarios

When considering a home equity loan, one of the key factors is determining how much you can borrow based on the equity you have in your home. In this section, we’ll walk through real-life scenarios that show how the formula works in different situations.

The amount you can borrow with a home equity loan is determined by your home’s appraised value and the equity you’ve built through paying off your mortgage. Typically, lenders will allow you to borrow up to 80% of your home’s appraised value minus what you owe on your mortgage. Let’s explore a few different scenarios to see how this works in practice.

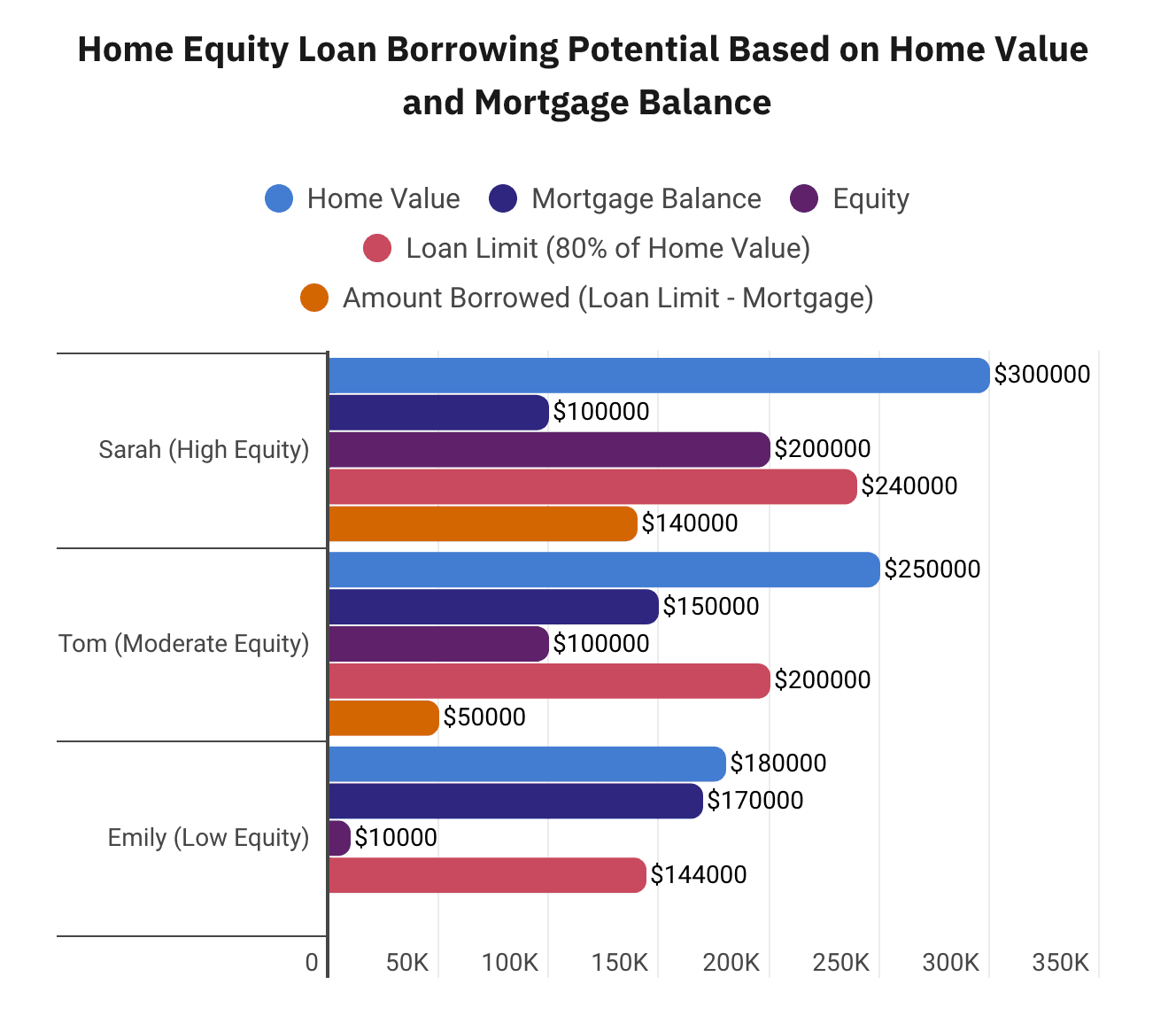

Scenario 1: A Homeowner with High Equity

Meet Sarah, who owns a home valued at $300,000 and owes $100,000 on her mortgage.

| Home Value | Mortgage Balance | Equity | Loan Limit (80% of Home Value) | Amount Sarah Can Borrow |

|---|---|---|---|---|

| $300,000 | $100,000 | $300,000 – $100,000 = $200,000 | 80% of $300,000 = $240,000 | $240,000 – $100,000 = $140,000 |

Sarah can borrow up to 80% of the appraised value of her home. The maximum loan she could qualify for would be:

- Loan Limit = 80% of $300,000 = $240,000

- Amount Sarah Can Borrow = $240,000 – $100,000 = $140,000

Scenario 2: A Homeowner with Moderate Equity

Next, let’s consider Tom, whose home is valued at $250,000, and he owes $150,000 on his mortgage.

| Home Value | Mortgage Balance | Equity | Loan Limit (80% of Home Value) | Amount Tom Can Borrow |

|---|---|---|---|---|

| $250,000 | $150,000 | $250,000 – $150,000 = $100,000 | 80% of $250,000 = $200,000 | $200,000 – $150,000 = $50,000 |

With the same 80% loan-to-value ratio, Tom’s maximum loan amount would be:

- Loan Limit = 80% of $250,000 = $200,000

- Amount Tom Can Borrow = $200,000 – $150,000 = $50,000

Scenario 3: A Homeowner with Low Equity

Finally, let’s look at Emily, who owns a home worth $180,000 and has a mortgage balance of $170,000.

| Home Value | Mortgage Balance | Equity | Loan Limit (80% of Home Value) | Amount Emily Can Borrow |

|---|---|---|---|---|

| $180,000 | $170,000 | $180,000 – $170,000 = $10,000 | 80% of $180,000 = $144,000 | Not Eligible (because equity is too low) |

In Emily’s case, the amount she could borrow is calculated as:

- Loan Limit = 80% of $180,000 = $144,000

- Amount Emily Can Borrow = $144,000 – $170,000 = Not eligible for a loan (negative equity)

Weighing the Benefits and Drawbacks of a Home Equity Loan

Before deciding whether a home equity loan is the right choice for you, it’s important to understand both its advantages and potential risks. While this type of loan can offer substantial benefits, it also comes with significant responsibilities. Take a closer look at the pros and cons to help you make a well-informed decision.

Factors that affect your eligibility for a home equity loan

Several factors influence whether you qualify for a home equity loan, including:

- Credit score: Lenders typically require a good credit score, usually 620 or higher, to qualify for a home equity loan. A higher credit score may help you secure better loan terms and lower interest rates.

- Income and debt levels: Your ability to repay the loan will be assessed based on your income and current debt levels. Lenders want to ensure that you can afford the monthly payments without stretching your finances too thin. A lower debt-to-income ratio is usually favorable.

- Home equity: Lenders typically allow you to borrow up to 80% of your home’s appraised value, minus any existing mortgage balance. If your equity is low, it could limit the loan amount you’re eligible for.

- Appraisal: The lender will often require a professional appraisal to assess your home’s current market value. This helps determine the equity in your home and ensures that the loan amount is appropriate relative to your home’s value.

Share this post:

AddTable of Contents